In the American economy’s golden era – spanning the 1950s and 1960s – real GDP growth averaged over 4%, while shareholders took home about 6.3% of annual GDP in corporate profits. After the heralded publication of Milton Friedman’s 1970 New York Times Magazine article “The Social Responsibility of a Corporation is to Raise its Profits,” shareholders have done relatively well: they have increased their take of output to over 8% of GDP in recent decades. Meanwhile, GDP growth has been on a steady downward trajectory, averaging only 2.5% over the same period. It seems clear that post-Friedman shareholder-centric capitalism has not been good for U.S. society at large. But has it even been good for shareholders?

There are points to argue in Friedman’s piece, but I whole-heartedly agree with him when he says “They [businesspeople] are capable of being extremely far-sighted and clear-headed in matters that are internal to their businesses. They are incredibly short-sighted and muddle-headed in matters that are outside their businesses but affect the possible survival of business in general.” With corporate profits as a percentage of GDP running at rates not seen in living memory, and owners of capital accreting enormous wealth, this question would seem to be a no-brainer “yes.” But what would shareholders’ experience have been under an alternative outcome?

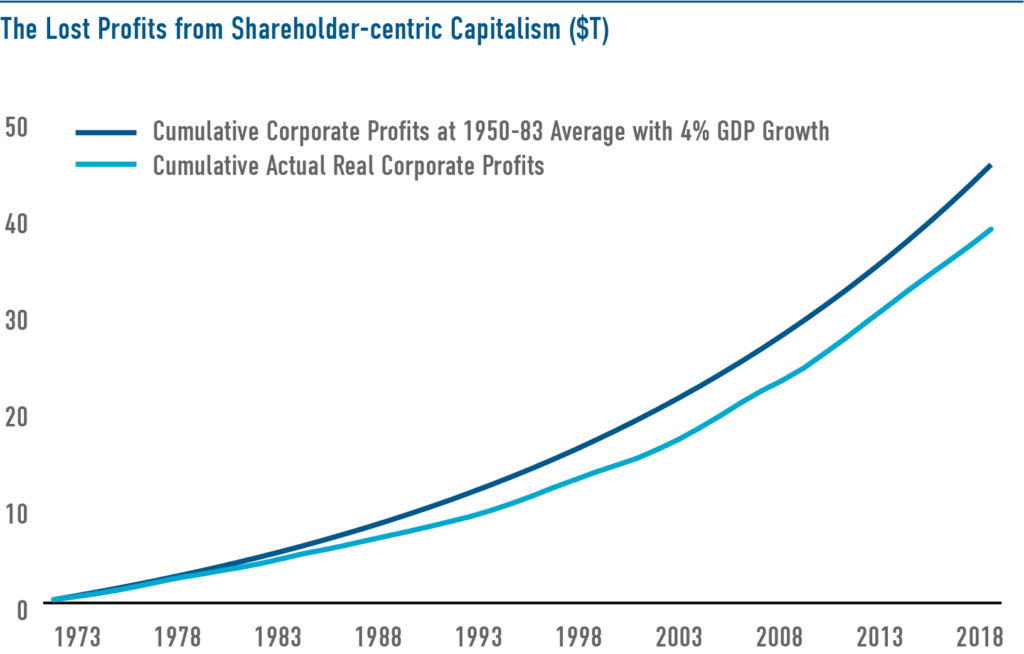

Consider this question: How much would shareholders have earned since 1973 if U.S. economic performance equaled that 4% growth and 6.3% Profit/GDP ratio? Is it greater or less than their actual total earnings?

In fact, total annual profits to corporations since 1973 (Real GDP * Annual Profit/GDP) are $6.7T less than they would have been in an alternative “higher growth, lower profitability” scenario. Not only has shareholder-centric capitalism been undermining the wider benefits to society that higher growth provides, but shareholders themselves have been worse off, too.

Even if we assume 3.5% GDP growth, shareholders would still be almost $1T better off. The power of compounding GDP growth dominates any benefit from taking a marginally bigger piece of that smaller economic pie.

Business leaders are starting to awaken to their responsibilities to the larger societies in which they operate. Their success in achieving higher returns for shareholders has not led to optimal distributive outcomes from capital reallocation (as Friedman might’ve hoped), but has instead suppressed potential GDP growth to shareholders’ own detriment. Investors and groups like the Business Roundtable are pushing back against the shareholder primacy model and recognizing that organizations must deliver value to all stakeholders – including workers, customers, communities, the environment, and shareholders.

We believe this return to “stakeholder capitalism” will enable business to play its necessary role in efficient allocation of resources, while maintaining its social license to operate by helping society grow output to serve broader social needs. We believe that effective measurement and management of value creation for workers, customers, communities, and the environment will lead to better outcomes overall. And maybe even more wealth in shareholders’ pockets, too.