This report was written by Mona Patni, Director of Quantitative Research & Analytics.

Stocks extended their rally in the second quarter, boosted by cooling inflation, the prospect of a shift in monetary policy, and enthusiasm over artificial intelligence, with the bulk of the gains made in June. The Russell 1000 Index was up 8.6% in Q2 2023, bringing its YTD return to 16.67%. With respect to sector performance, IT companies led the stock market advance in the quarter, while the consumer discretionary and communication services sectors also performed strongly. Underperforming sectors included energy and utilities.

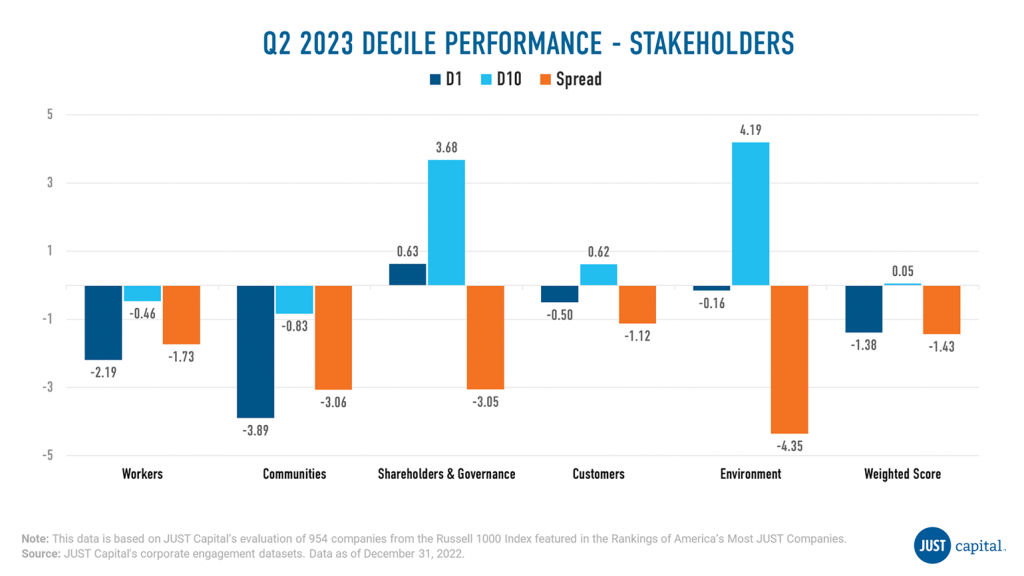

JUST Capital found that all five stakeholders we track delivered negative performance in Q2 2023. However, over the longer term from Jan 2018 to June 2023, the leaders have outperformed the laggards by 52.13% as measured by JUST Overall Score. In Q2 2023, the Customers stakeholder delivered the strongest performance over this period with a long-short spread of -1.12%, while the Environment stakeholder fared most poorly at -9.11%. Within the Customers and Environment stakeholders, underperformance was driven by both deciles, with the top decile underperforming and bottom decile outperforming. For the Workers and Communities stakeholders, underperformance was driven by the top decile, whereas for the Shareholders & Governance stakeholder underperformance was driven by the bottom decile.

JUST Capital’s Overall Weighted Score takes into account the 20 core Issues determined through our survey research – including paying a living wage, creating a diverse, inclusive workplace, and helping combat climate change – across key business stakeholders: Workers, Communities, Shareholders & Governance, Customers, and Environment. This Overall Weighted Score had a negative long-short spread of -1.43% over the period ending June 30, 2023 which was an improvement from Q1 2023 at -7.14%, but still not positive.

Negative contribution to the top decile of the Overall Weighted Score was driven primarily by the Industrials and Consumer discretionary sectors. Basic Materials, Real Estate, and Technology companies were positive contributors to the top decile. Overweight stocks like Illumina (-19.38%) and Target (-19.82%), and underweight companies like Carvana (164.76%), didn’t help the performance of the top decile of the Overall Weighted Score. On the other hand, the bottom decile, which consists of low performers as measured by stakeholder performance, delivered close to neutral performance. Negative contributions largely came from Financials and Health Care names, while bottom decile companies like Carnival Corp (Consumer Discretionary) and Builders FirstSource Inc (Industrials) rallied during this quarter.

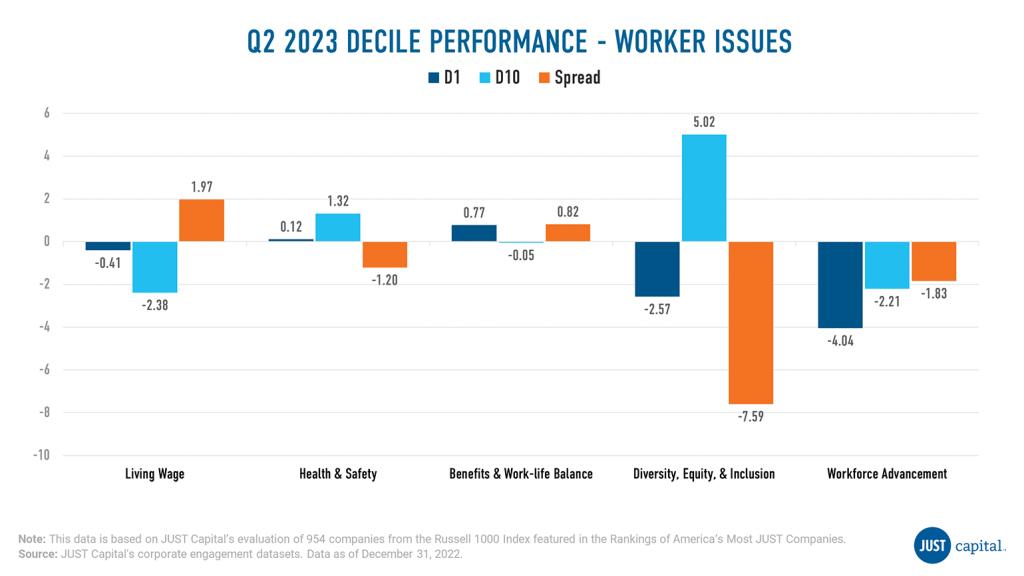

The Workers stakeholder measures a company across five Issues:

In Q2 2023, we saw Living Wage and Benefits Issues deliver positive performance whereas DEI fared most poorly. Underperformance in DEI & Workforce Advancement was driven by negative performance from both top and bottom decile companies, whereas negative performance in Health & Safety came from bottom decile names.

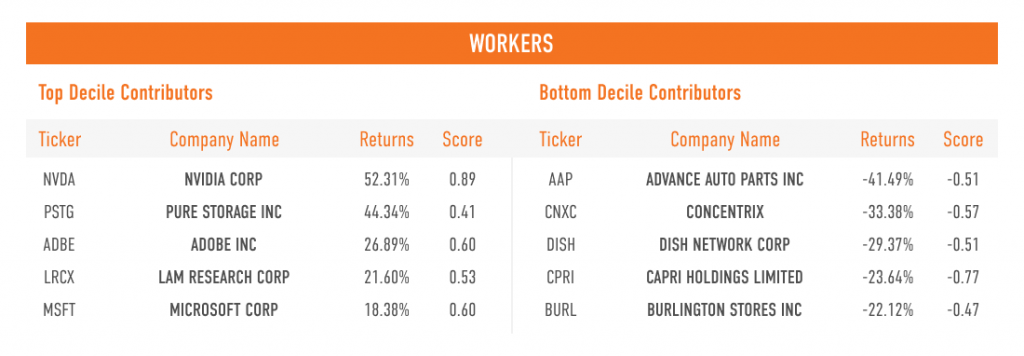

Shown below are the top and bottom five contributors to the top decile (D1), the top-ranked companies as measured by their Workers score, and the bottom decile (D10), the lowest-ranked companies as measured by their Workers score.

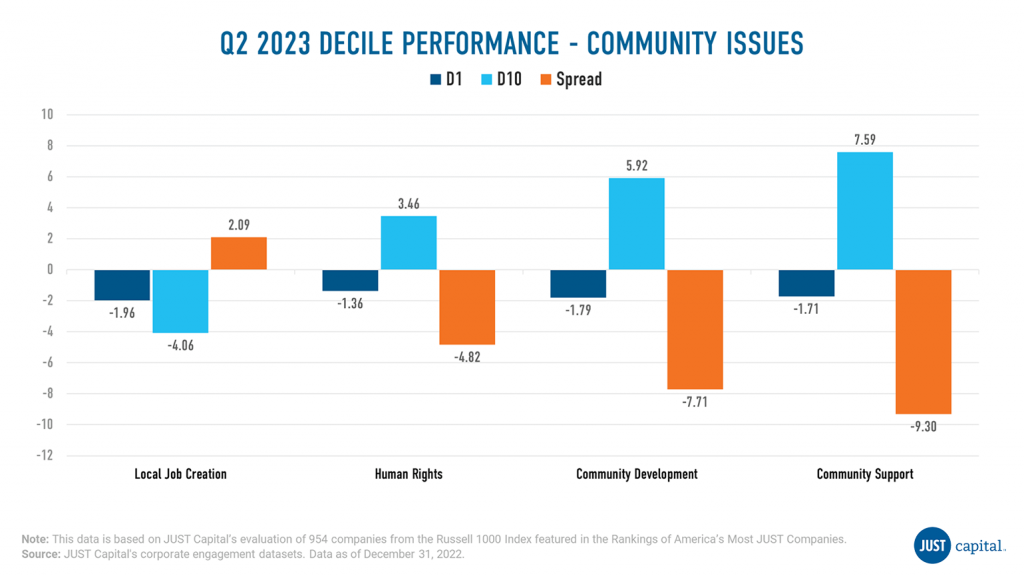

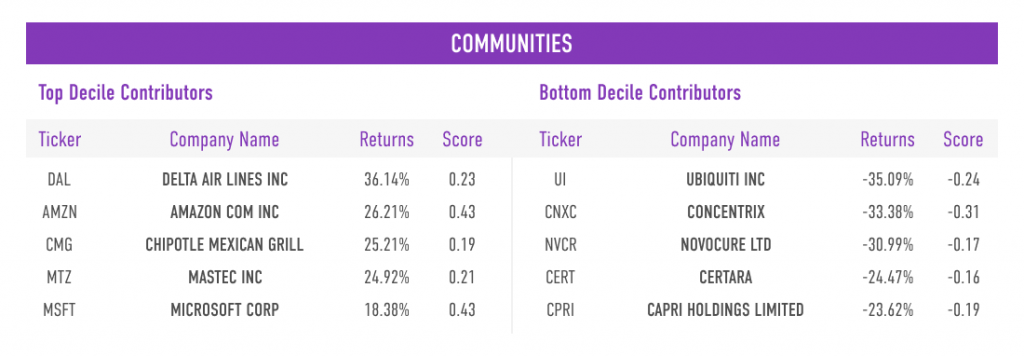

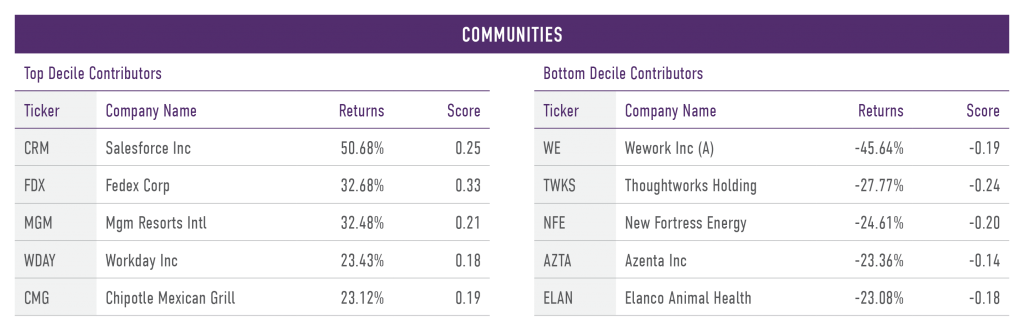

The Communities stakeholder measures a company across four Issues:

Community Support was the weakest performer followed by Community Development and Supply Chain, with negative contributions coming from both top and bottom decile companies.

Shown below are the both top and bottom five contributors to the top decile (D1), the best-ranked companies as measured by their Communities score, and the bottom decile (D10), the lowest-ranked companies as measured by their Communities score.

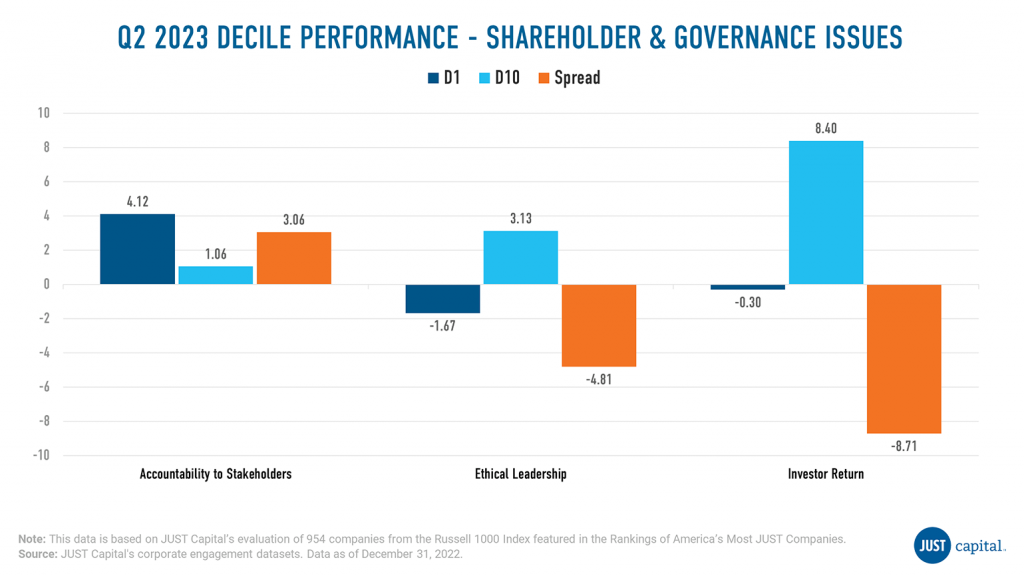

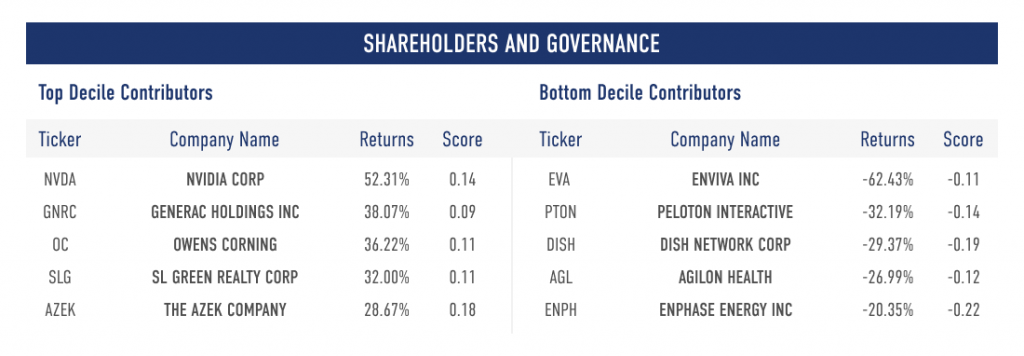

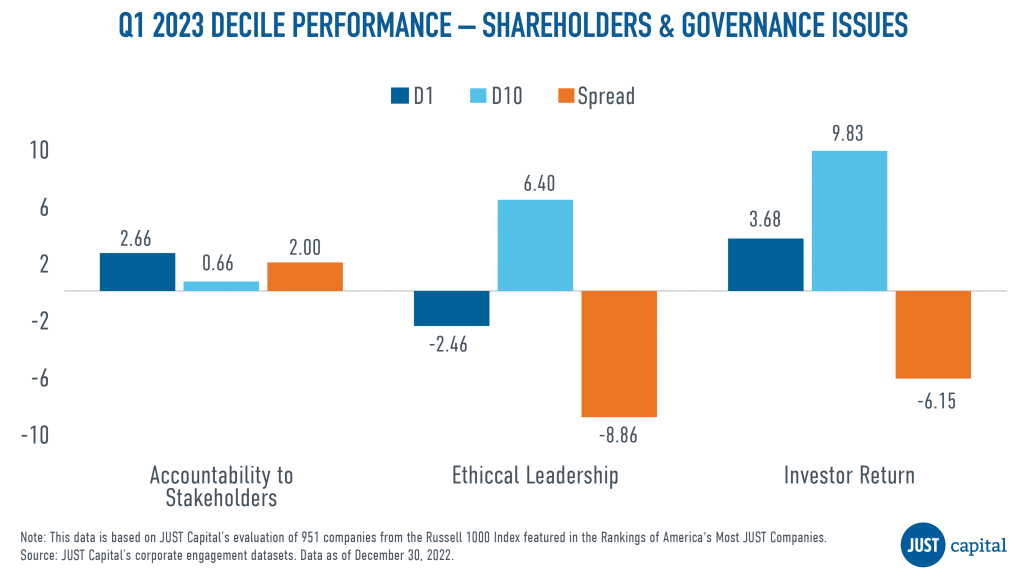

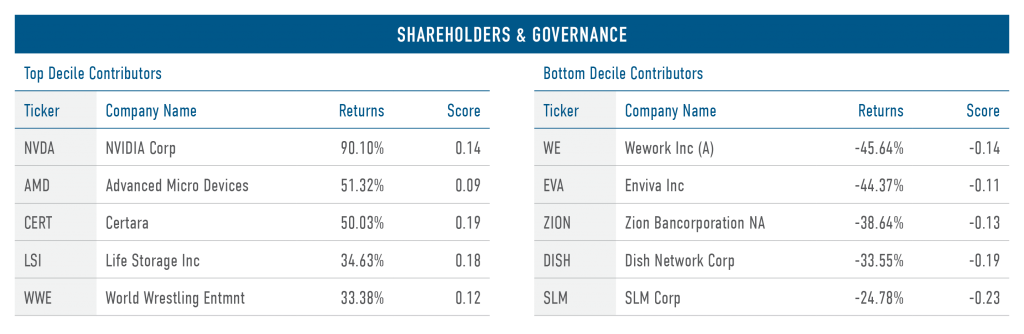

The Shareholders and Governance stakeholder measures a company across three Issues:

In Q2 we saw the Accountability to Stakeholders Issue deliver positive performance, with a long-short spread of 3.1%, whereas Ethical Leadership and Investor Return performance was negative.

Shown below are both the top and bottom five contributors to the top decile (D1), the best-ranked companies as measured by their Shareholders and Governance score, and the bottom decile (D10), the lowest-ranked companies as measured by their Shareholders and Governance score.

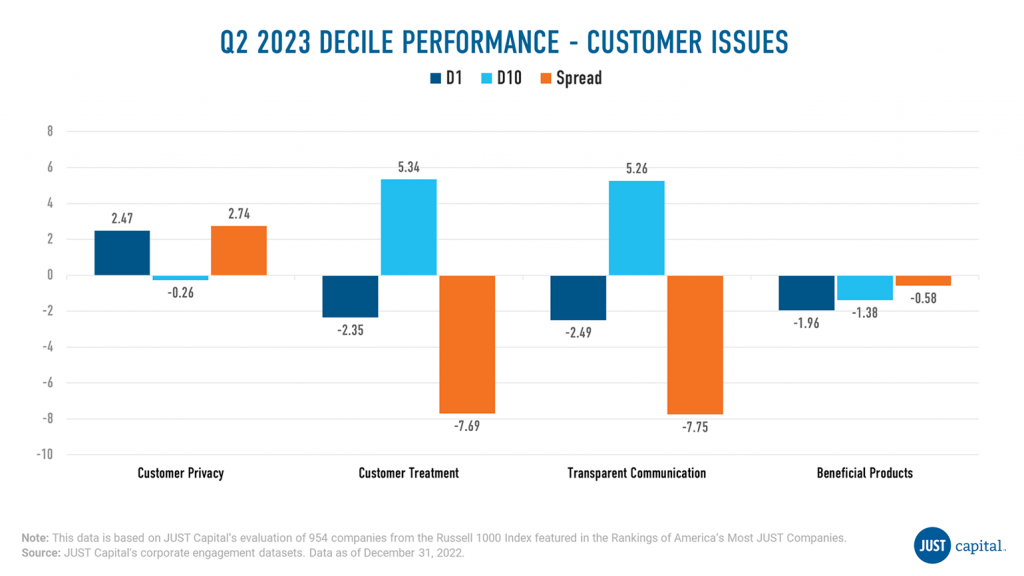

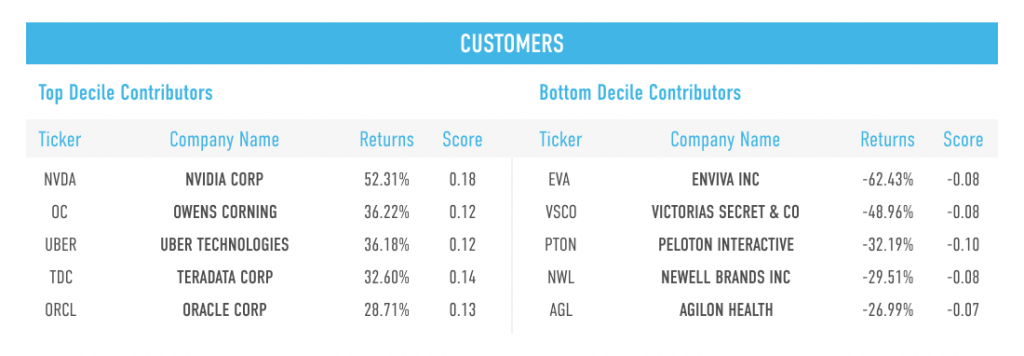

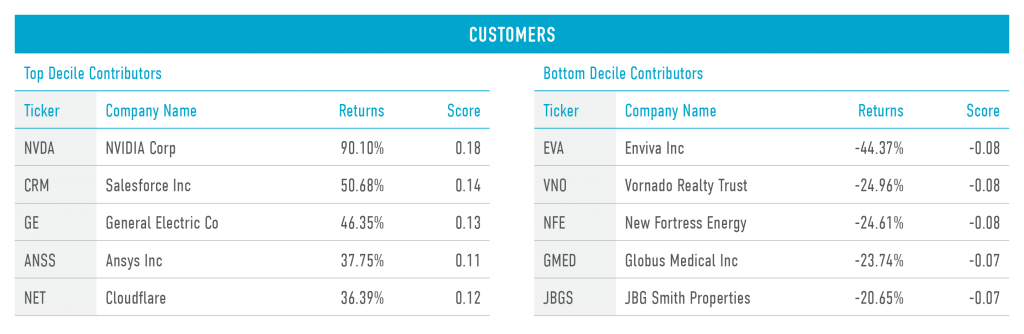

The Customers stakeholder measures a company across four Issues:

In Q2 2023, we saw Customer Privacy outperform the other Customer Issues, with a long-short spread of 2.7%. Beneficial Products, Customer Treatment, and Transparent Communication were negative contributors to Customers performance.

Shown below are both the top and bottom five contributors to the top decile (D1), the best-ranked companies as measured by their Customers score, and the bottom decile (D10), the lowest-ranked names as measured by their Customers score.

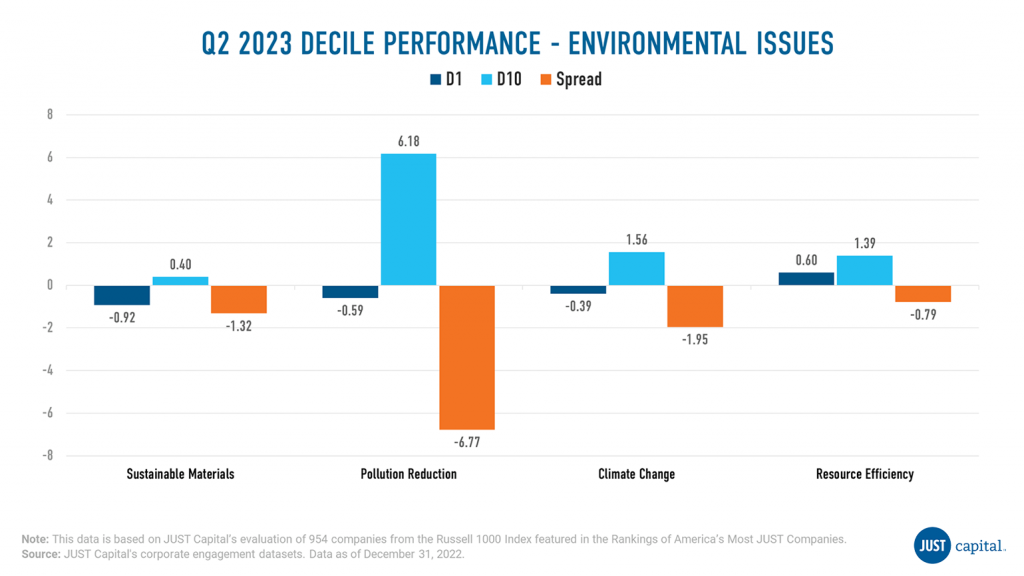

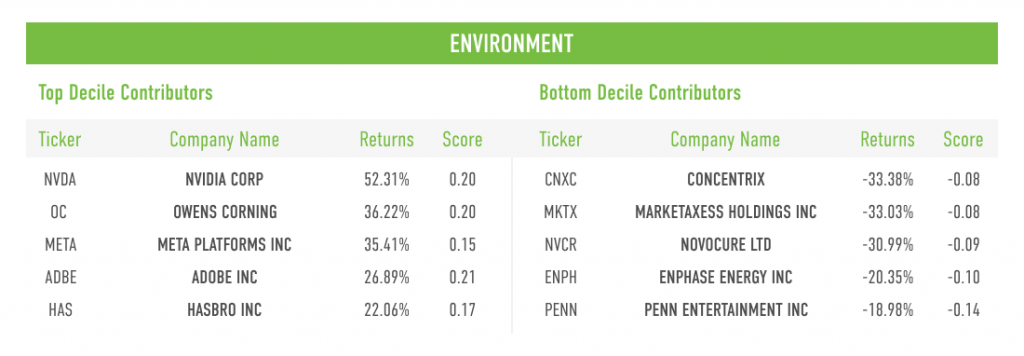

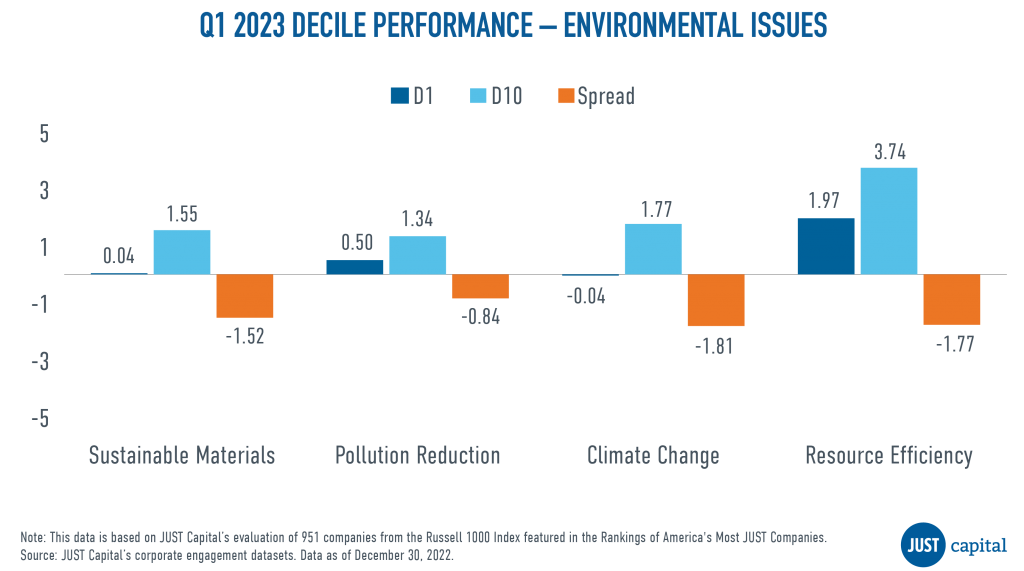

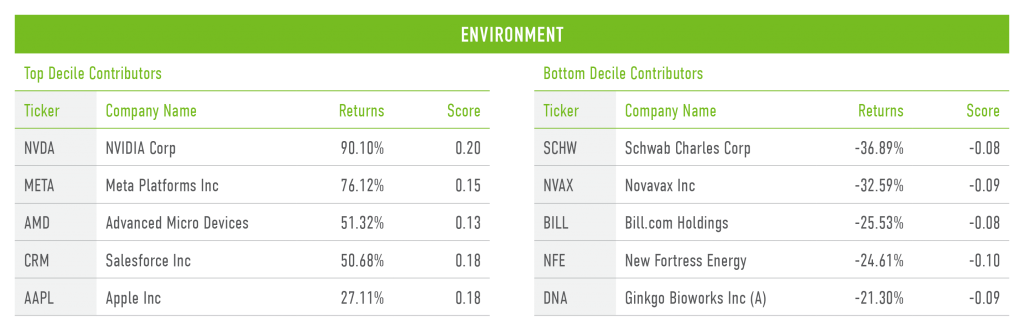

The Environment stakeholder measures a company across four Issues:

In Q2 2023, we saw all Environment Issues deliver negative performance, with Pollution Reduction being the weakest.

Shown below are both the top and bottom five contributors to the top decile (D1), the best-ranked companies as measured by their Environment score, and the bottom decile (D10), the lowest-ranked companies as measured by their Environment score.

Computation Methodology

We monitor the performance of these stakeholders and Issues on a long-short basis. The long and short portfolios are selected based on the factor scores as the top and bottom deciles within the universe of companies we track in the Russell 1000. Top decile (D1) companies are those that rank highest based on the factor score, and bottom decile (D10) companies are those that rank lowest based on the factor score.

D1 Performance is computed as:

(Equally weighted average of returns of stocks in D1 bucket) – (Equally weighted average of returns of all stocks within the Universe)

D10 Performance is computed as:

(Equally weighted average of returns of stocks in D10 bucket) – (Equally weighted average of returns of all stocks within the Universe)

Spread is computed as:

D1 Performance – D10 Performance

Written by Cambria Allen-Ratzlaff and Mona Patni

Today, we’re excited to celebrate a very special milestone. The JUST ETF – which we launched in 2018 in partnership with Goldman Sachs Asset Management to track the top 50% of Russell 1000 companies according to the priorities of the American public – is turning five.

Just’s mission is to demonstrate that just business is better business, by incentivizing America’s largest companies to deliver on the priorities of the public. And a key part of achieving that aim is to drive financial capital toward companies that best serve the needs and expectations of their workers, customers, communities, and the environment.

That capital comes from shareholders – from families saving for their kids’ college to large institutions safeguarding pensions and healthcare for our teachers, municipal workers, and police officers – who provide money to firms through equity and debt financing. This money is then used by companies to power their businesses. Without it, companies couldn’t create good jobs, build the best products and services, support strong communities, and continue to innovate and grow.

Financial capital has played a crucial role in developing America’s economy – including the growth of largest public companies in the Russell 1000, which collectively represent 93% of the U.S. public equity market. So what if we could measure how good individual companies are for America, using Americans’ own voices as the measuring stick – and then see how the companies that are best for workers, customers, communities, and the environment actually perform for their investors? In other words, can just companies create competitive value for shareholders, too?

The answer is a resounding yes. On June 7, 2018, we launched the Just ETF, powered by our proprietary Just U.S. Large Cap Diversified Index (JULCD). The JULCD represents the top half of companies in Just Capital’s Rankings of America’s Most JUST Companies, by industry, and has outperformed the Russell 1000 by 8.78% since inception through May 31, 2023. If you invested $100 in the fund at launch, you would have nearly $220 in your pocket today.

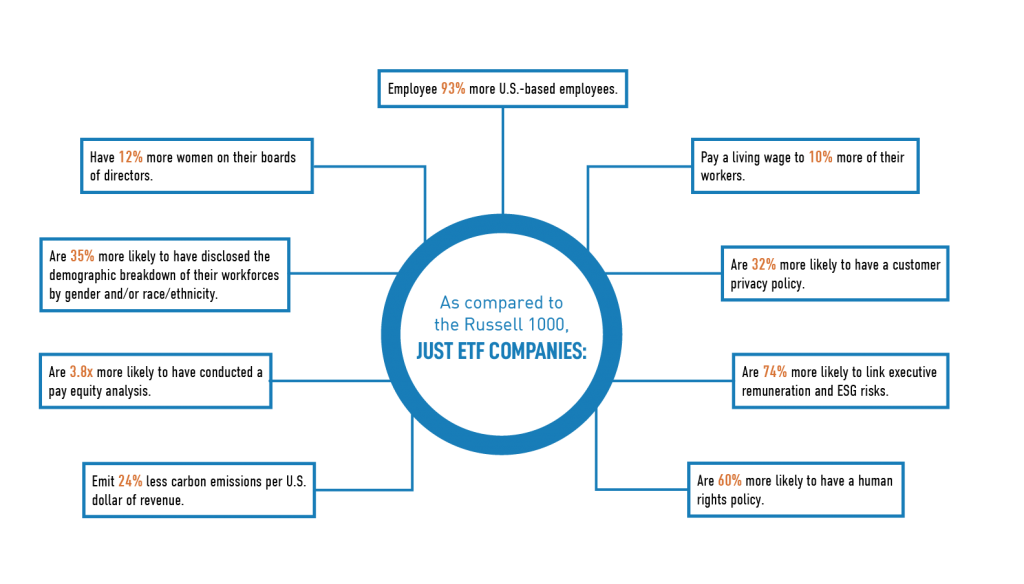

These companies not only outperform in the market but are leaders when it comes to the priorities of the American public. In our six years of survey research, we have found that Americans are remarkably united in what they want companies to prioritize: workers, wages, and jobs. Paying a fair and living wage is the most important priority across all demographic groups, followed by creating jobs in their communities. Americans also expect companies to behave ethically, serve their customers with beneficial, safe products, and act as responsible stewards of the environment and the communities in which they operate.

In this regard, the JUST ETF also delivers concrete impact. Companies in the JUST ETF are innovative and can quickly adapt in response to risks and opportunities impacting their businesses, while protecting and strengthening brand value.

The JUST ETF is a live accounting of how companies that deliver value for their workers, customers, communities, and the environment, deliver value for their shareholders, as well. These are the companies that understand they are of society, not apart from society.

As we look ahead to the next five years of the Just ETF and beyond, we remain committed to demonstrating the value of just corporate leadership, as defined by the voice of the American public.

The Investor Solutions team at Jist Capital continues to expand the suite of products tracking our in-depth company research and polling of the American public. We firmly believe that together we can create a more just and equitable marketplace that works for all Americans. Please reach out using this request form below if you have an interest in partnering with us to launch your next innovative large-cap public equity or fixed income strategy.

Note: Tracking Error of JUST ETF vs JUST U.S Large Cap Diversified (JULCD) Index is 0.1 as of March 31 2023 over 1 year.

The information contained herein is for informational purposes only without regard to any particular user’s investment objectives, risk tolerances or financial situation and does not constitute investment advice, nor should it be considered a solicitation or offering to investors residing outside the United States. JUST Capital makes no representation as to the advisability of investing in any investment fund or other vehicle. Shares of JUST are made only by prospectus. The addition, removal, or inclusion of a security in any JUST Capital index is not a recommendation to buy, sell, or hold that security, nor is it investment advice. The JUST Parties do not in any way sell, sponsor, support, promote, or endorse any securities based on the JULCD, or have any involvement in their operations or distribution. Prospective investors should not make a decision to invest in any investment fund or other vehicle based on the information contained in this website, and JUST Capital shall not be responsible or liable for any advice given to third parties or decisions to invest in any investment fund or other vehicle by you or third parties based on the information. Index performance does not reflect the deduction of any fees or expenses. Past results of the JUST U.S. Large Cap Diversified Index are no guarantee of future performance.

The JUST US Large Cap Diversified Index is calculated and maintained by FTSE Russell using the Russell 1000 Index as a starting universe, and aims to reflect the performance of a JUST Capital Foundation Inc. methodology. FTSE Russell does not sponsor, endorse, sell, or promote any investment vehicle that is offered by any third party that seeks to provide an investment return based on the performance of any index. It is not possible to invest directly in an index.

This report was written by Mona Patni, Director of Quantitative Research & Analytics.

After a year of volatility and uncertainty, U.S. stocks gained during the first quarter of 2023 in a surprise show of resilience despite a banking crisis, cryptocurrency meltdowns, and plenty of uncertainty around interest rates. The Russell 1000 index concluded a turbulent first quarter of 2023 to rise around 7%, while the tech-heavy Nasdaq Composite proved to be the real standout, soaring nearly 17%. With respect to sector performance, seven of the 11 large-cap sectors were higher, led by Technology and Communications while stocks in the energy and healthcare sectors lagged the most over the quarter.

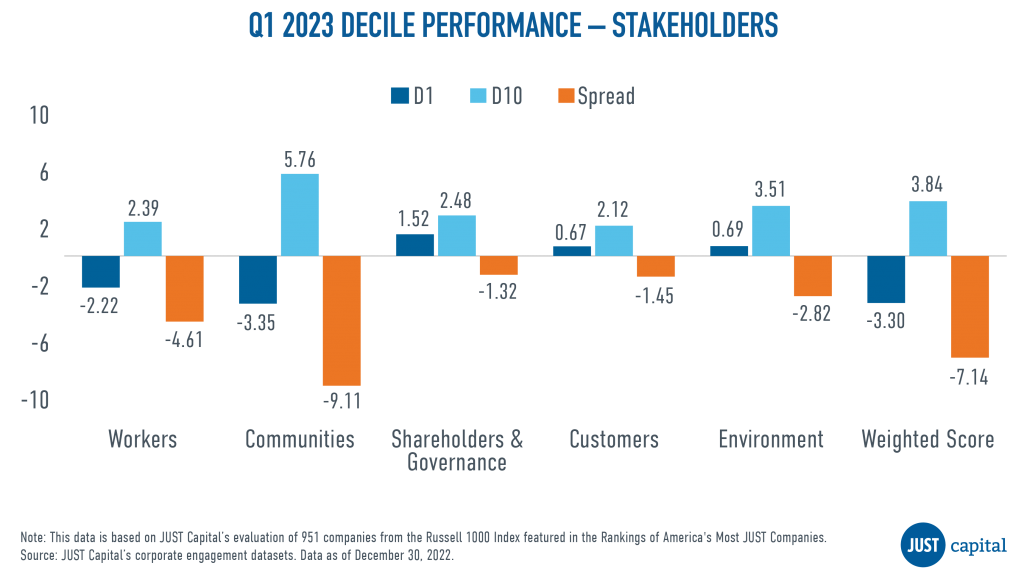

Although the JUST Overall Weighted Score has outperformed the Russell 1000 by 50.67% from Jan 2018 to March 2023, JUST Capital found that all five stakeholders we track delivered negative performance in Q1 2023, primarily driven by negative contribution from the Financials sector. The Shareholders and Governance stakeholder delivered the best performance over this period with a long-short spread of -1.32%, while Communities stakeholder fared the worst at -9.11%. Within the Workers and Communities stakeholders, underperformance was driven by both deciles, with the top decile underperforming and bottom decile outperforming. For the remaining stakeholders, underperformance was driven by the bottom decile.

JUST Capital’s Overall Weighted Score takes into account the 20 core Issues determined through our survey research – including paying a living wage, creating a diverse, inclusive workplace, and helping combat climate change – across key business stakeholders: Workers, Communities, Shareholders and Governance, Customers, and Environment. This Overall Weighted Score had a negative long-short spread of -7.14% over the period ending March 31, 2023.

Negative contribution in the top decile of the Overall Weighted Score was driven primarily by both allocation and selection within the Financials sector. Overweight in Financials was driven by banks outperforming other industries on the Local Job Creation, Resource Efficiency, and Living Wage Issues, which together make up more than 33% of our model.

Owning stocks like First Republic Bank (-88.9%) and Comerica (-33.98%) didn’t help the performance of the top decile of the Overall Weighted Score. Following the failures of Silicon Valley Bank and Signature Bank, which led to broader concerns about industry liquidity, regional banks’ (especially First Republic Bank’s) stock price came under pressure due to exposure to venture capital and a large amount of uninsured deposits, similar to the failed banks. On the other hand, the bottom decile, which consists of low performers, counter-intuitively outperformed the Russell 1000. Negative contributions largely came from Industrials and Technology names. Bottom decile companies like Vontier (Industrials) and Universal Display Corp (Technology) rallied during this quarter.

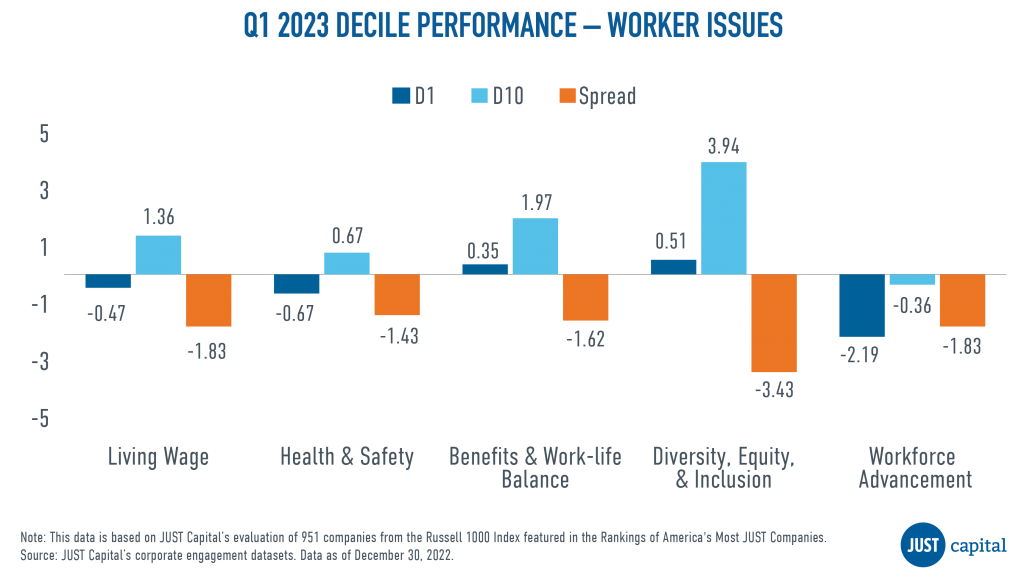

The Workers stakeholder measures a company across five Issues:

In Q1 2023, we saw all the Worker Issues underperform. Underperformance in Living Wage and Health & Safety was driven by negative performance from both top and bottom decile companies.

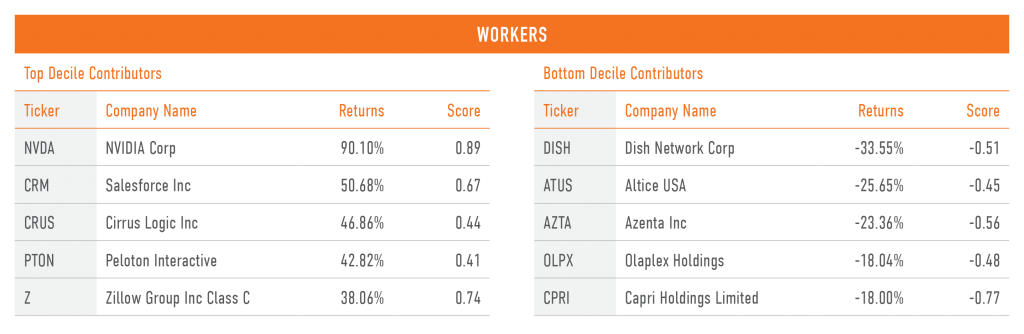

Shown below are the top and bottom five contributors to the top decile (D1), the top-ranked companies as measured by their Workers score, and the bottom decile (D10), the lowest-ranked companies as measured by their Worker score.

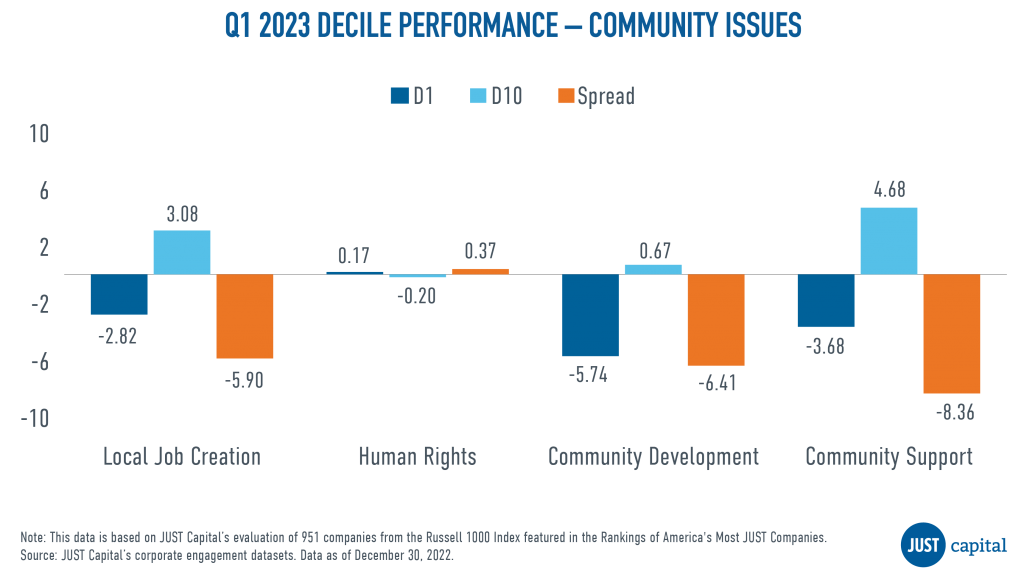

The Communities stakeholder measures a company across four Issues:

Community Support was the weakest performer followed by Community Development and Local Job Creation, with negative contribution coming from both top and bottom decile companies.

Shown below are the both top and bottom five contributors to the top decile (D1), the best-ranked companies as measured by their Communities score, and the bottom decile (D10), the lowest-ranked companies as measured by their Communities score.

The Shareholders and Governance stakeholder measures a company across three Issues:

In Q1 we saw the Accountability to Stakeholders Issue deliver positive performance, with a long-short spread of 2%, whereas Ethical Leadership and Investor Return stakeholder performance was negative.

Shown below are both the top and bottom five contributors to the top decile (D1), the best-ranked companies as measured by their Shareholders and Governance score, and the bottom decile (D10), the lowest-ranked companies as measured by their Shareholders and Governance score.

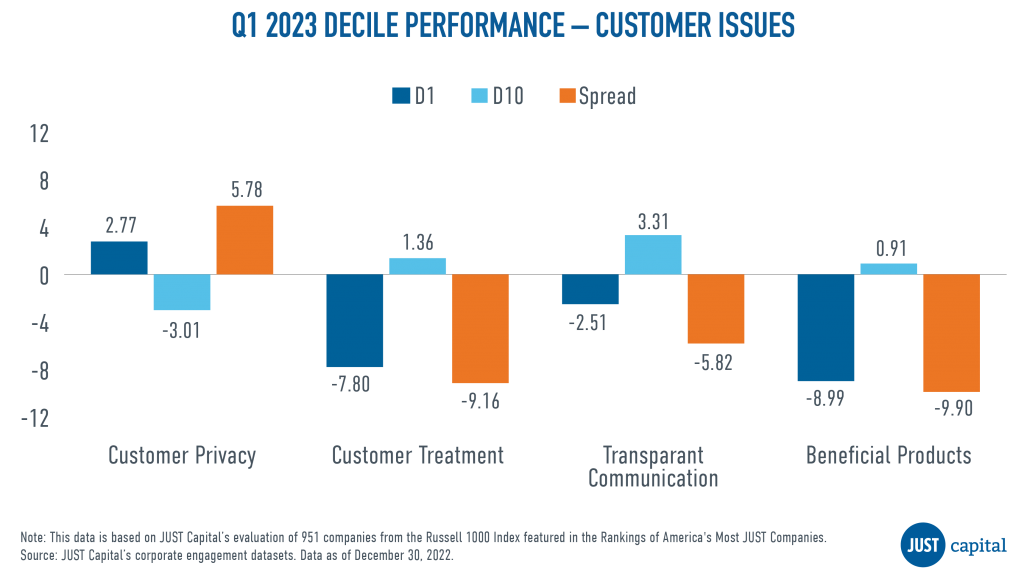

The Customers stakeholder measures a company across four Issues:

In Q1 2023, we saw Customer Privacy outperform the other Customer Issues, with a long-short spread of 5.78%. Beneficial Products, Customer Treatment, and Transparent Communication were negative contributors to Customer performance.

Shown below are the both top and bottom five contributors to the top decile (D1), the best-ranked companies as measured by their Customer score, and the bottom decile (D10), the lowest-ranked names as measured by Customer score).

The Environment stakeholder measures a company across four Issues:

In Q1 2023, we saw all Environment Issues deliver negative performance with Pollution Reduction outperforming other Environment Issues. Resource Efficiency, Sustainable Materials, and Climate Change delivered negative performance in this quarter.

Shown below are the both top and bottom five contributors to the top decile (D1), the best-ranked companies as measured by their Environmental score, and the bottom decile (D10), the lowest-ranked companies as measured by their Environmental score.

Computation Methodology

We monitor the performance of these stakeholders and Issues on a long-short basis. The long and short portfolios are selected based on the factor scores as the top and bottom deciles within the universe of companies we track in the Russell 1000. Top decile (D1) companies are those that rank highest based on the factor score, and bottom decile (D10) companies are those that rank lowest based on the factor score.

D1 Performance is computed as:

(Equally weighted average of returns of stocks in D1 bucket) – (Equally weighted average of returns of all stocks within the Universe)

D10 Performance is computed as:

(Equally weighted average of returns of stocks in D10 bucket) – (Equally weighted average of returns of all stocks within the Universe)

Spread is computed as:

D1 Performance – D10 Performance

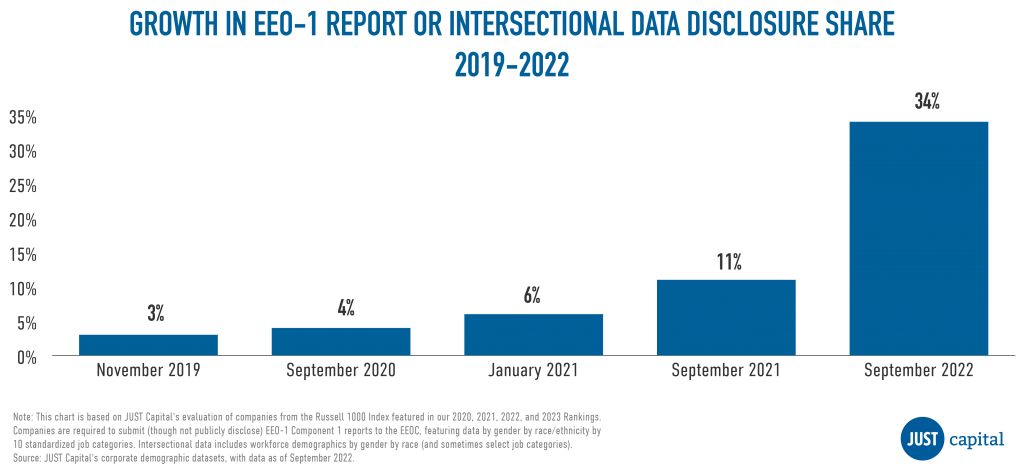

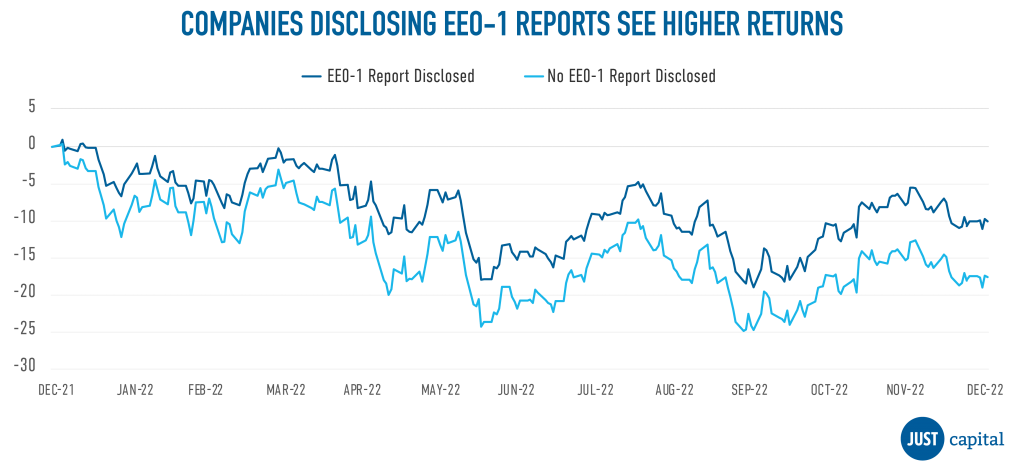

As diversity, equity, and inclusion (DEI) becomes an increasingly urgent priority in the U.S., the expectation is growing for corporate leaders to take meaningful action to advance racial equity in the workplace. Our survey research shows that DEI Issues remain a key element of just business behavior, with 92% of Americans saying that it is important for companies to promote racial equity in the workplace and 76% agreeing that reporting workforce demographics is a critical step toward doing so. With 68% of Americans agreeing that companies have more work to do on these issues, we are seeing that – when it comes to demographic disclosure – more and more companies are in fact stepping up to the plate.

In our own recent analysis, we found that the number of Russell 1000 companies that publicly disclose intersectional data detailing gender, race, and ethnicity by job category from their EEO-1 reports or equivalent – has grown substantially, from 3% in 2019 to 34% in 2022.

In addition to the American public, investors want to see more of this kind of action as well. Public disclosure of EEO-1 data can promote transparency and accountability, and help investors understand how much progress companies are making in their commitments to increase representation at all job levels. NYC’s Comptroller’s Office and New York City Retirement Systems (NYCRS) have been on the forefront of a successful three-year campaign to push companies to make disclosure of EEO-1 reports the norm. (Watch this video featuring JUST Capital, NYCRS, CalSTRS, and Bloomberg discussing that work). In the last three years, shareholders have endorsed proposals at nine companies to increase diversity and EEO-1 reporting with an average of 54% support, nearly double the general average support for social proposals of 29%.

To build the business and investor case for tracking workforce diversity data we looked specifically at the subset of companies that disclose EEO-1 or equivalent data, and found that they delivered higher returns than those that didn’t disclose an EEO-1 report or equivalent, outperforming by 7.9% over the trailing one-year period ending in 2022.

By encouraging companies to disclose their EEO-1 reports, investors can help promote transparency and accountability around workplace diversity and inclusion. Doing so benefits workers, communities, and society as a whole, but also crucially helps investors make more informed decisions about which companies to invest in, as research has shown that companies with diverse workforces and leadership teams tend to perform better financially.

Companies are heading in the right direction, with more and more disclosing demographic data each year. But with just one-third of America’s largest companies publishing their EEO-1 reports, there’s still a long way to go. Investors play a key role in incentivizing corporate leaders to prioritize demographic disclosure – helping to build a just and inclusive economy that truly works for all.

If you are interested in supporting our philanthropic mission by licensing our unique data, we are happy to discuss data needs, index licensing, and other ways we can partner. Please reach out to Manager, Investor Market Solutions, Michael Wirtz, at mwirtz@justcapital.com.

This report was written by Mona Patni, JUST Director of Quantitative Research & Analytics.

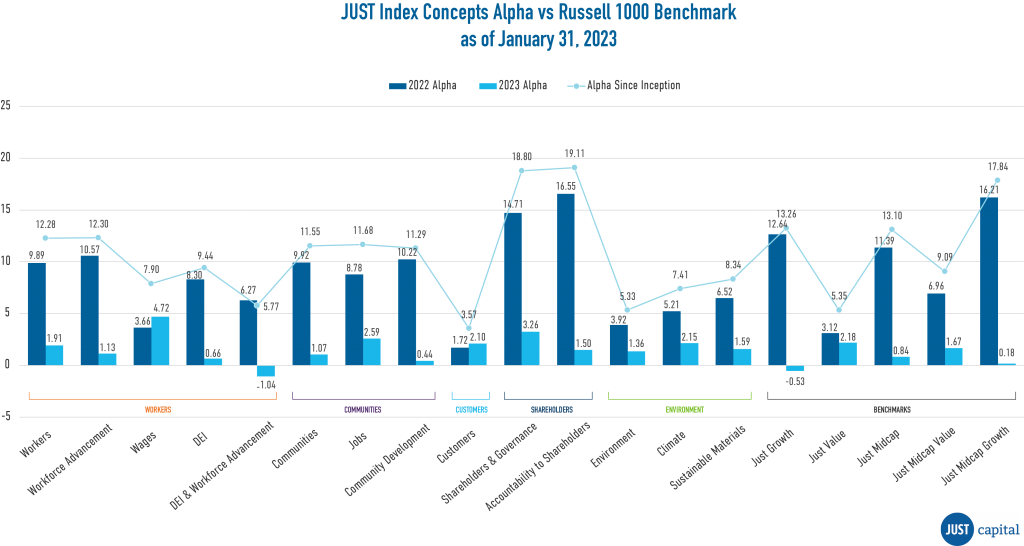

Each index concept has outperformed its benchmark since inception, with the Accountability to Stakeholders index concept focused on good governance generating over 19% alpha.

As part of our ongoing work to build the business and investor case for just business behavior, Just Capital has released 19 new index concepts that demonstrate the power of investing in companies at the forefront of stakeholder value creation.

Each concept features companies that score in the top 20% of our Rankings of America’s Most Just Companies, which evaluate how the nation’s largest corporations perform on the Issues that matter most to Americans today. Each concept demonstrates that investors need not sacrifice returns to support companies doing right by all their stakeholders.

Incepted on December 31, 2021, each concept has over a year’s worth of performance history, and to date, each one of them has outperformed the Russell 1000 benchmark with alpha ranging between 3.6% to 19.1%. The chart below demonstrates that throughout 2022 and even in January 2023, the indexes have continued to outperform and generate alpha:

Just Capital’s full slate of index concepts include:

The top performing index since inception is the Accountability to Stakeholders Index with 19.1% Alpha. This issue index highlights the financial performance and impact of investing in companies that prioritize good governance with diverse, independent boards that oversee corporate performance on key environmental, health, safety, and social matters. JUST Capital’s “Prioritize accountability to all stakeholders” Issue accounts for 2.1% of a company’s score in our Rankings of America’s Most JUST Companies, and covers three metrics encompassing 10 data points, tracking Board Independence, Board Diversity, and Board Oversight of JUST Issues, including if ESG-related performance is linked to compensation for employees and executives.

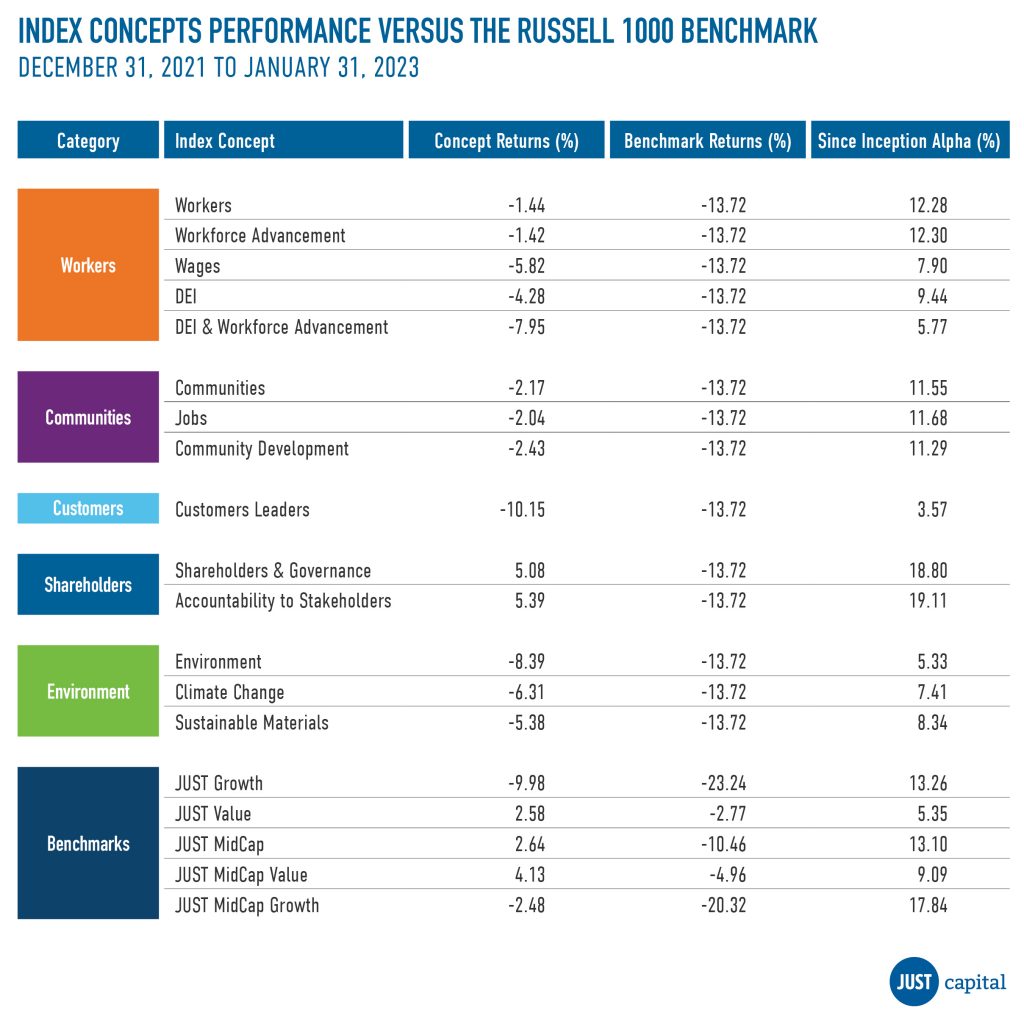

The table below illustrates the cumulative performance and related alpha for all 19 indexes against their benchmarks from December 31, 2021 to January 31, 2023:

Explore additional top performing indexes within the other stakeholder and benchmark groups below and visit our microsite to explore all related charts and data.

Outperforming Index Concept: Workforce Advancement Leaders

Since Inception Alpha vs. Russell 1000 Benchmark: 12.3%

According to JUST Capital’s survey research, Americans identified Workforce Advancement as one of the top Issues companies should prioritize, and our data set tracks corporate performance on five data points: Average Hours of Training or Career Development Per Employee, Career Opportunities Rating, Tuition Reimbursement, Retention Rate, and Internal Hiring Rate. This concept tracks the financial performance and social impact of an intersection of companies in our Rankings that prioritize upward mobility and the professional advancement of their workforces. The Workforce Advancement Issue accounts for 7.1% of a company’s score in our Rankings of America’s Most JUST Companies.

Compared to the Russell 1000, Workforce Advancement Leaders Are:

Outperforming Index Concept: Jobs Leaders

Since Inception Alpha vs. Russell 1000 Benchmark: 11.6%

Americans agree that companies should serve their communities where they operate, and this concept helps investors track the performance of companies that prioritize job creation within those communities. Our data set covers four key Issues encompassing 42 data points, including Employee-Led Giving and Volunteering, Opportunities for Local Businesses, Local School Support, Percent of U.S. Jobs Created, and more. The Local Job Creation Issue accounts for 11.1% of a company’s score in our Rankings of America’s Most JUST Companies.

Compared to the Russell 1000, Jobs Leaders:

Outperforming Index Concept: Customers Leaders

Since Inception Alpha vs. Russell 1000 Benchmark: 3.6%

Customers are a key corporate stakeholder, and this index concept helps investors track the financial performance and social impact of companies that make customers a core priority. Overall, Customer Issues – including whether companies protect data privacy, make beneficial products, and more – account for 14% of a company’s score in our Rankings of America’s Most JUST Companies.

Compared to Russell the 1000, Customers Leaders:

Outperforming Index Concept: Sustainable Materials Leaders

Since Inception Alpha vs. Russell 1000 Benchmark: 8.3%

This index concept tracks companies that prioritize the environment through use of natural resources, renewable energy, and waste reduction practices. The IPCC’s August report found that unless there is an immediate, rapid, and large-scale reduction in greenhouse gas emissions, limiting warming to 1.5 degrees Celsius or even 2 degrees Celsius will be beyond reach. The “Uses sustainable materials” Issue accounts for 3.5% of a company’s score in our Rankings of America’s Most JUST Companies.

Compared to the Russell 1000, Sustainable Materials Leaders:

Outperforming Concept: JUST Midcap Growth Leaders

Since Inception Alpha vs Russell 1000: 17.8%

Within the benchmarks category, JUST MidCap Growth Leaders has been leading the performance since inception. The JUST MidCap Growth index concept takes the top quintile of companies in JUST Capital’s annual Rankings within the Russell 1000 MidCap Growth Index. This index concept exposes investors to a stylized benchmark portfolio concentrated around America’s Most JUST Companies.

Compared to Russell 100 companies, JUST Midcap Growth Leaders:

If you are interested in supporting our philanthropic mission by licensing our unique data, we are happy to discuss data needs, index licensing, and other ways we can partner. Please reach out to ESG Business Development Associate, Michael Wirtz, at mwirtz@justcapital.com.

Using data from JUST Capital’s Rankings of America’s Most JUST Companies, USA Financial has developed four account strategies that have seen phenomenal growth in assets under management (AUM). These strategies have delivered strong performance not only in 2022, but since inception.

The strategies rely on JUST Capital’s Overall Weighted Score, which takes into account the 20 core Issues determined through our survey research across key business stakeholders. Our 2023 Rankings continue to reflect the increased interest Americans show for workers’ issues, and these investment vehicles have quickly gained support from investors who care about good performance along with issues like workers’ pay and health and safety.

The funds have been popular with investors nationally, with a large concentration in the Midwest, and especially those in the 55+ age demographic. Because our Rankings reflect the issues that the majority of Americans are concerned about, these investment strategies appeal to investors across geography, generational divides, and political spectrums.

“The dynamic nature of the companies that rise to the top of JUST Capital Rankings are attractive investment options,” USA Financial CEO Mike Walters told us. “And knowing that these large companies are conscious of their place in the world and responsibility for the greater good makes the JUST Capital 100 a great starting point to apply our criteria.”

USA Financial offers four active strategies using JUST Capital’s Overall Weighted Score:

Depending on the selected strategy, USA Financial Formulas applies proprietary formulaic criteria or its Value Line Research (VLR) Ranking to the holdings obtained from our JUST 100 and JUST Industry Leaders when managing the account.

AUM has more than doubled in these strategies, with combined AUM growth of 252.6% from December 2021 to December 2022. The best performing of the four is the JUST Capital Industry Leaders Sustainable Equity Freedom strategy, delivering an alpha of 65.45% since inception and an alpha of 18.87% in 2022.

The companies comprising these USA Financial strategies have demonstrated their commitment to delivering value to all their stakeholders, not just their shareholders. They have shown that it is possible to achieve strong performance on issues that Americans prioritize without incurring additional costs. JUST Rankings serve as a scorecard for just business behavior and these strategies demonstrate that just business behavior pays off in the long run.

If you would like to learn more about JUST Capital’s Investor Strategies work, contact our team, and if you would like to license our data, fill out this form. You can also contact USA Financial to learn more about its strategies discussed above.