In the third quarter of 2024, the S&P 500 posted a gain of 5.9%, reflecting the resilience of equity markets as they overcame initial volatility, including a sharp 12% correction in the technology sector. This recovery was driven by a significant shift in Federal Reserve policy, with the Fed implementing a 0.50% rate cut in September, the first such reduction since March 2020.

Sector performance underscored a rotation from growth-oriented areas of the market to more stable, income-generating value sectors. Value stocks out-performed growth stocks, with value sectors like utilities, financials, and consumer staples gaining traction amid market uncertainty. Value stocks returned a robust 9% for the quarter, significantly outperforming growth stocks, which posted a more modest 3.6% gain. Utilities led the way with an impressive 19.4% return, followed by real estate investment trusts (REITs), which gained 17.2%, and financials, which rose 10.7%. These sectors benefited from their defensive characteristics and income-generating potential, which became more attractive as interest rate expectations shifted. Energy, however, was the sole sector in negative territory due to weaker demand and lower oil prices, although it remains up 8.4% year-to-date.

The Federal Reserve’s rate cut also supported a notable rally in small-cap stocks, which outperformed their large-cap counterparts. The Russell 2000 small-cap index gained 9.3% during the quarter, benefitting from the Fed’s dovish stance, as lower rates tend to favor smaller companies that are more sensitive to borrowing costs. This marked a reversal from earlier in the year, when large-cap growth stocks dominated due to their perceived stability in a volatile economic environment.

As of September 30, 2024, our flagship index – the Just U.S. Large Cap Diversified Index (JULCD) has out-performed the Russell 1000 (Cap-Weighted) benchmark by 0.46% year-to-date and by 11.97% since its inception. Additionally, the Just 100 (equally weighted index) has outperformed the Russell 1000 (Equally-Weighted) index by 7.38% year-to-date and by 51.1% since its inception.

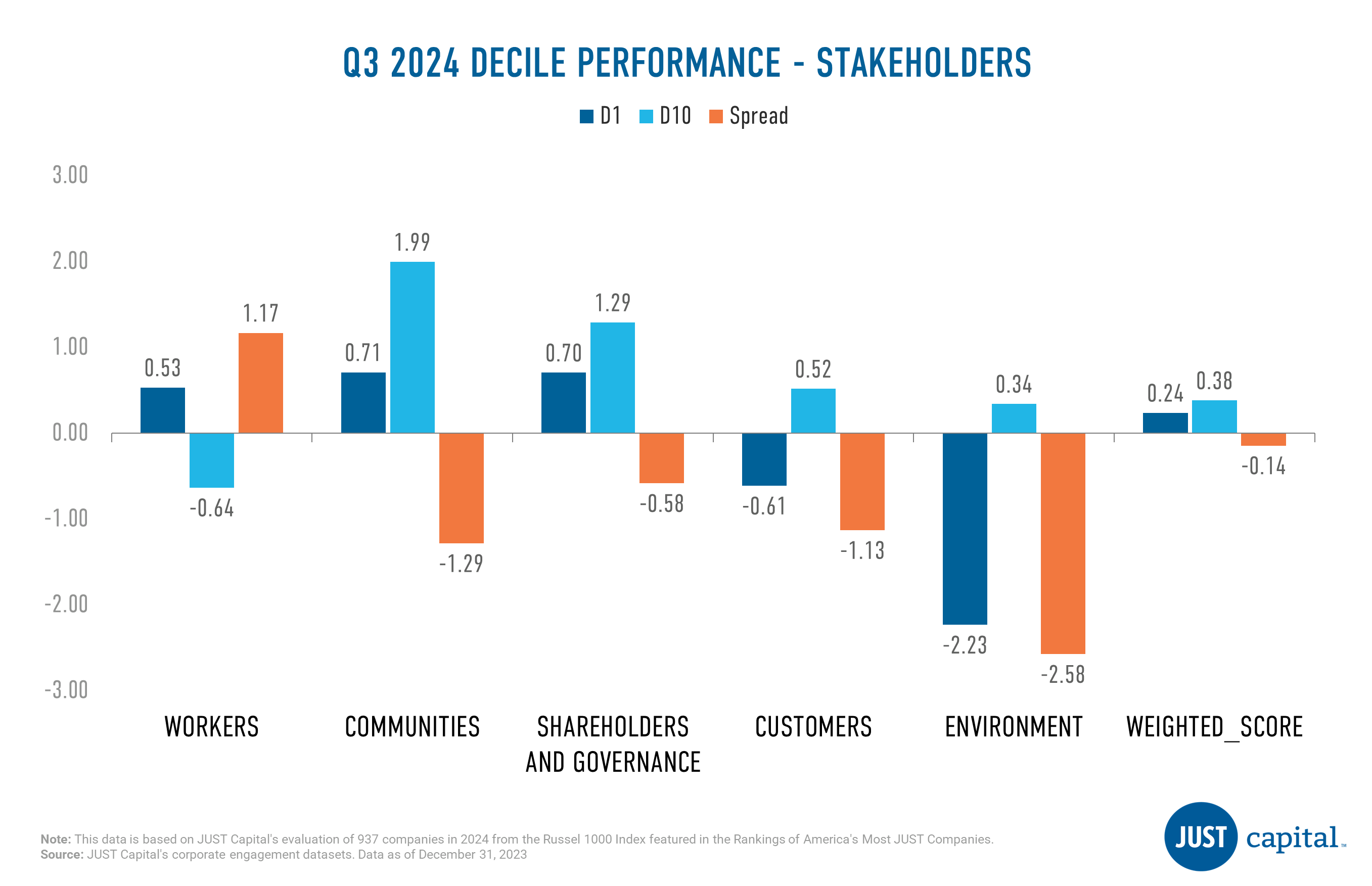

Just Capital found that four out of the five stakeholder categories it tracks delivered negative performance in Q3 2024, with the “Workers” stakeholder being the sole positive performer. The Workers stakeholder delivered the strongest performance over this period with a long-short spread of 1.17%. Notably, within the Workers stakeholder, outperformance was driven by both the top and bottom deciles.

Just Capital’s Overall Weighted Score takes into account the 20 core Issues determined through our annual survey research – including paying a living wage, creating a diverse, inclusive workplace, and helping combat climate change – across key business stakeholders: Workers, Communities, Shareholders & Governance, Customers, and Environment. The Overall Weighted Score delivered an almost neutral long-short spread of -0.14%, with the bottom decile serving as the primary negative contributor for the period ending September 30, 2024. Year-to-date the performance spread between top and bottom decile for Overall Score is at 9.11%

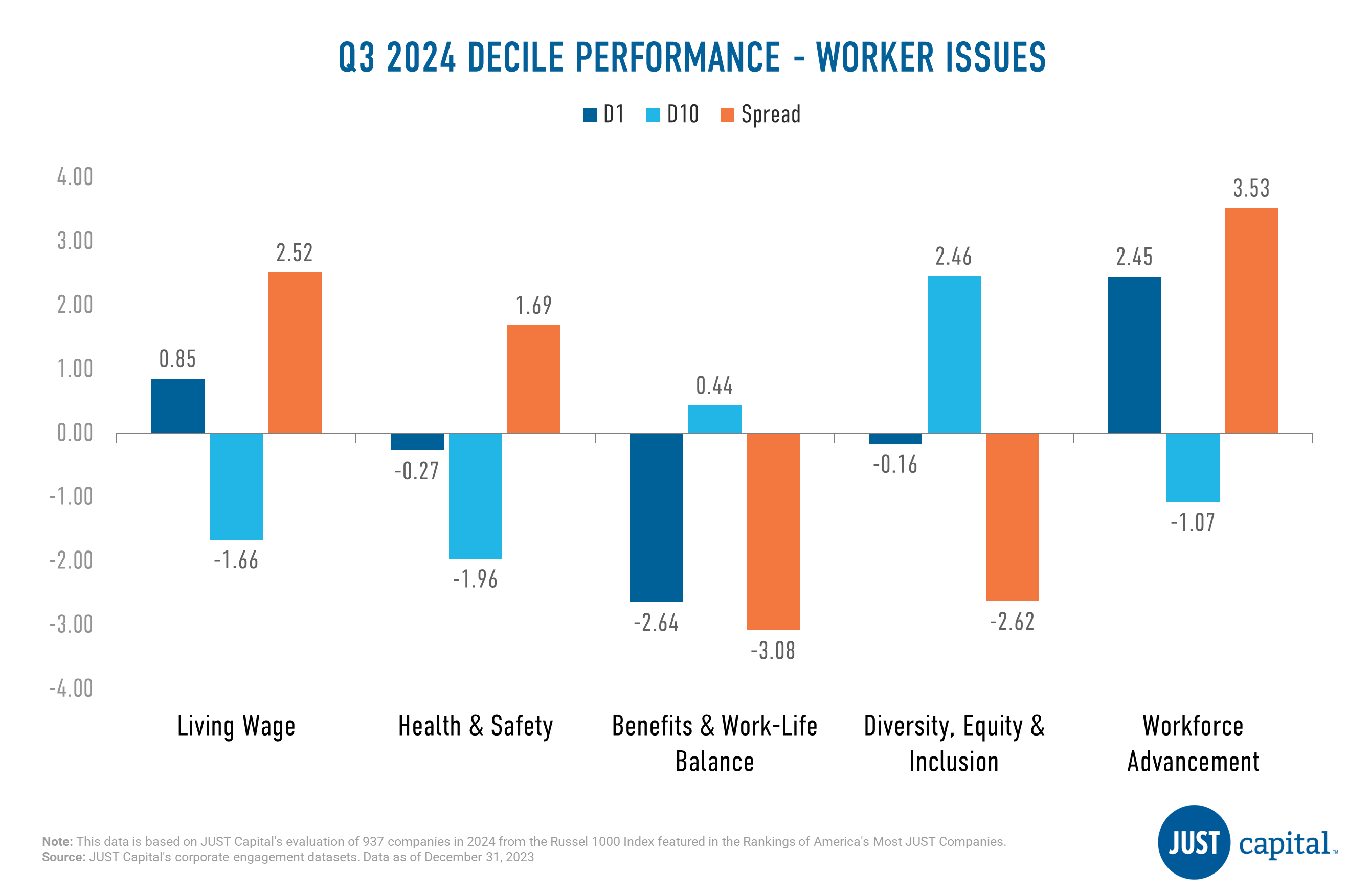

Workers

The Workers stakeholder measures a company across five Issues:

In Q3 2024, we saw three out of five issues deliver positive performance, with the Workforce Advancement Issue faring the best. Benefits & Work-Life Balance was the weakest performer amongst the Worker issues.

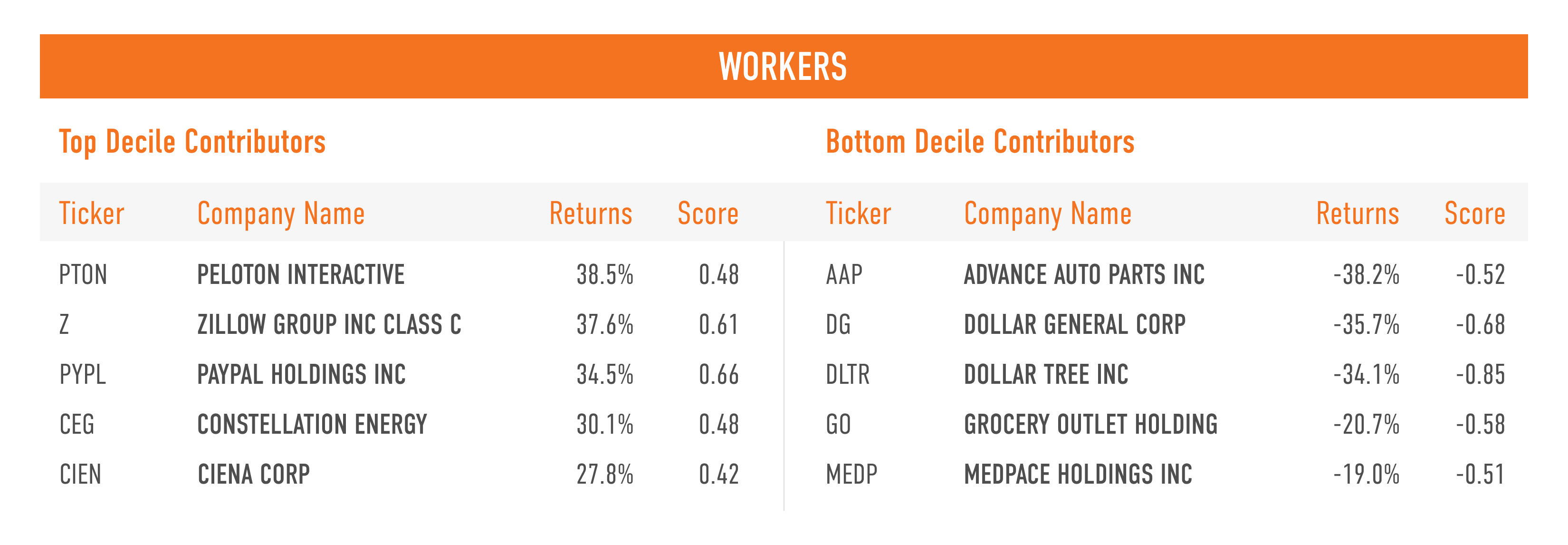

Shown below are the top and bottom five contributors to the top decile (D1), the top-ranked companies as measured by their Workers score, and the bottom decile (D10), the lowest-ranked companies as measured by their Workers score.

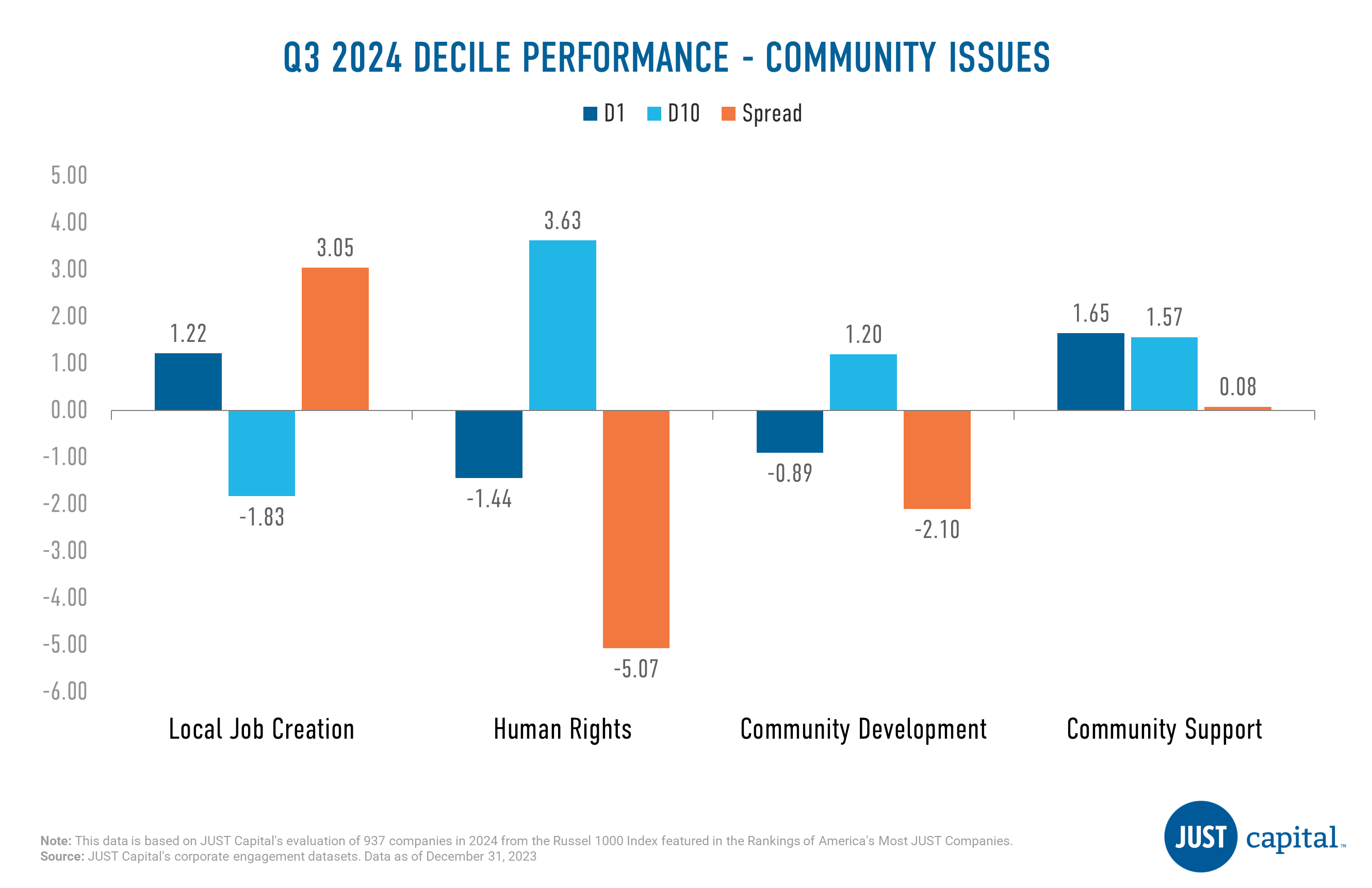

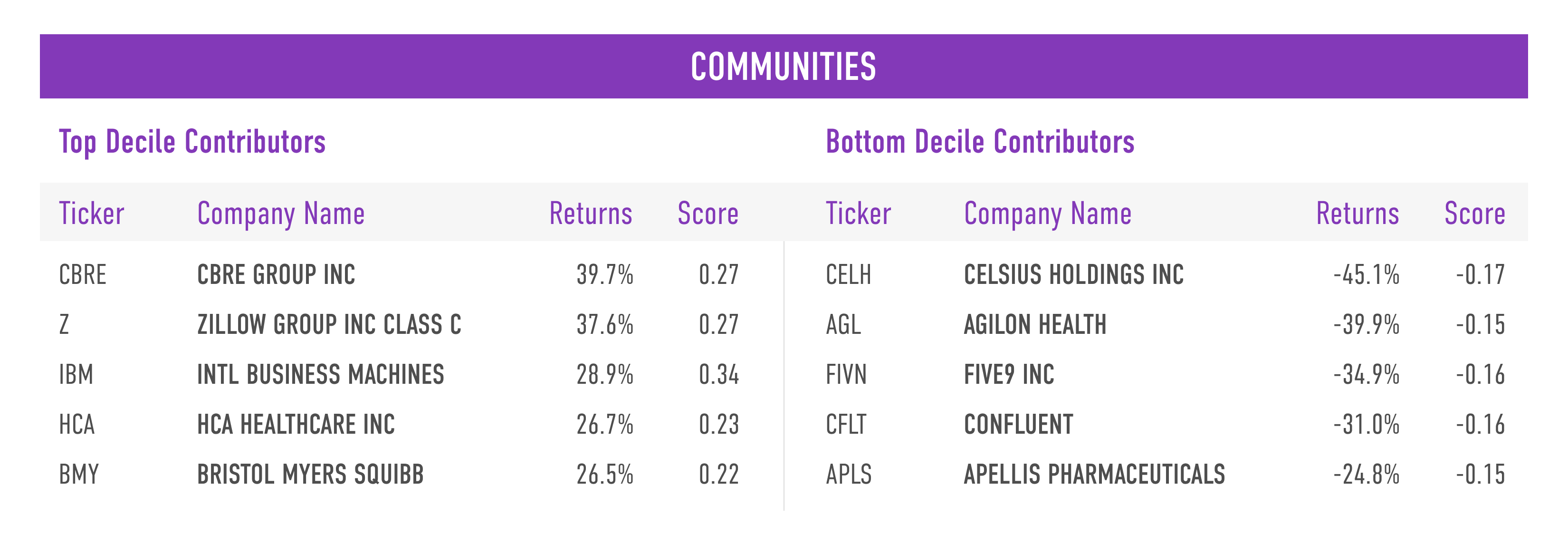

The Communities stakeholder measures a company across four Issues:

Local Job Creation was the strongest performer followed by Community Support. Human Rights and Community Development were negative contributors this quarter.

Shown below are the top and bottom five contributors to the top decile (D1), the best-ranked companies as measured by their Communities score, and the bottom decile (D10), the lowest-ranked companies as measured by their Communities score.

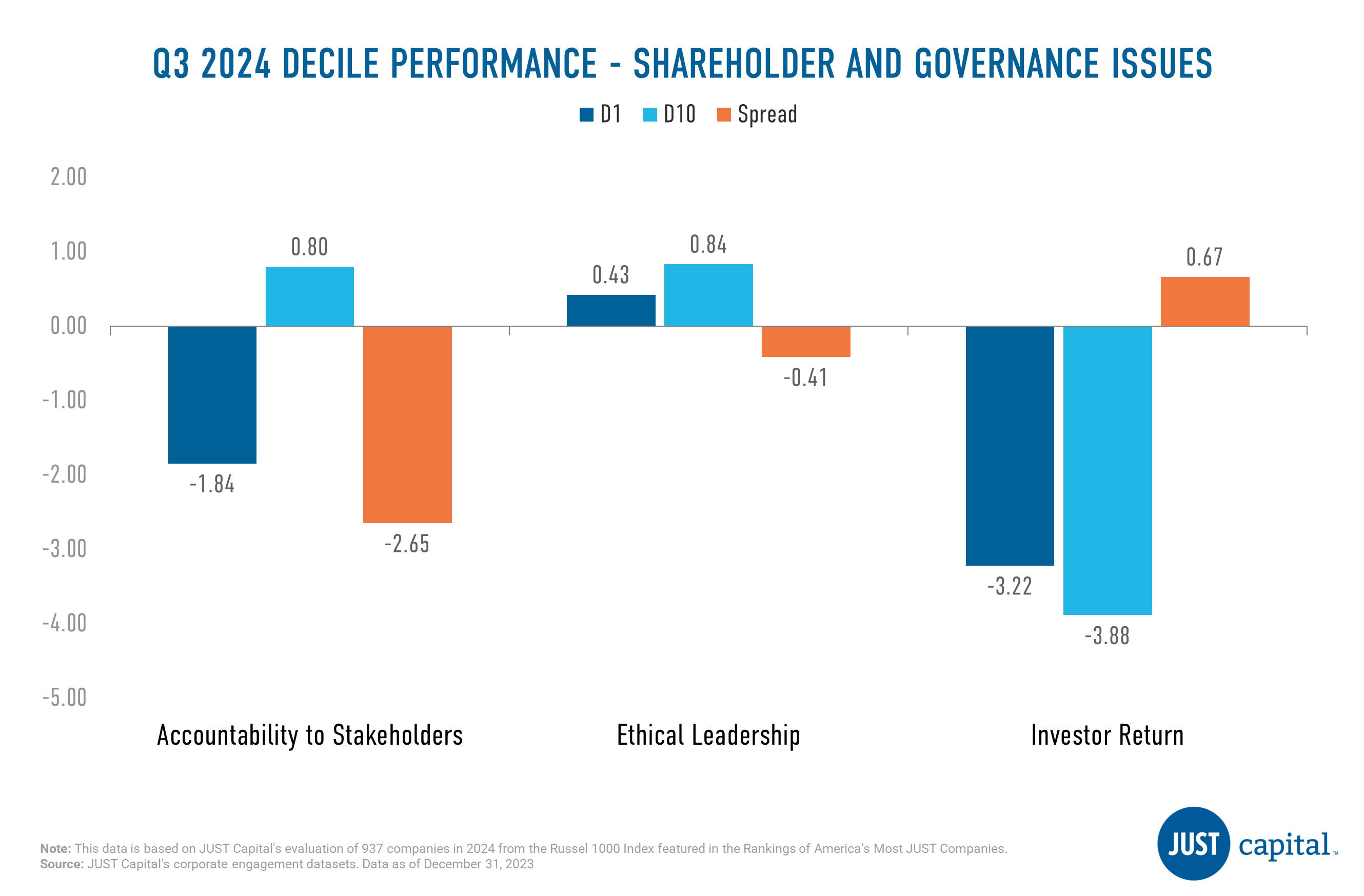

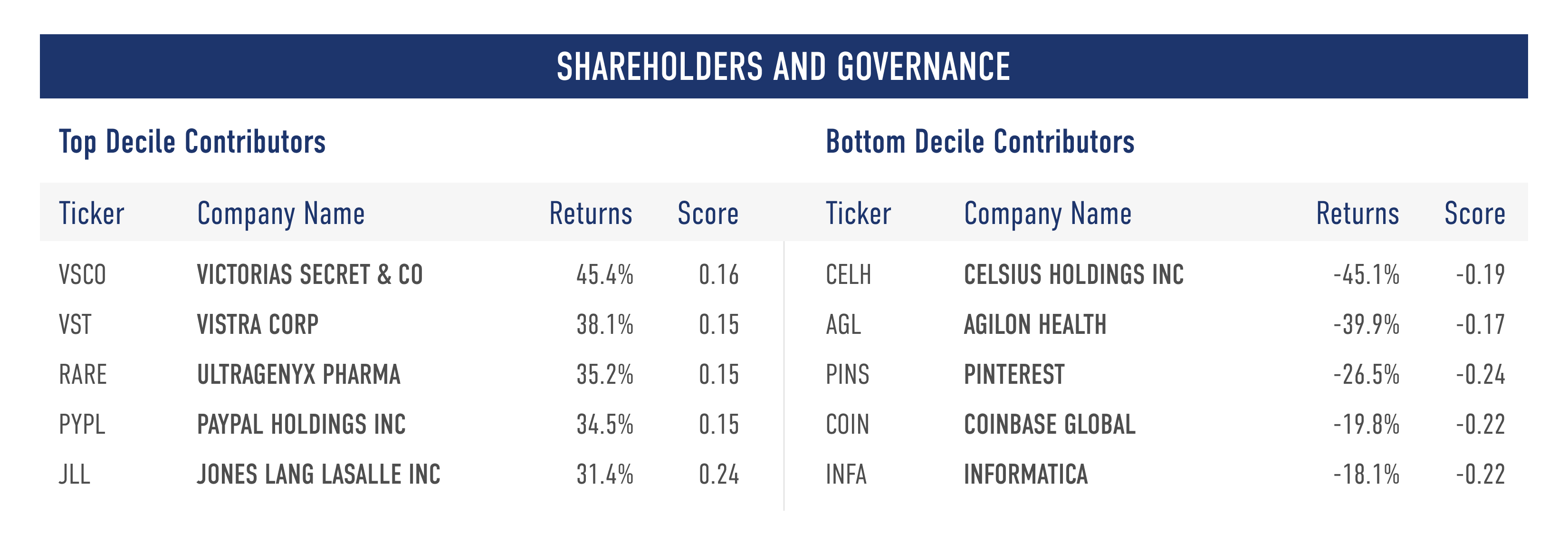

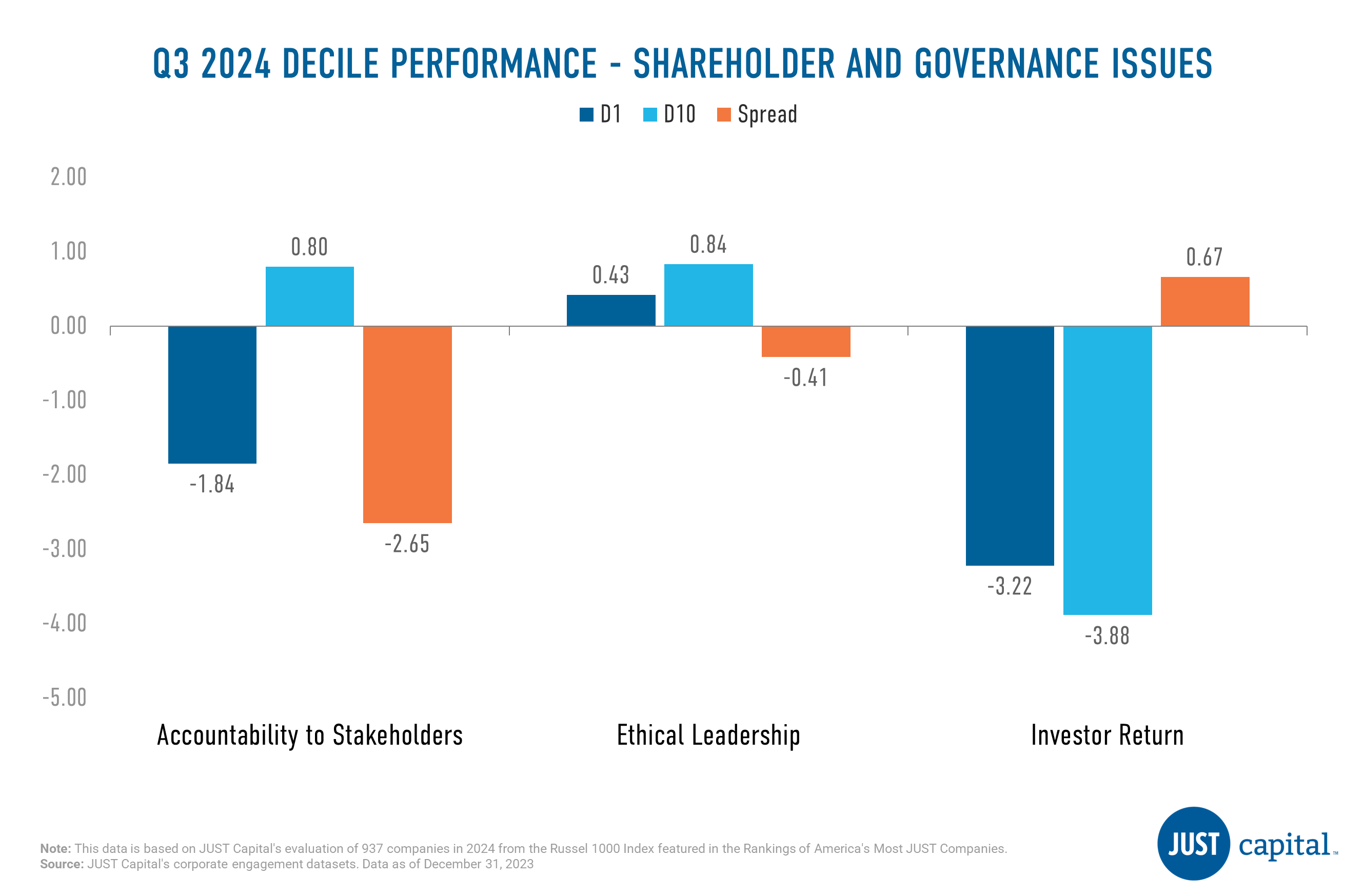

Shareholders and Governance

The Shareholders and Governance stakeholder measures a company across three Issues:

Investor Return Issue was the only positive performer in Q3 with a long-short spread of 0.67%. Remaining issues within the Shareholder stakeholder were negative this quarter.

Shown below are the top and bottom five contributors to the top decile (D1), the best-ranked companies as measured by their Shareholders and Governance score, and the bottom decile (D10), the lowest-ranked companies as measured by their Shareholders and Governance score.

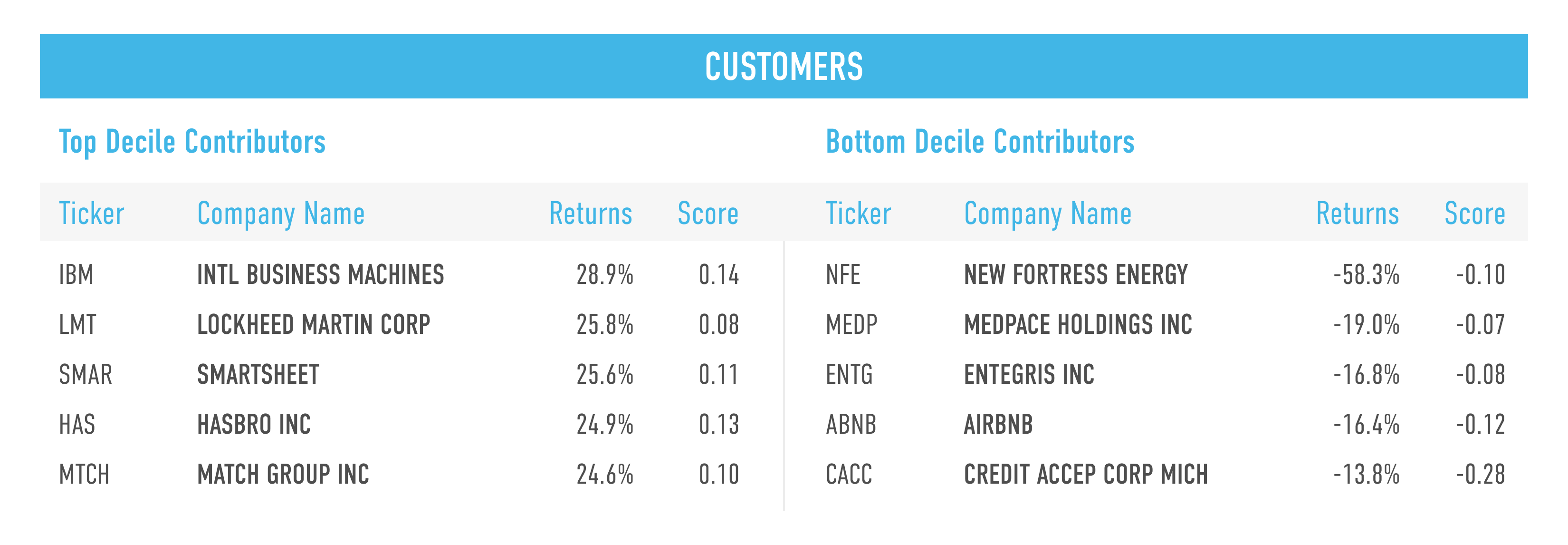

Customers

The Customers stakeholder measures a company across four Issues:

In Q3 2024, all four Customer Issues delivered negative performance. Customer Treatment was the weakest performer followed by Beneficial Products.

Shown below are the top and bottom five contributors to the top decile (D1), the best-ranked companies as measured by their Customers score, and the bottom decile (D10), the lowest-ranked names as measured by their Customers score.

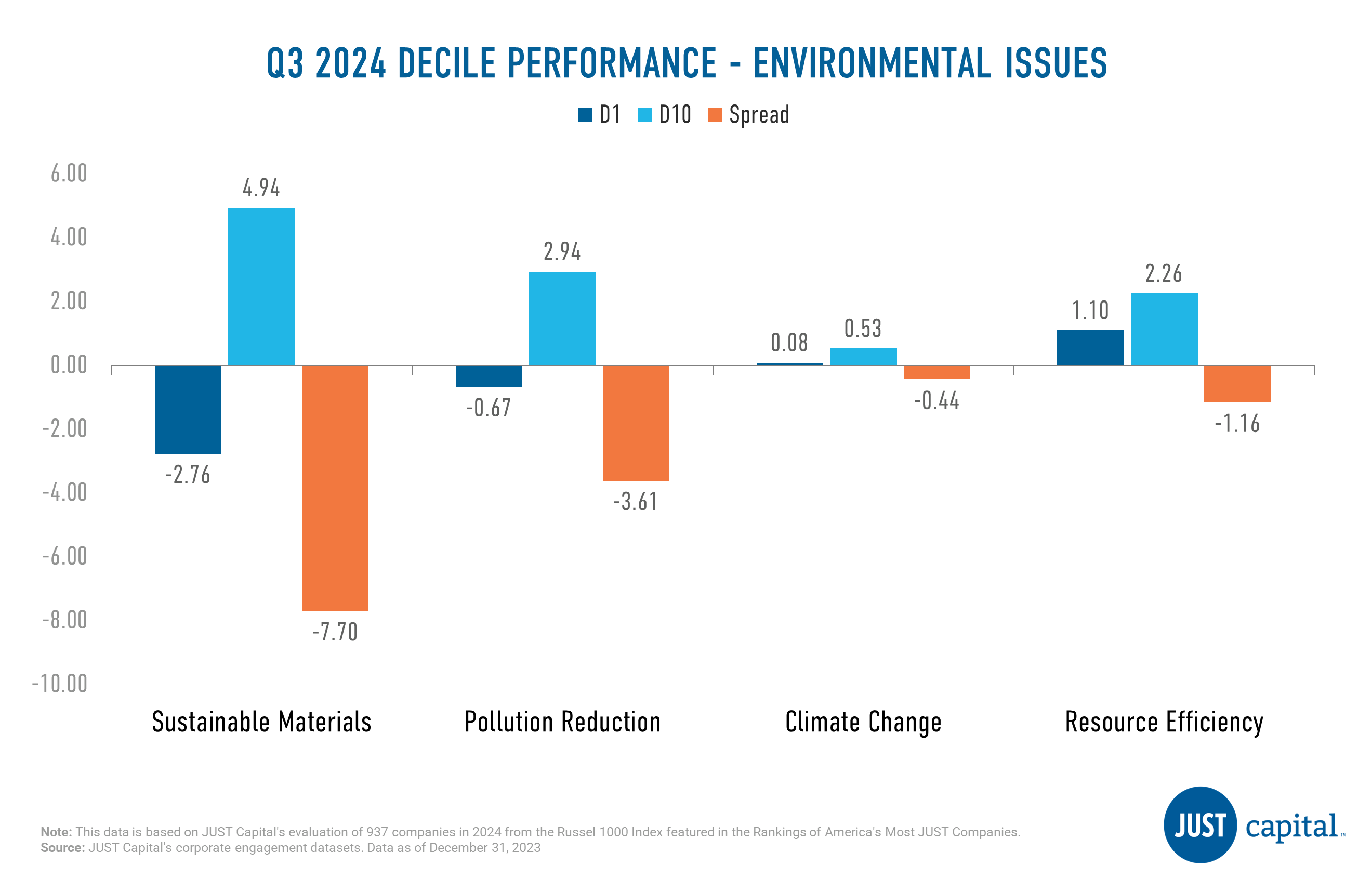

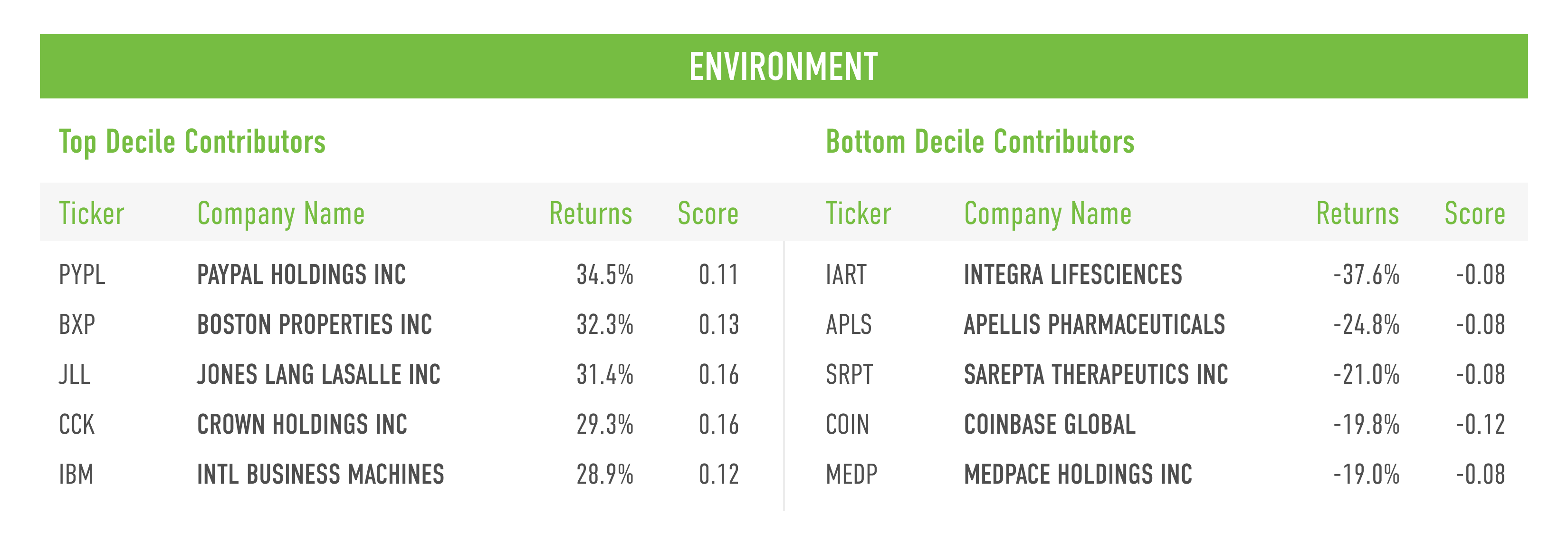

Environment

The Environment stakeholder measures a company across four Issues:

In Q3 2024, we saw all four Environmental issues deliver negative performance. Sustainable Materials was the worst performing issue within Environment stakeholder this quarter.

Shown below are the top and bottom five contributors to the top decile (D1), the best-ranked companies as measured by their Environment score, and the bottom decile (D10), the lowest-ranked companies as measured by their Environment score.

Computation Methodology

We monitor the performance of these stakeholders and Issues on a long-short basis. The long and short portfolios are selected based on the factor scores as the top and bottom deciles within the universe of companies we track in the Russell 1000. Top decile (D1) companies are those that rank highest based on the factor score, and bottom decile (D10) companies are those that rank lowest based on the factor score.

D1 Performance is computed as

(Equally weighted average of returns of stocks in D1 bucket) – (Equally weighted average of returns of all stocks within the Universe)

D10 Performance is computed as

(Equally weighted average of returns of stocks in D10 bucket) – (Equally weighted average of returns of all stocks within the Universe)

Spread is computed as

D1 Performance – D10 Performance

Over two years into the pandemic, the strain it’s placed on working women continues to persist. The latest jobs report from the Bureau of Labor Statistics shows that the U.S. economy added 428,000 jobs in April, 65% of which went to women. At the same time, 181,000 women left the workforce last month – compared to 130,000 men. Additional analysis from the National Women’s Law Center also finds that over 1 million fewer women are working or looking for work, as of April, compared to February 2020.

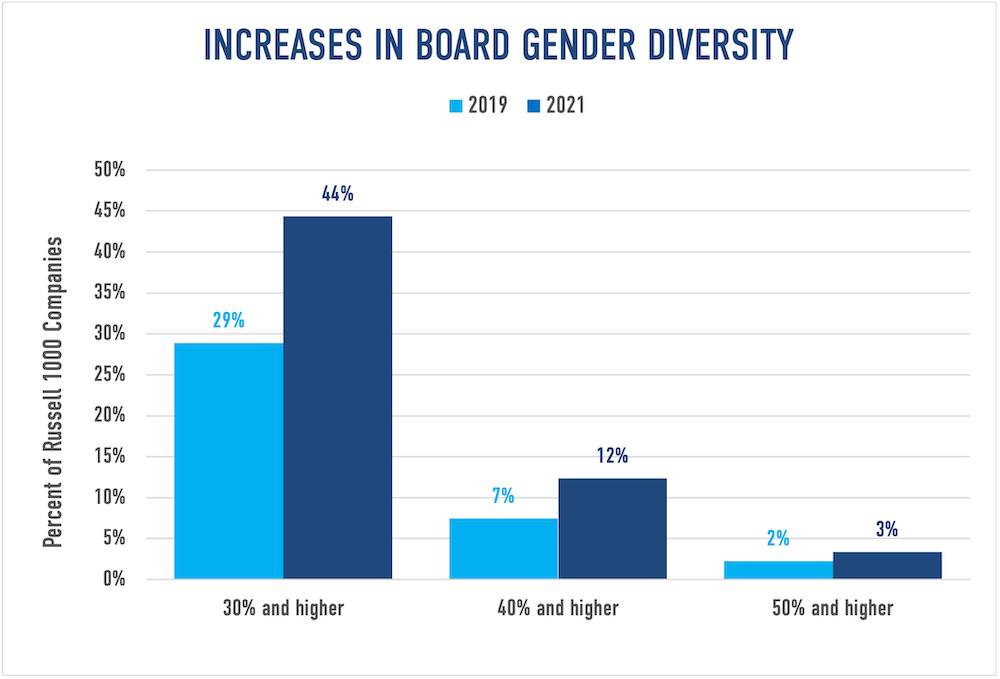

There’s no question women’s economic recovery is lagging. And in a recent survey of the American public we conducted with our partners at SRSS, majorities agreed that women leaving the workforce is bad for the economy (66%), and bad for women’s equality (59%). One area where working women have gained, however, is in board leadership. JUST Capital analysis finds that the average representation of women on Russell 1000 boards rose from 23.8% to 28.2% between 2019-2021 – with gains across representation thresholds of 30%, 40%, and 50%. This is in addition to recent analysis finding women held nearly 27% of Russell 3000 board seats in 2021, up from nearly 24% in 2020.

In light of these gains, we took a closer look at how our 2022 JUST 100 leaders perform on board gender diversity, identifying which companies had the largest percentage of women on their board of directors. We found five companies that have boards comprised of 40% or more (ranging from 43-58%) women – General Motors, Citigroup, Procter & Gamble, Nielsen, and Merck – and at least one board committee chaired by a woman. Each also has a dedicated board committee for environmental, social, and governance (ESG) performance, three of which are chaired by women.

Read on to explore additional ways they’re leading on gender board diversity.

Ranked 2nd in its industry and 30th overall

Automobiles & Parts company based in Detroit, Michigan

With 58% of its board composed of women, General Motors (GM) has one of the most gender-diverse boards of the companies we rank. Women also chair the majority of GM’s board committees, including the Risk and Cybersecurity committee, the Executive Compensation Committee, and the Governance committee. CEO Mary Barra oversees the executive committee and, under her leadership, GM has been a JUST 100 leader for the past five years. Linda R. Gooden leads the company’s Risk and Cybersecurity Committee, which focuses on protecting customers’ data and mitigating potential privacy risks. GM ranks first in its industry for customer privacy as well as first overall for its Customers-related performance among Automobiles & Parts companies.

Ranked 2nd in its industry and 15th overall

Bank based in New York, New York

Citigroup increased its gender board diversity from 50% in 2021 to 58% in 2022 (seven out of 12 members are women). At least one female board member sits on each of Citigroup’s six board committees and Diana L. Taylor is the committee chair for the Nomination, Governance, and Public Affairs Committee. This committee focuses on improving Citigroup’s ESG performance and is responsible for bringing on new board members and ensuring the company is meeting its pledge to have a diverse board. The success of this committee is reflected across our Rankings, as Citigroup earned the number one rank among Banks for its climate commitments and human rights policies as well as for its performance on the Workers stakeholder overall. Citigroup’s prioritization of diversity is not exclusive to its board – the company has also met a three-year goal to increase diversity within its firm, with 40% of women in leadership roles globally.

Ranked 2nd in its industry and 59th overall

Personal Products company based in Cincinnati, Ohio

Procter & Gamble (P&G) currently has a board composed of 50% women. Women chair two of P&G’s board committees and bring expertise in strategy & risk management, marketing, and digital technology to its board overall. Angela Braly is the Chair of the Governance and Public Responsibility Committee, which oversees the evaluation of new board members, and focuses on ESG issues. In 2021, the committee held six meetings to review ESG performance. Patricia A. Woertz chairs P&G’s Audit Committee, overseeing the company’s financial reporting and risk management including information security. P&G is a leader among its industry peers ranking second among Personal Products companies for customer privacy.

Ranked 3rd in its industry and 87th overall

Media company based in New York, New York

Nielsen’s board of directors includes 10 members, five of whom are women, resulting in 50% gender diversity. Nancy Tellem chairs the board’s Compensation and Talent Committee, which includes three women. As Chair, Tellem oversees many issues, including executive compensation, compensation-related disclosure, talent development, and diversity, equity, and inclusion (DEI) engagement. Nielsen places in the top 11% of all companies we rank on workforce demographics disclosure. Lauren Zalaznick chairs the board’s Nomination, and Corporate Governance Committee, which includes oversight of the company’s ESG performance. Nielsen performs well on several issues in the “S” of ESG – it ranks first among all companies we analyze, as well as those within the Media industry, for its performance on human rights and community development Issues.

Ranked 1st in its industry and 26th overall

Pharmaceuticals & Biotech company based in Rahway, New Jersey

Merck has a 43% gender-diverse board, as six of its 14 board members are women. Of these six women, two sit on its Compensation and Management Development Committee, which establishes and maintains equitable compensation and benefits policies. Merck ranks third among Pharmaceutical & Biotech companies for its DEI performance and sixth among the Russell 1000 for its Workers-related performance. Patricia F. Russo, a JUST board member, chairs this committee and Risa J. Lavizzo-Mourey, M.D., a JUST Advisor, also sits on this committee. Merck also ranks in the top 25% of all companies we analyze in CEO-to-Median Worker Pay and is in the top 5% overall, and top-ranked in its industry, on Benefits and Work-Life Balance. Merck’s Governance Committee, which focuses on the company’s ESG efforts, contains three women. Merck’s ESG performance is top-rated in our Rankings, with the company leading the Pharmaceutical and Biotech industry.

Last week, a California judge struck down a law passed in 2018 requiring publicly traded companies headquartered in the state to have at least one woman on their board. The move follows a similar ruling from a judge last month, deeming a state law passed in 2020 requiring companies to meet a quota of at least one racially, ethnically, or otherwise diverse board director unconstitutional. While the decision is a blow to board gender diversity advocates, and the state is expected to appeal it, the law’s impact is already clear. Analysis of board growth among California-based companies in 2021 found that more than half of new board appointees that year were women.

This trend has continued beyond the confines of California-headquartered companies. JUST analysis found that average board gender diversity in the Russell 1000 rose from 23.8% to 28.2% between 2019-2021. When we break these gains down by representation thresholds of 30%, 40%, and 50%, we see gains across each of these groupings. (Figure 1).

In 2021, almost half (44%) of the corporate boards JUST Capital analyzed were composed of at least 30% women. Far fewer boards were composed of 40% or more women and only 3% of boards reached parity or had more than 50% women). Moreover, from 2019-2021, the percent of companies in all three thresholds grew by over 50%. Nevertheless, board diversity still has a long way to go to achieve gender parity, as evidenced by the slow growth in the highest threshold of 50% or more.

While JUST Capital’s analysis shows that board gender diversity has increased substantially at each of the three thresholds in just a two year period, this has not always been the case. Progress on board gender diversity has previously been slow, or even glacial. Between 2012-2017, the share of directors who were women in the S&P 500 rose only five percentage points (from 17% to 22%). But in the last five years, the percent of women in board director seats in the S&P 500 rose by nine percentage points (from 22% to 31%), almost double the increase from 2012-2017.

The success of the board gender diversity movement contains key lessons – around investor pressure, coalition building, and specific asks – that can help accelerate broader pushes for corporate diversity.

Effective shareholder pressure is a major factor behind increased board gender diversity. Beginning in 2017, campaigns from the “big three” institutional investors, BlackRock, State Street, and Vanguard, used their leverage to advance board gender diversity with various voting policies that challenged boards that were not sufficiently gender diverse. Research indicates that this resulted in companies broadening their recruitment efforts for female candidates, electing more women to boards and in board committee chair positions.

To complement institutional investors’ push for board diversity, Nasdaq’s board disclosure rule, which was approved by the SEC in August 2021, marks a different approach to fostering board diversity. Nasdaq’s rule encourages diverse boards by asking companies to publicly disclose their board demographics and, for companies that do not have at least two diverse directors (diverse defined as women, belonging to an underrepresented racial or ethnic group, or as LGBTQ+), to explain why that remains the case. Nasdaq’s rule pushes for greater transparency and standardized reporting gives investors increased insight into various demographic indicators of directors.

And this approach has seen success. Speaking at a JUST Capital event, Nasdaq SVP and Head of U.S. Listings and Revenue Karen Snow said that prior to the rule about 25% of the S&P 500 disclosed their board demographics and now over 60% have disclosed. “It’s about taking leadership now and presenting guidelines that might help investors and others in the community understand what you’re doing,” she said. To Snow, the rule’s focus on disclosure, over quotas, has helped see progress from companies. A similar approach to other forms of diversity disclosure, including workforce demographics, could help accelerate transparency from corporate America.

While investor engagement influenced companies to appoint more women to their boards, advocacy organizations were crucial in elevating board gender diversity as a priority for investors. The 30% Club, originating in the U.K. in 2010 and expanded internationally, and the 30 Percent Coalition, founded in the U.S. in 2011, successfully developed coalitions between investors, board members, and corporate governance experts to champion board gender diversity.

Additionally, women-led networking organizations played a role in helping companies find new board leadership talent. Equilar’s Diversity Network partners, the organization’s consortium to advance board diversity, contains several women-led networking groups, some of which are regional or university-based. Women Corporate Directors and Athena Alliance, two other diversity network partners, provide education and coaching to women as well as networking opportunities to increase their likelihood of joining a corporate board.

Another lesson that can be applied to pushes for corporate diversity is that targets are helpful, but less ambitious targets will lead to less ambitious achievements. In much of the advocacy efforts surrounding board gender diversity, 30% is cited as the target threshold and has even been used to brand certain organizations, as seen in the 30% Club and 30 Percent Coalition. Some view 30% as the critical mass where underrepresented groups can impact boardroom dynamics and has been embraced by investors as the recommended percent of gender diversity on a board.

Other groups have evolved to set more ambitious goals for board gender diversity, and they argue that the percent of women in corporate boardrooms should be more representative of the population. 50/50 Women on Boards, for example, now advocates for gender parity on boards of Russell 3000 companies after achieving its initial goal of 20% women directors in 2020. Some may think 50% or greater board gender diversity is asking too much of companies, but JUST Capital’s data shows that companies within the JUST 100 are more than twice as likely to have 50% or greater board gender diversity than their Russell 1000 peers. However, as Figure 1 above shows, companies with this level of board gender diversity remain very rare.

In addition to setting targets, it is also important to consider intersectional pushes for diversity. Importantly, not all women have benefited equally from pushes for board gender diversity. In 2020, white women held over three times as many board seats as women of color in the Fortune 500. As discussed in a 2021 JUST analysis of board diversity, advocacy groups for racial/ethnic representation can help these efforts. But because historical movements around board gender diversity did not take race into consideration from the start, their efforts have led to unequal advances for women. The elevation of board racial/ethnic diversity for companies is crucial for expanding board diversity beyond gender and ensuring that white women are not the primary beneficiaries of diversity pushes.

And while we continue to see a rise in board gender diversity, it is important to not conflate that success with women’s progress overall in corporate America. Recent data shows women are woefully underrepresented in the C-Suite, and perhaps even more alarmingly, female executives are still experiencing the same kinds of gender discrimination that plague women at every rung of corporate America. Investors and advocacy groups should expand their diversity focus beyond the board level. Campaigns for C-suite diversity and other levels of leadership have the potential to create more equitable representation at the top, and other efforts can push for similar outcomes across a company’s entire workforce.

Board gender diversity in corporate America is continuing to increase, but it’s taken a decade of sustained efforts from multiple groups to achieve that success. The lessons learned over that period of time can, and should, be leveraged to help accelerate broader efforts to diversify the ranks of corporate America.