In the third quarter of 2024, the S&P 500 posted a gain of 5.9%, reflecting the resilience of equity markets as they overcame initial volatility, including a sharp 12% correction in the technology sector. This recovery was driven by a significant shift in Federal Reserve policy, with the Fed implementing a 0.50% rate cut in September, the first such reduction since March 2020.

Sector performance underscored a rotation from growth-oriented areas of the market to more stable, income-generating value sectors. Value stocks out-performed growth stocks, with value sectors like utilities, financials, and consumer staples gaining traction amid market uncertainty. Value stocks returned a robust 9% for the quarter, significantly outperforming growth stocks, which posted a more modest 3.6% gain. Utilities led the way with an impressive 19.4% return, followed by real estate investment trusts (REITs), which gained 17.2%, and financials, which rose 10.7%. These sectors benefited from their defensive characteristics and income-generating potential, which became more attractive as interest rate expectations shifted. Energy, however, was the sole sector in negative territory due to weaker demand and lower oil prices, although it remains up 8.4% year-to-date.

The Federal Reserve’s rate cut also supported a notable rally in small-cap stocks, which outperformed their large-cap counterparts. The Russell 2000 small-cap index gained 9.3% during the quarter, benefitting from the Fed’s dovish stance, as lower rates tend to favor smaller companies that are more sensitive to borrowing costs. This marked a reversal from earlier in the year, when large-cap growth stocks dominated due to their perceived stability in a volatile economic environment.

As of September 30, 2024, our flagship index – the Just U.S. Large Cap Diversified Index (JULCD) has out-performed the Russell 1000 (Cap-Weighted) benchmark by 0.46% year-to-date and by 11.97% since its inception. Additionally, the Just 100 (equally weighted index) has outperformed the Russell 1000 (Equally-Weighted) index by 7.38% year-to-date and by 51.1% since its inception.

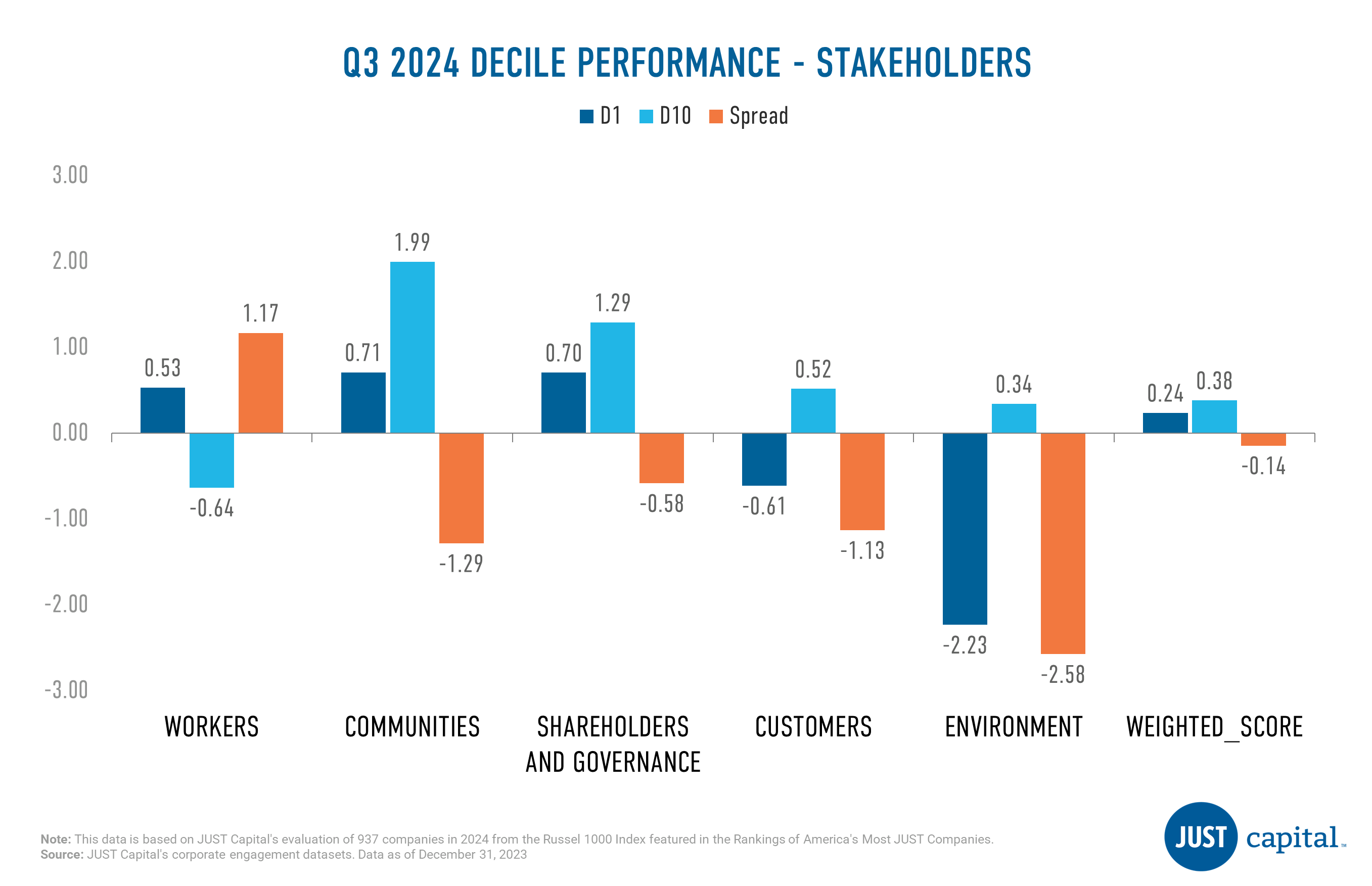

Just Capital found that four out of the five stakeholder categories it tracks delivered negative performance in Q3 2024, with the “Workers” stakeholder being the sole positive performer. The Workers stakeholder delivered the strongest performance over this period with a long-short spread of 1.17%. Notably, within the Workers stakeholder, outperformance was driven by both the top and bottom deciles.

Just Capital’s Overall Weighted Score takes into account the 20 core Issues determined through our annual survey research – including paying a living wage, creating a diverse, inclusive workplace, and helping combat climate change – across key business stakeholders: Workers, Communities, Shareholders & Governance, Customers, and Environment. The Overall Weighted Score delivered an almost neutral long-short spread of -0.14%, with the bottom decile serving as the primary negative contributor for the period ending September 30, 2024. Year-to-date the performance spread between top and bottom decile for Overall Score is at 9.11%

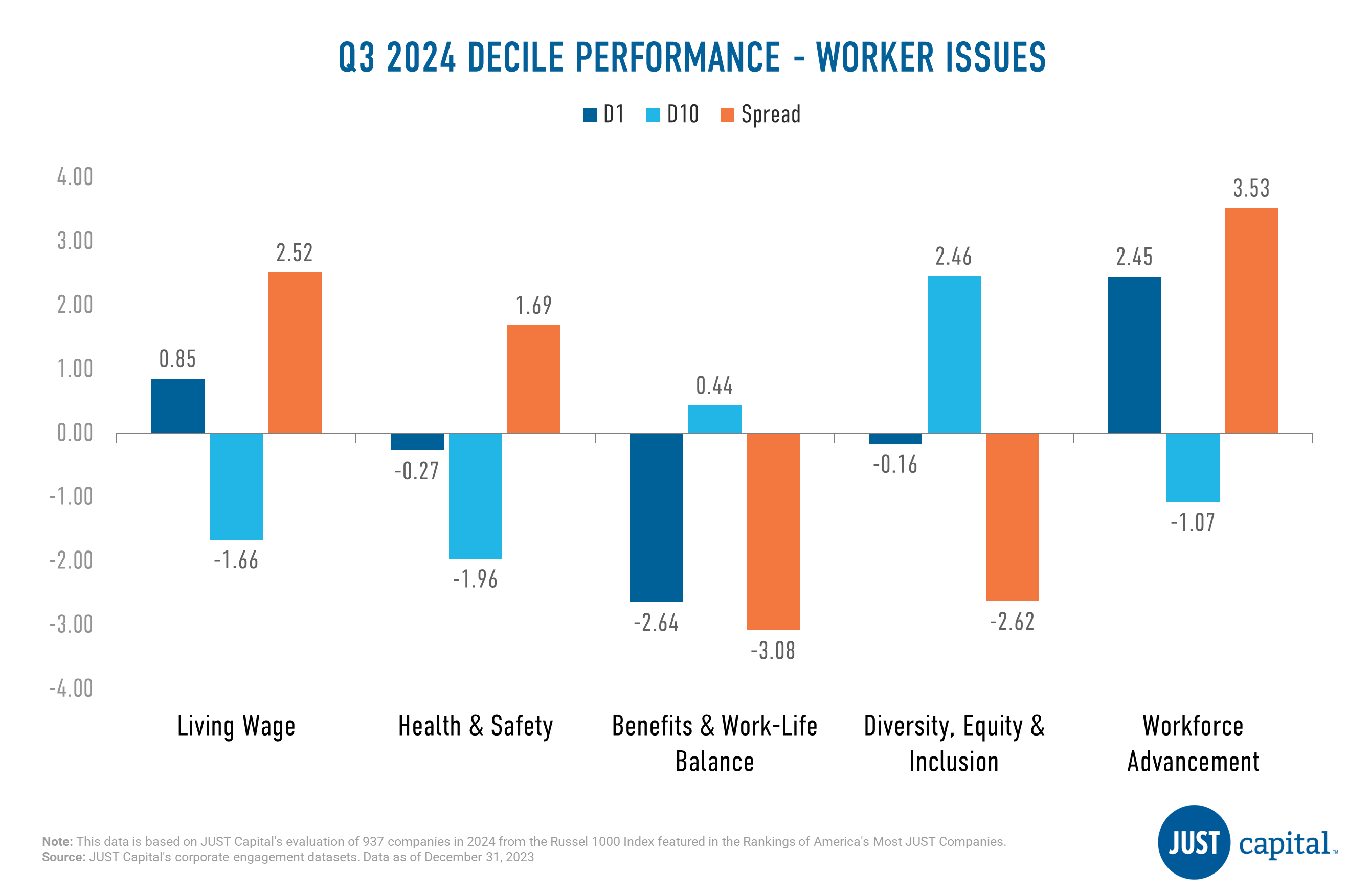

Workers

The Workers stakeholder measures a company across five Issues:

In Q3 2024, we saw three out of five issues deliver positive performance, with the Workforce Advancement Issue faring the best. Benefits & Work-Life Balance was the weakest performer amongst the Worker issues.

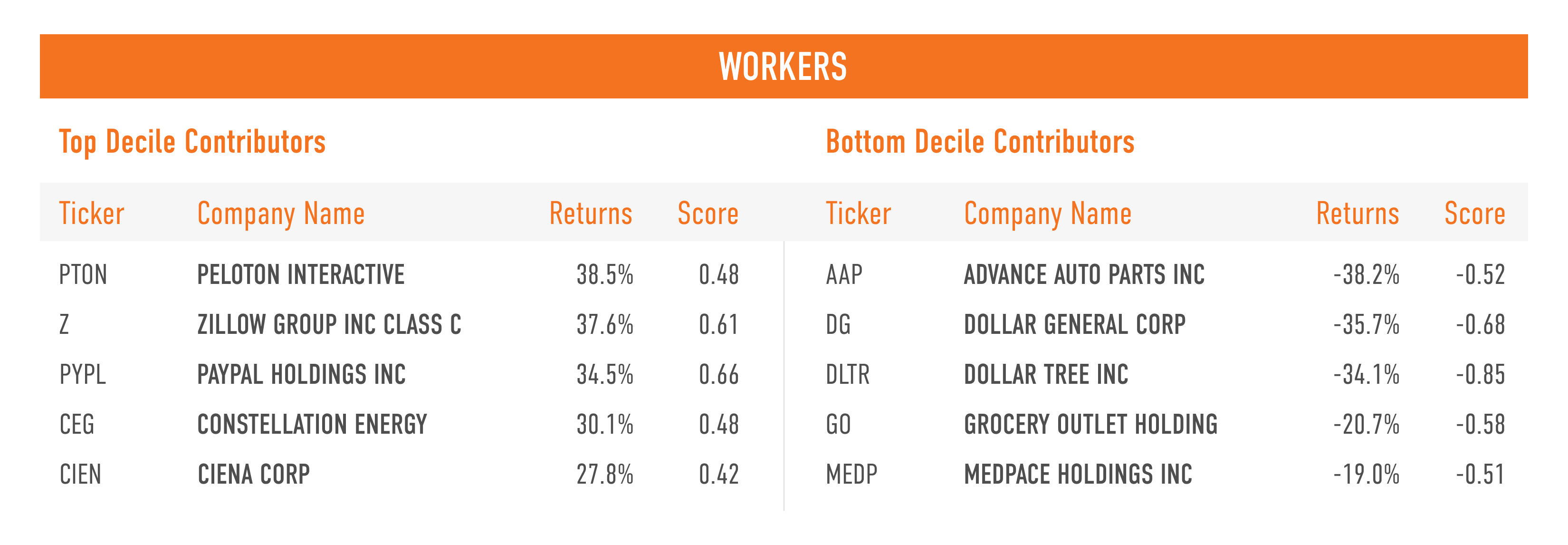

Shown below are the top and bottom five contributors to the top decile (D1), the top-ranked companies as measured by their Workers score, and the bottom decile (D10), the lowest-ranked companies as measured by their Workers score.

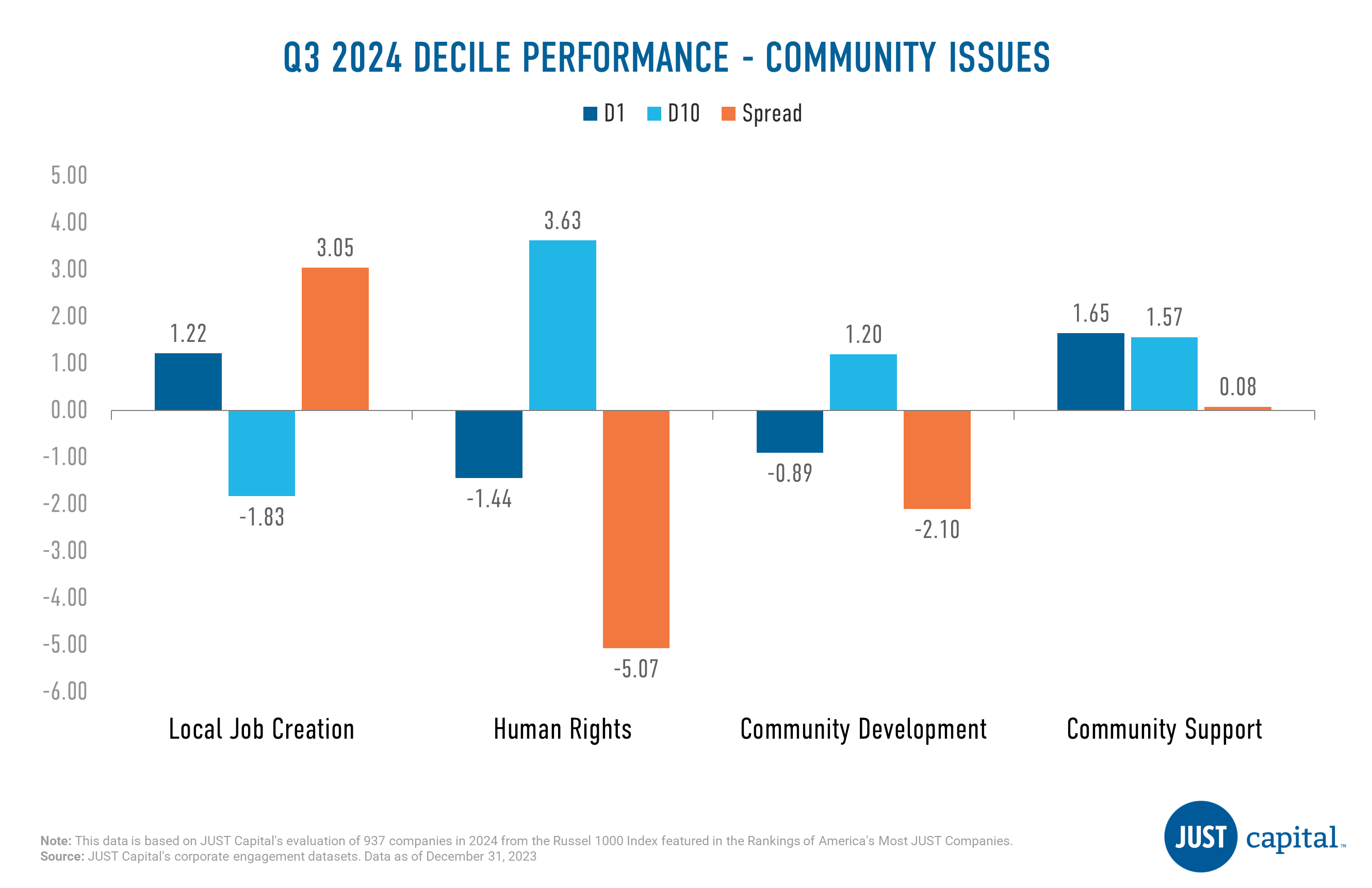

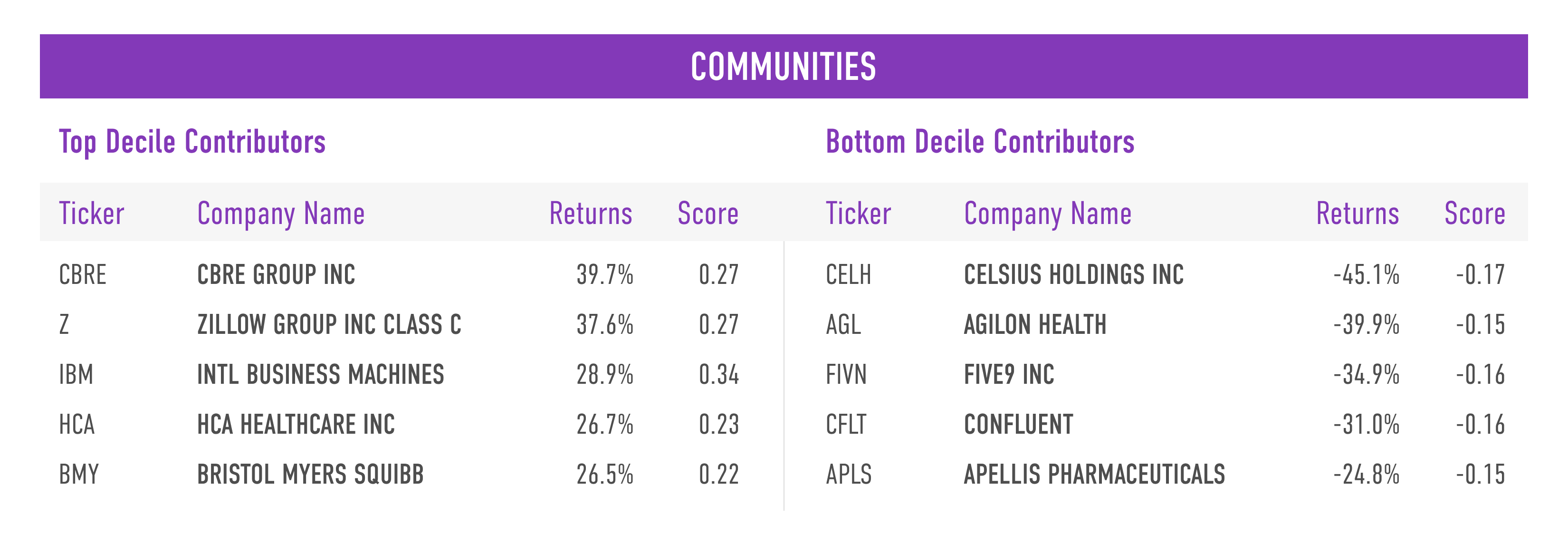

The Communities stakeholder measures a company across four Issues:

Local Job Creation was the strongest performer followed by Community Support. Human Rights and Community Development were negative contributors this quarter.

Shown below are the top and bottom five contributors to the top decile (D1), the best-ranked companies as measured by their Communities score, and the bottom decile (D10), the lowest-ranked companies as measured by their Communities score.

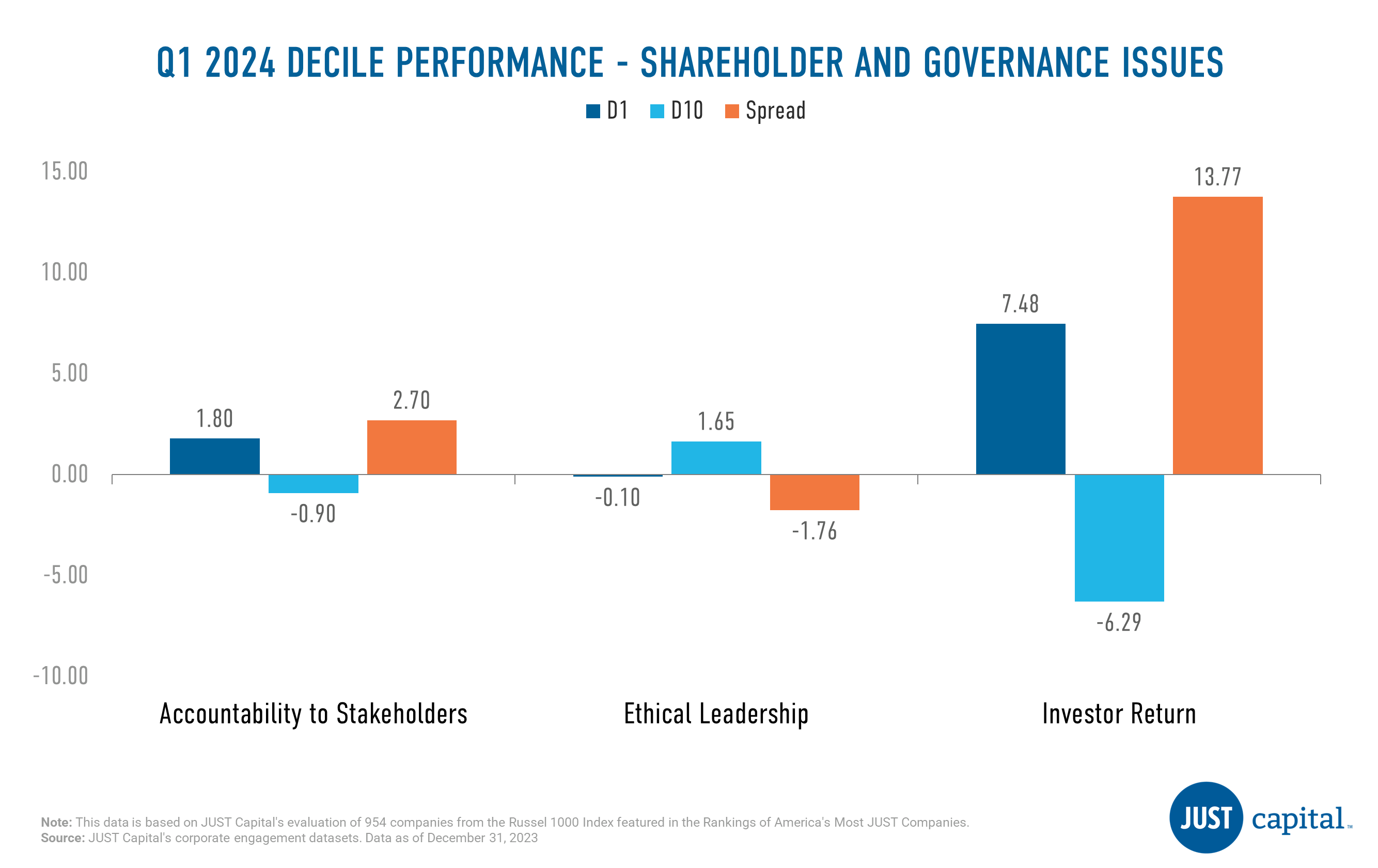

Shareholders and Governance

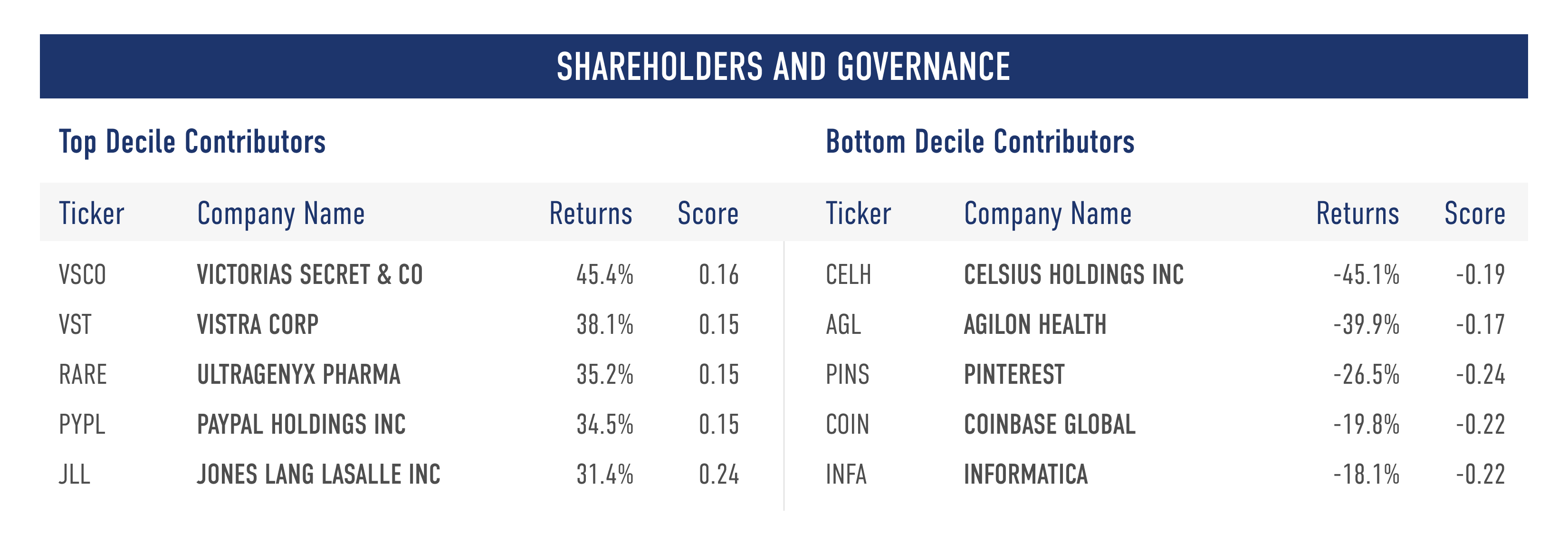

The Shareholders and Governance stakeholder measures a company across three Issues:

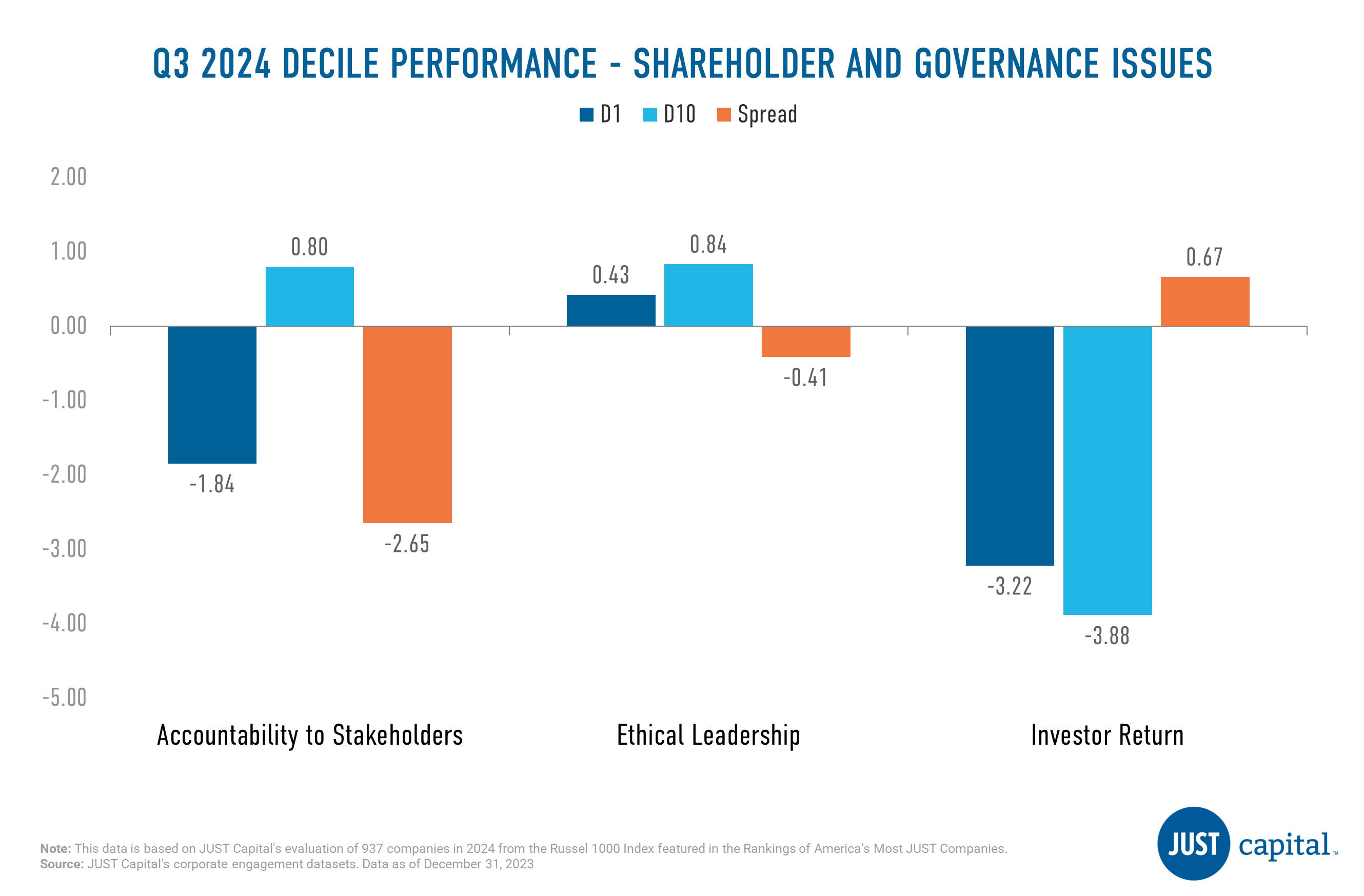

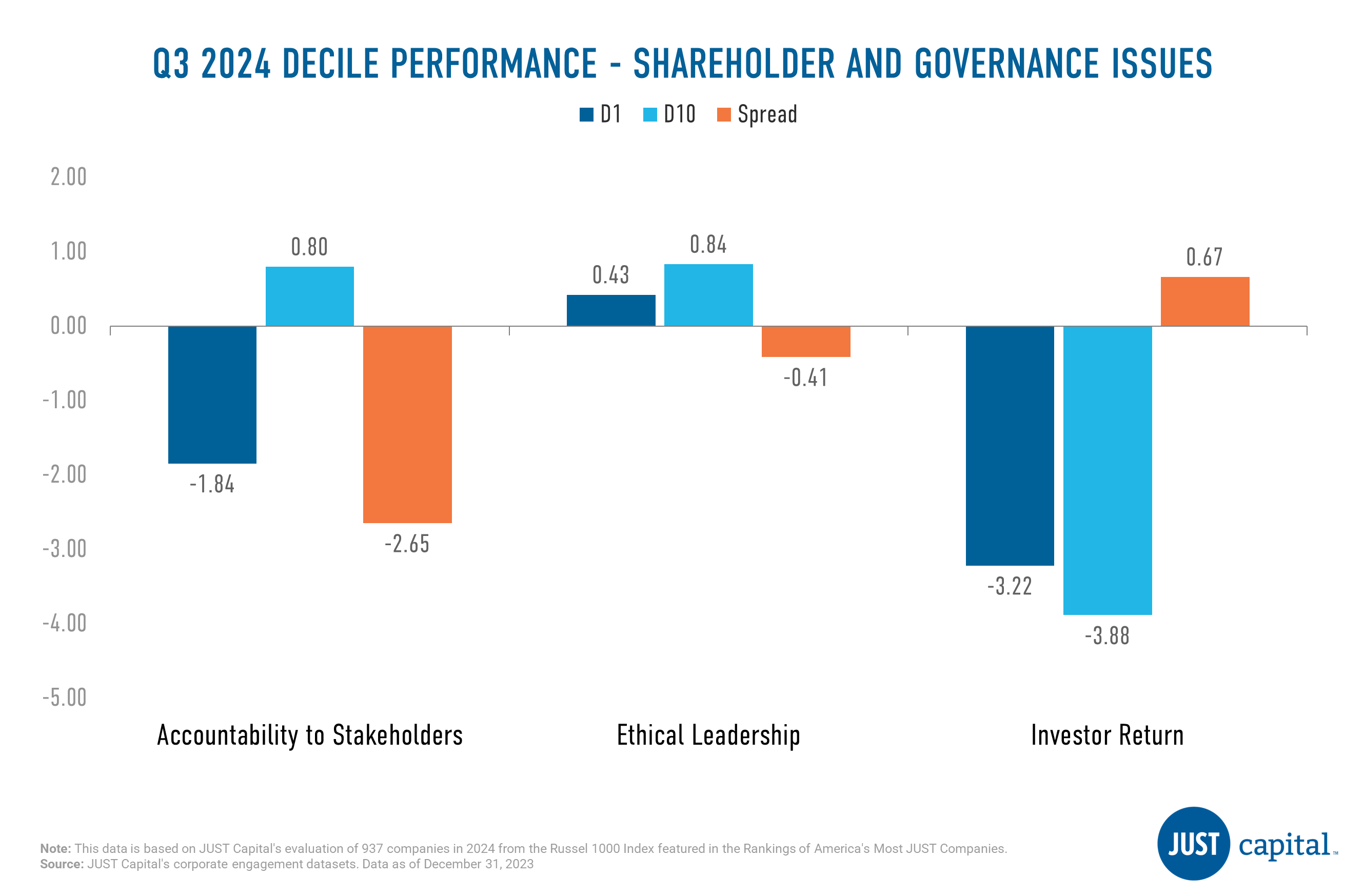

Investor Return Issue was the only positive performer in Q3 with a long-short spread of 0.67%. Remaining issues within the Shareholder stakeholder were negative this quarter.

Shown below are the top and bottom five contributors to the top decile (D1), the best-ranked companies as measured by their Shareholders and Governance score, and the bottom decile (D10), the lowest-ranked companies as measured by their Shareholders and Governance score.

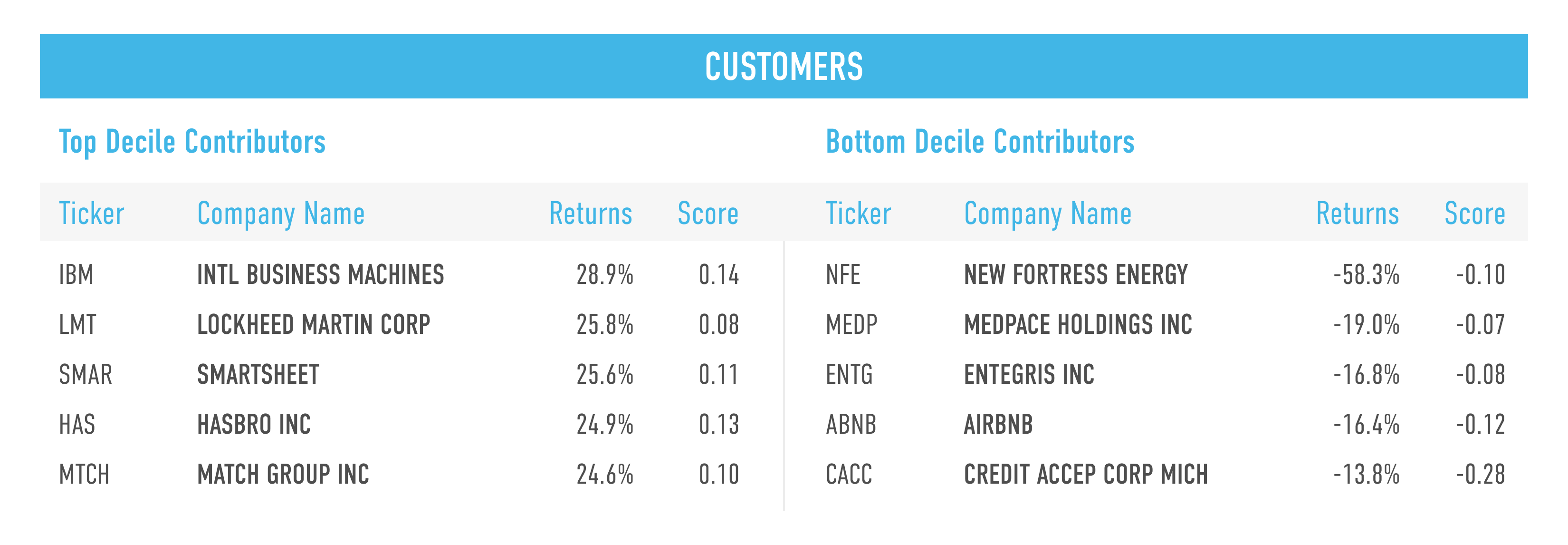

Customers

The Customers stakeholder measures a company across four Issues:

In Q3 2024, all four Customer Issues delivered negative performance. Customer Treatment was the weakest performer followed by Beneficial Products.

Shown below are the top and bottom five contributors to the top decile (D1), the best-ranked companies as measured by their Customers score, and the bottom decile (D10), the lowest-ranked names as measured by their Customers score.

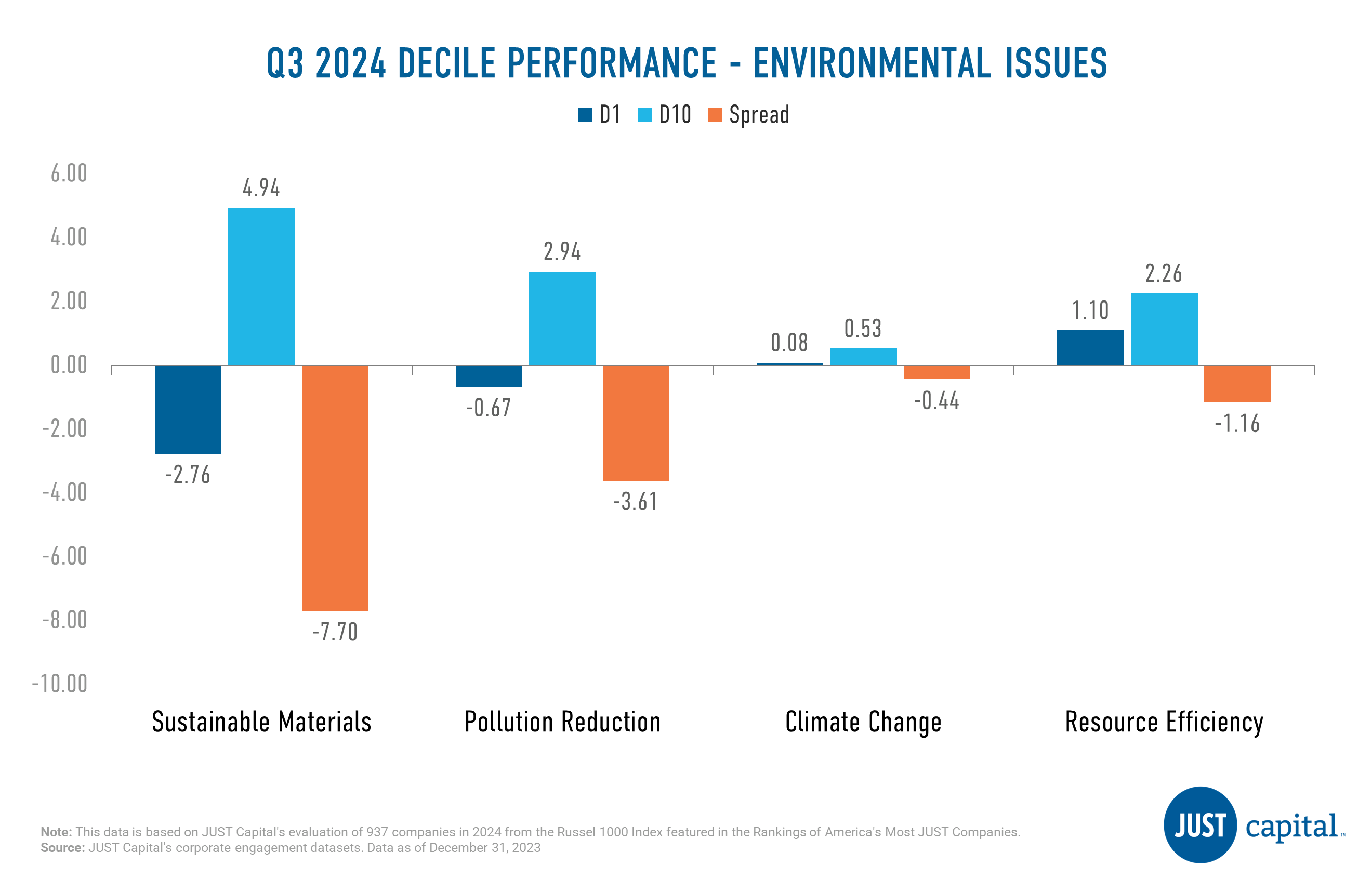

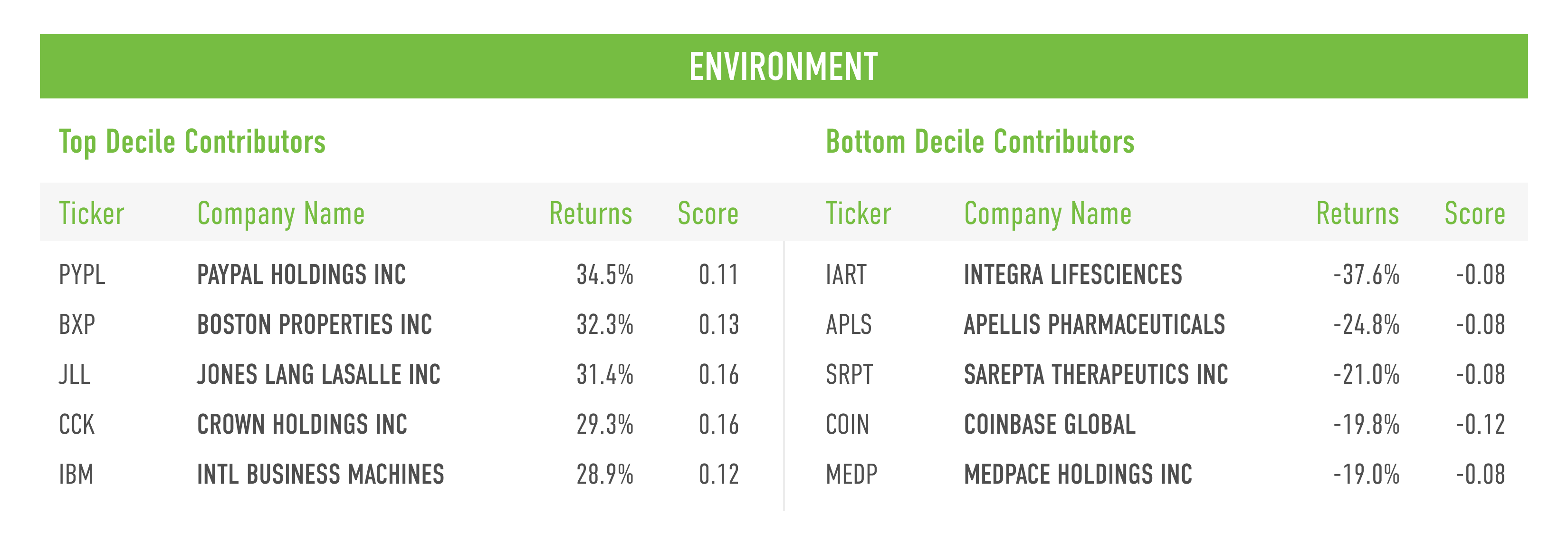

Environment

The Environment stakeholder measures a company across four Issues:

In Q3 2024, we saw all four Environmental issues deliver negative performance. Sustainable Materials was the worst performing issue within Environment stakeholder this quarter.

Shown below are the top and bottom five contributors to the top decile (D1), the best-ranked companies as measured by their Environment score, and the bottom decile (D10), the lowest-ranked companies as measured by their Environment score.

Computation Methodology

We monitor the performance of these stakeholders and Issues on a long-short basis. The long and short portfolios are selected based on the factor scores as the top and bottom deciles within the universe of companies we track in the Russell 1000. Top decile (D1) companies are those that rank highest based on the factor score, and bottom decile (D10) companies are those that rank lowest based on the factor score.

D1 Performance is computed as

(Equally weighted average of returns of stocks in D1 bucket) – (Equally weighted average of returns of all stocks within the Universe)

D10 Performance is computed as

(Equally weighted average of returns of stocks in D10 bucket) – (Equally weighted average of returns of all stocks within the Universe)

Spread is computed as

D1 Performance – D10 Performance

In the second quarter of 2024, global equity prices continued their robust performance, contributing to an impressive one-year rebound. The S&P 500 Index rose by 4.3% during this period, though many segments of the domestic stock market, including mid and small-cap indices, lagged behind and declined. Among large-cap stocks, the average stock fell by 2.6%, as indicated by the equal-weighted version of the S&P 500. The quarter experienced fluctuations, with April seeing a downturn that reversed some Q1 gains, but a rebound in May led the S&P 500 to set multiple new all-time highs. The quarter concluded with strong stock market gains, fueled by robust company earnings and easing inflation, elevating the S&P 500’s year-to-date performance to 15.3%.

The strong performance of the S&P 500 was primarily driven by the Information Technology and Communication Services sectors, with ongoing enthusiasm around AI boosting related companies amid strong earnings and optimistic outlook statements. The Information Technology sector alone accounted for 95% of the Index’s gain, with NVIDIA leading the charge and contributing nearly half of the S&P 500’s return. Conversely, cyclical sectors such as Financials, Industrials, Health Care, and Materials were the biggest underperformers.

As of June 30, 2024, our flagship index – the JUST U.S. Large Cap Diversified Index (JULCD) has out-performed the Russell 1000 (Cap-Weighted) benchmark by 1.51% year-to-date and by 13.78% since its inception. Additionally, the JUST 100 (equally weighted index) has outperformed the Russell 1000 (Equally-Weighted) index by 6.65% year-to-date and by 44.77% since its inception.

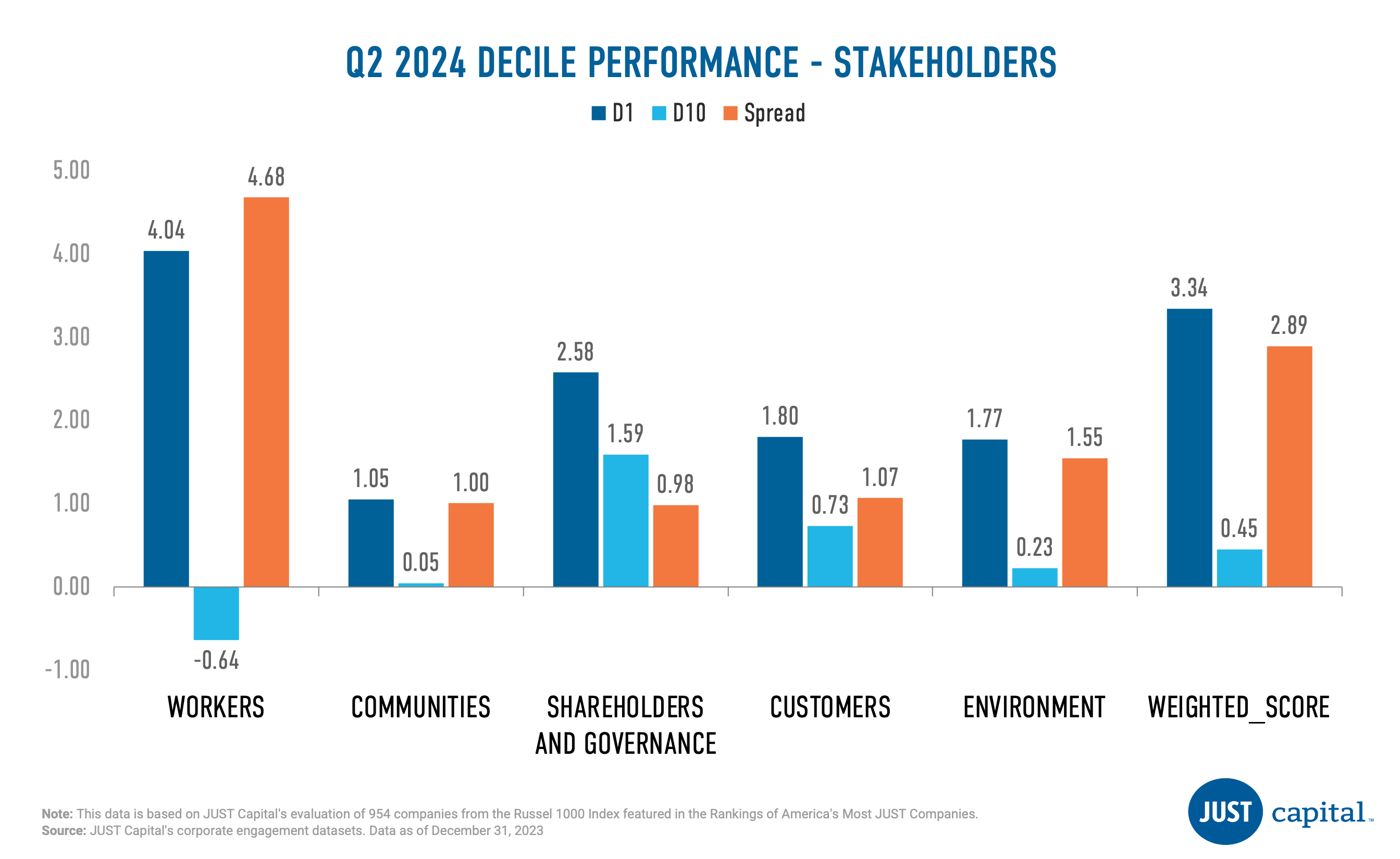

JUST Capital found that all of the five stakeholders we track delivered positive performance in Q2 2024. The Workers stakeholder delivered the strongest performance over this period with a long-short spread of 4.68%. Within the Workers stakeholder, outperformance was driven by both the top and bottom deciles whereas for remaining stakeholders outperformance was driven by top decile.

JUST Capital’s Overall Weighted Score takes into account the 20 core Issues determined through our annual survey research – including paying a living wage, creating a diverse, inclusive workplace, and helping combat climate change – across key business stakeholders: Workers, Communities, Shareholders & Governance, Customers, and Environment. This Overall Weighted Score had a positive long-short spread of 2.89% over the period ending June 28,2024.

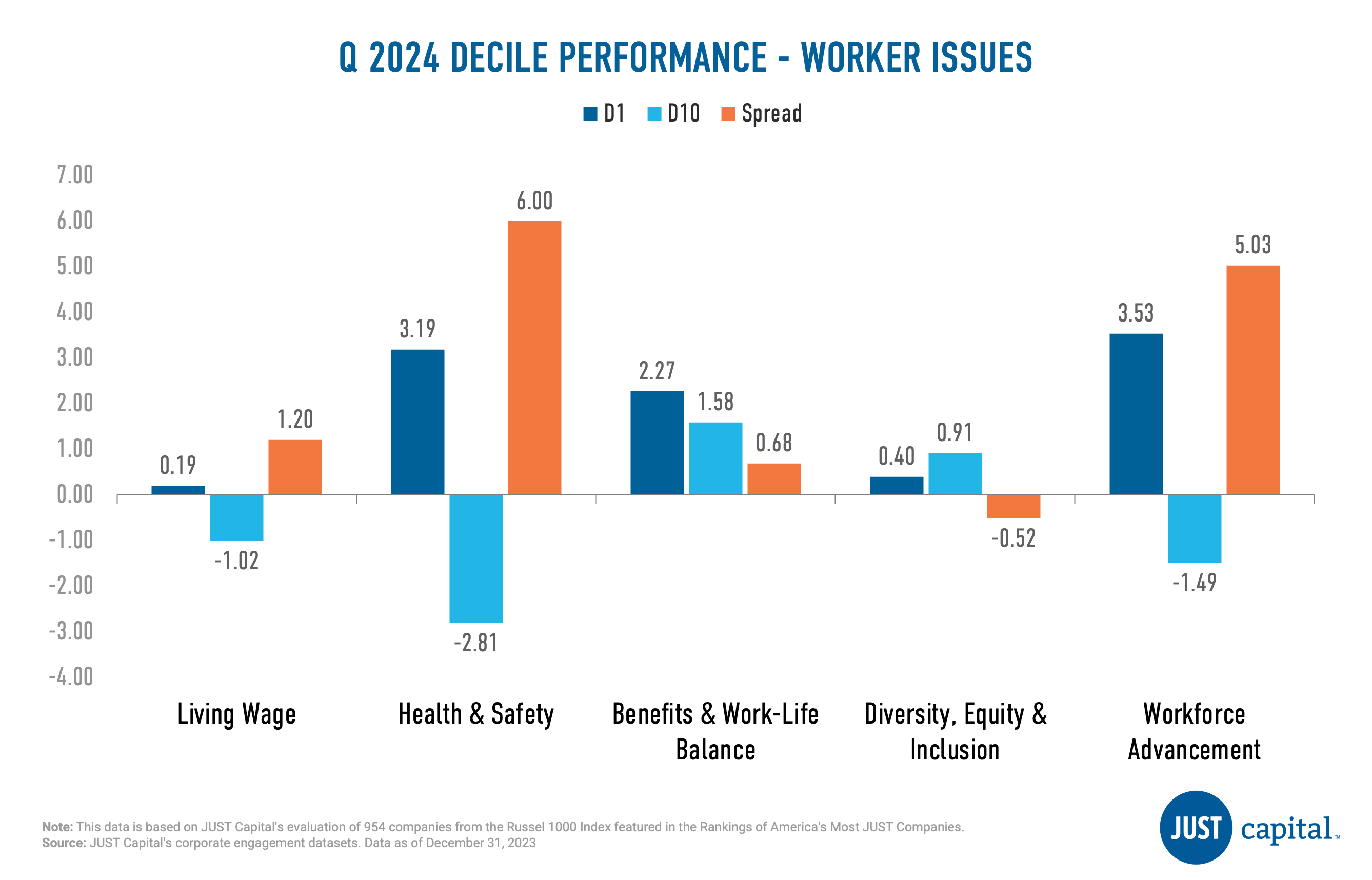

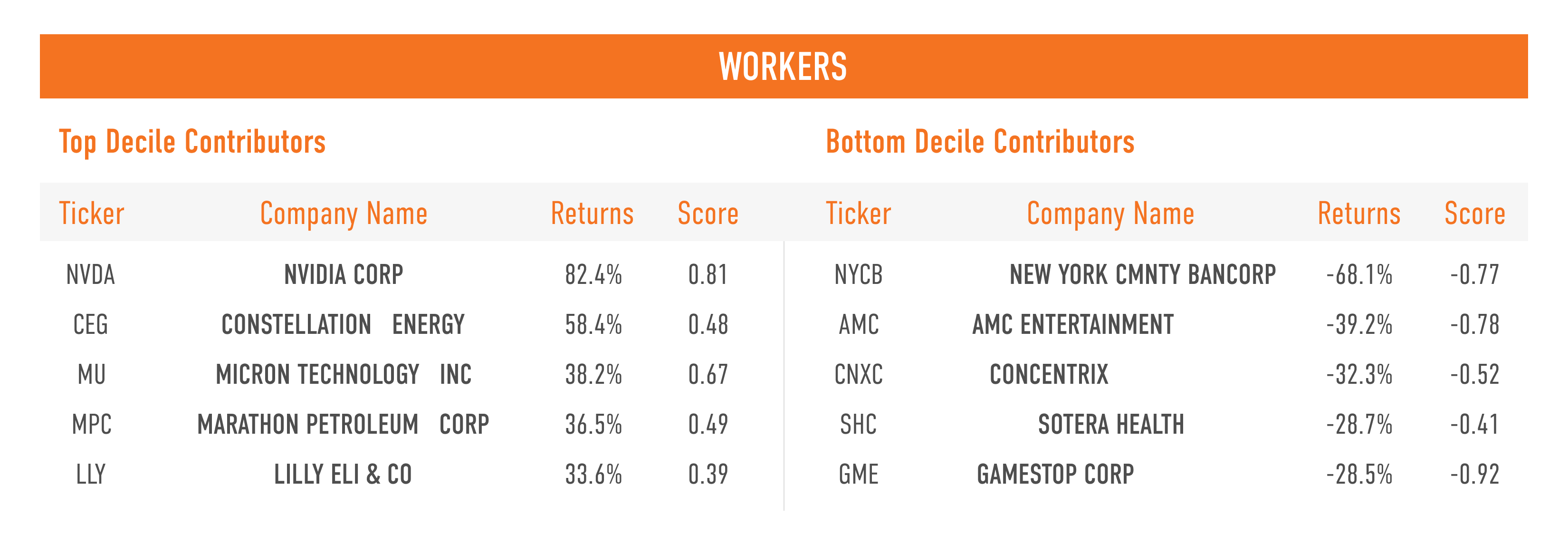

The Workers stakeholder measures a company across five Issues:

In Q2 2024, we saw four out of five issues deliver positive performance, with the Health & Safety Issue faring the best. Diversity Equity & Inclusion was the weakest performer amongst the Worker issues.

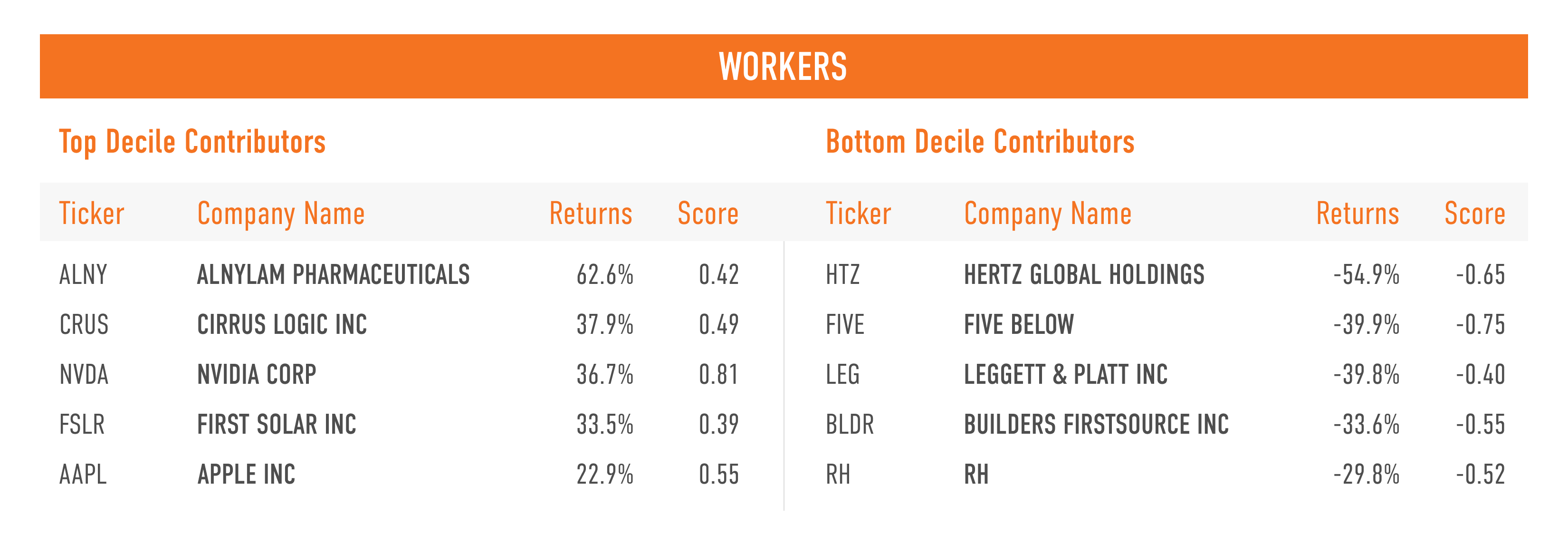

Shown below are the top and bottom five contributors to the top decile (D1), the top-ranked companies as measured by their Workers score, and the bottom decile (D10), the lowest-ranked companies as measured by their Workers score.

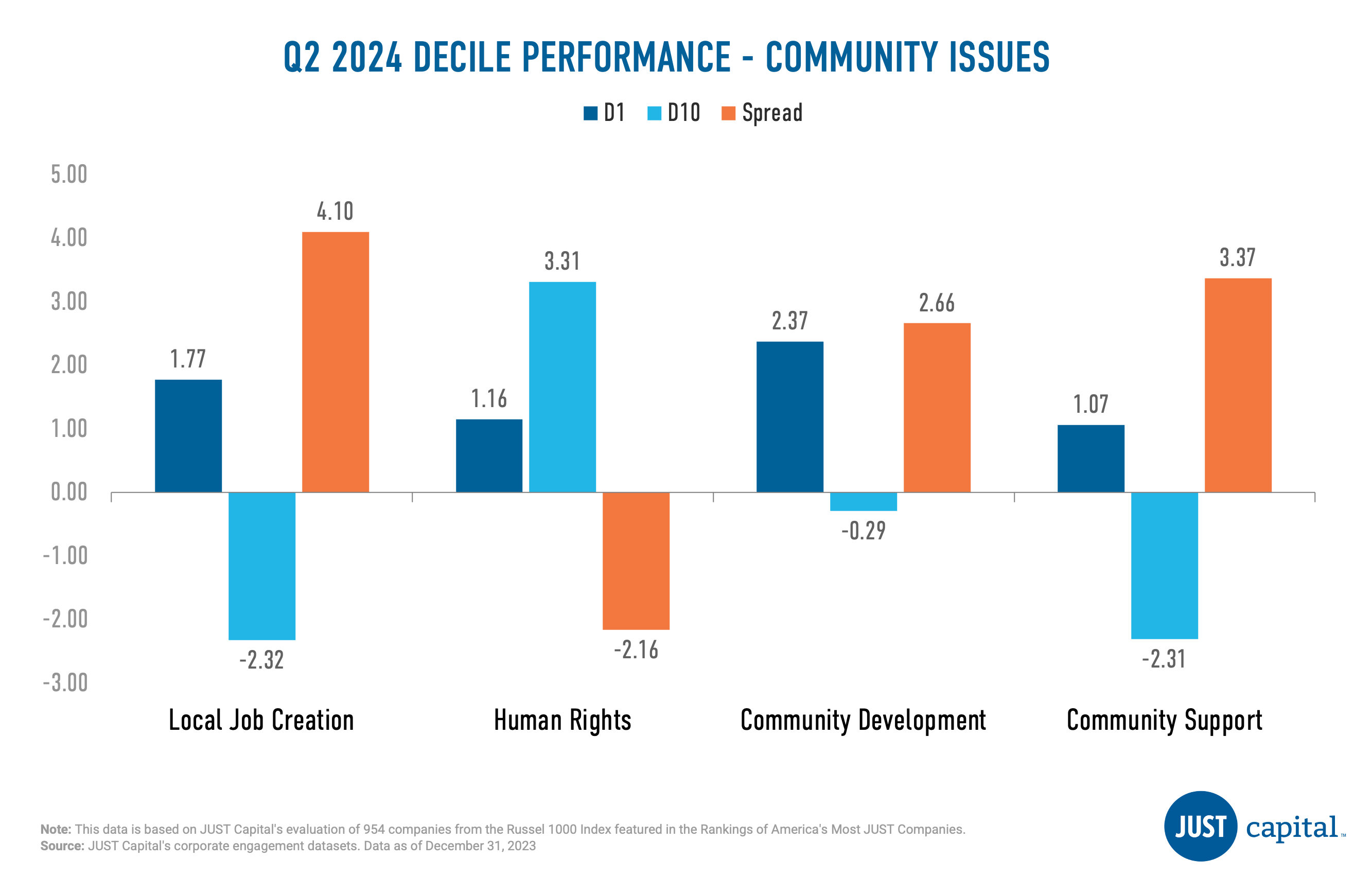

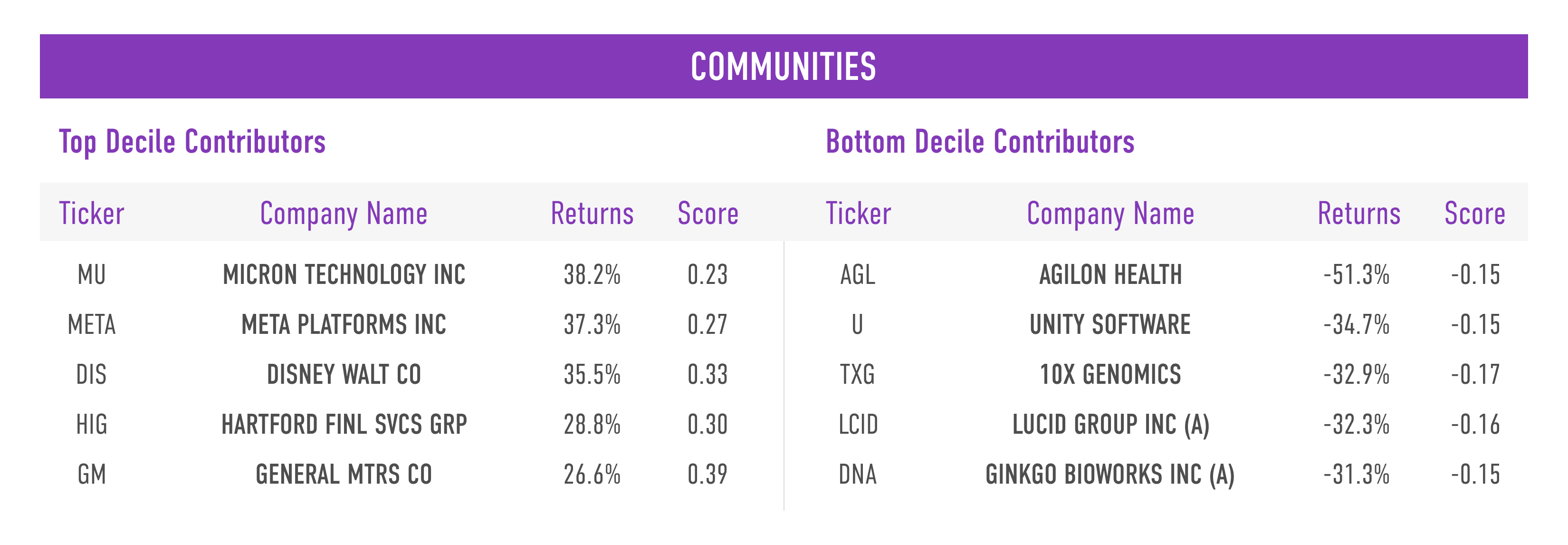

The Communities stakeholder measures a company across four Issues:

Local Job Creation was the strongest performer followed by Community Support. Human Rights was a negative contributor this quarter.

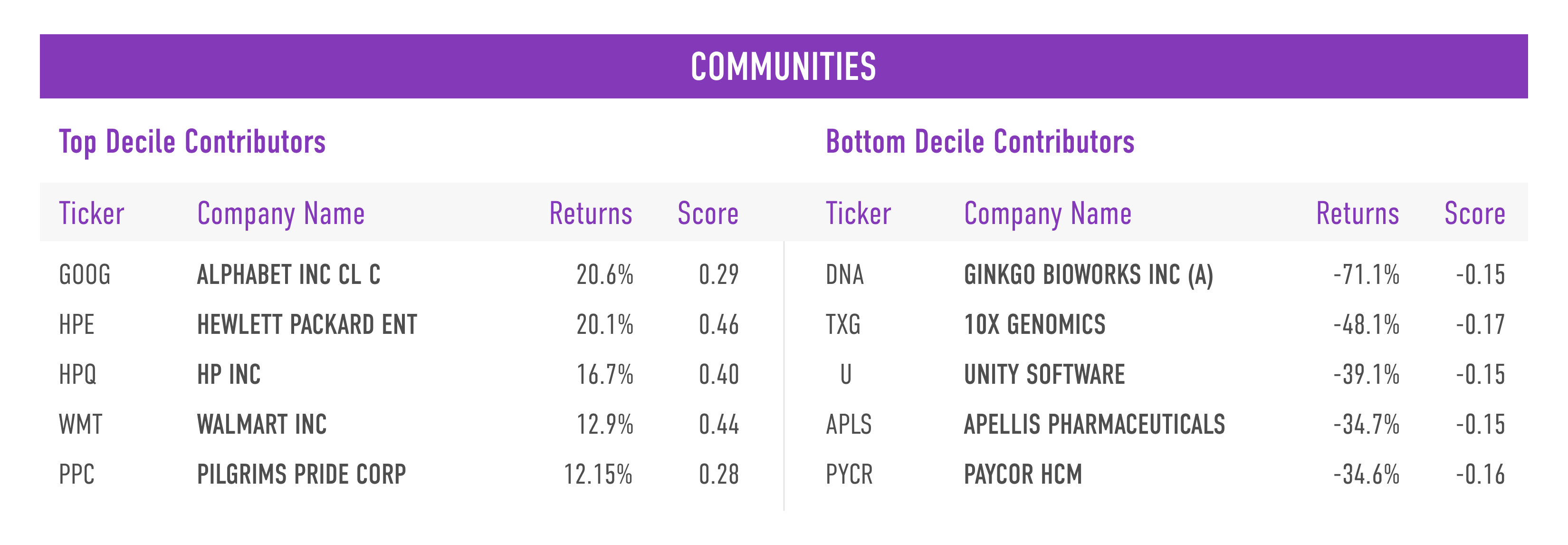

Shown below are the top and bottom five contributors to the top decile (D1), the best-ranked companies as measured by their Communities score, and the bottom decile (D10), the lowest-ranked companies as measured by their Communities score.

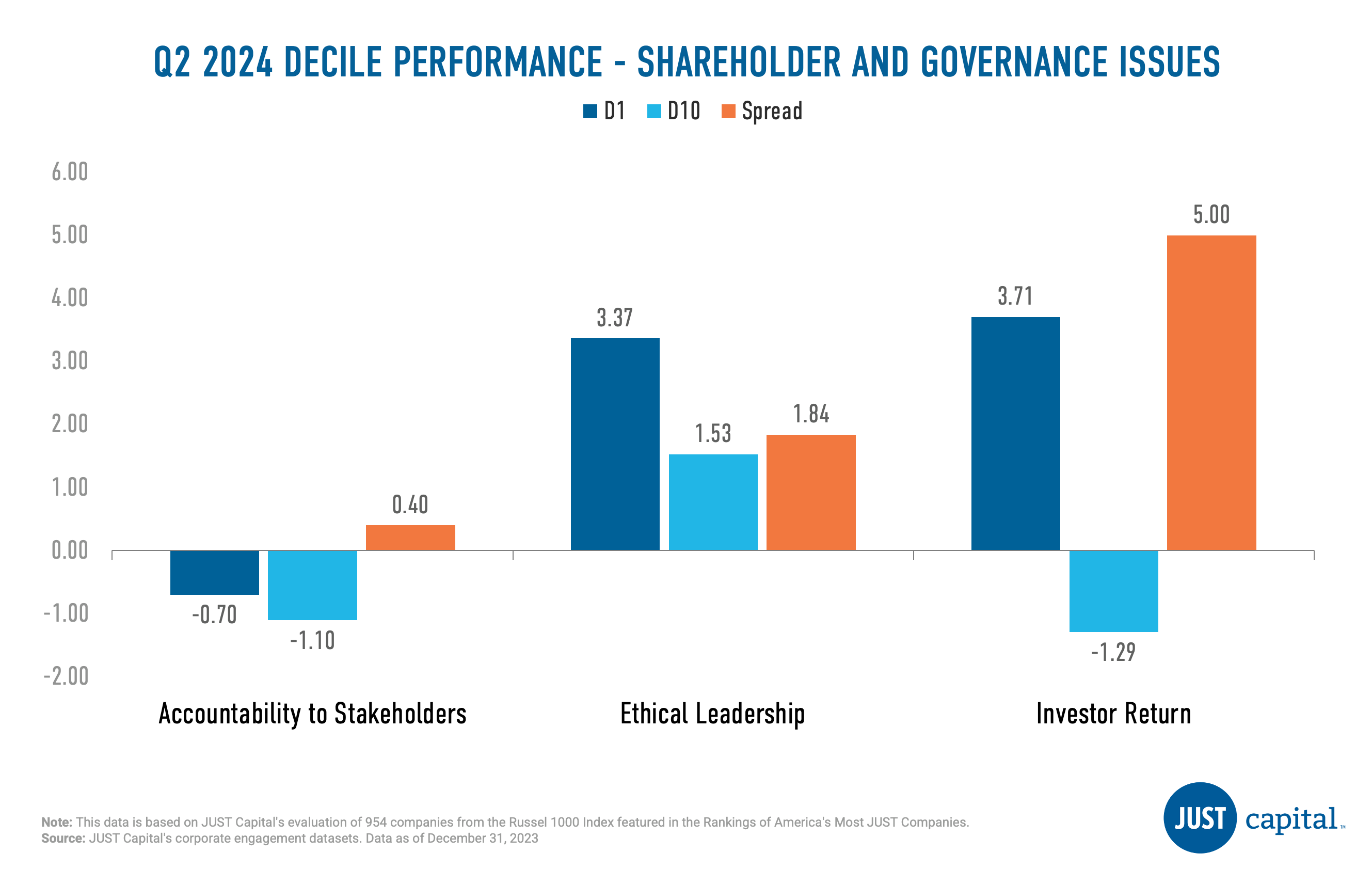

The Shareholders and Governance stakeholder measures a company across three Issues:

Investor Return Issue was the strongest performer in Q2 with a long-short spread of 5% followed by Ethical Leadership. All issues delivered positive performance in Q2 2024.

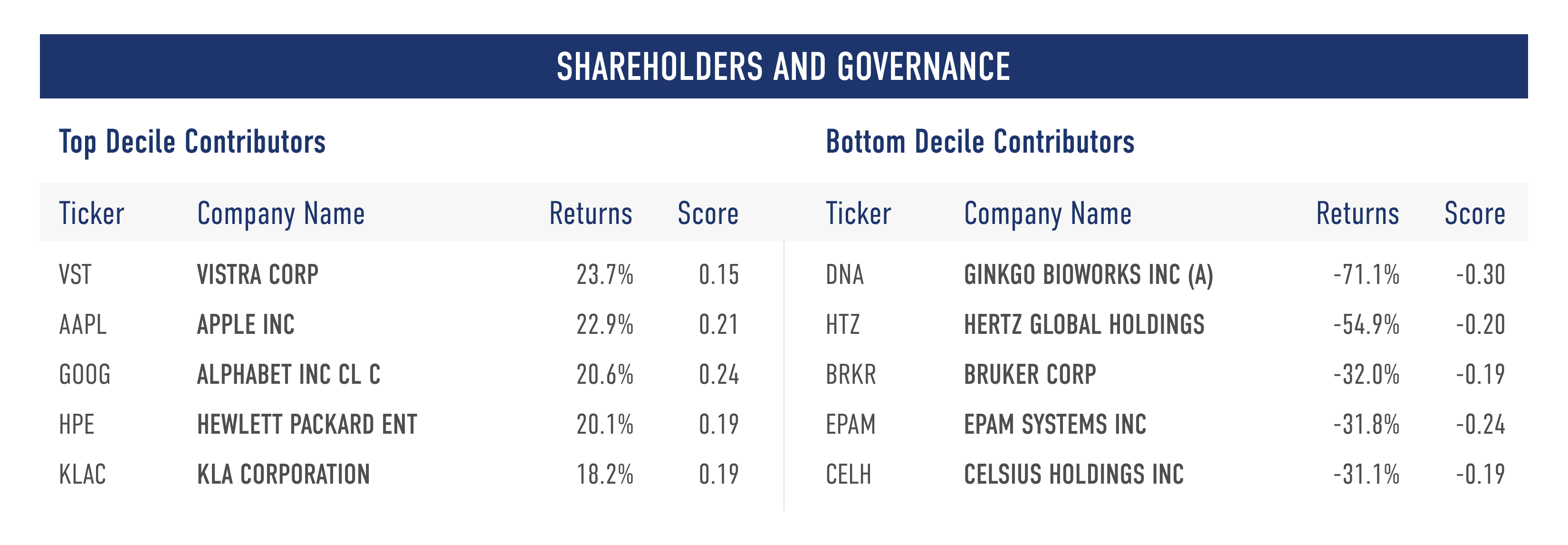

Shown below are the top and bottom five contributors to the top decile (D1), the best-ranked companies as measured by their Shareholders and Governance score, and the bottom decile (D10), the lowest-ranked companies as measured by their Shareholders and Governance score.

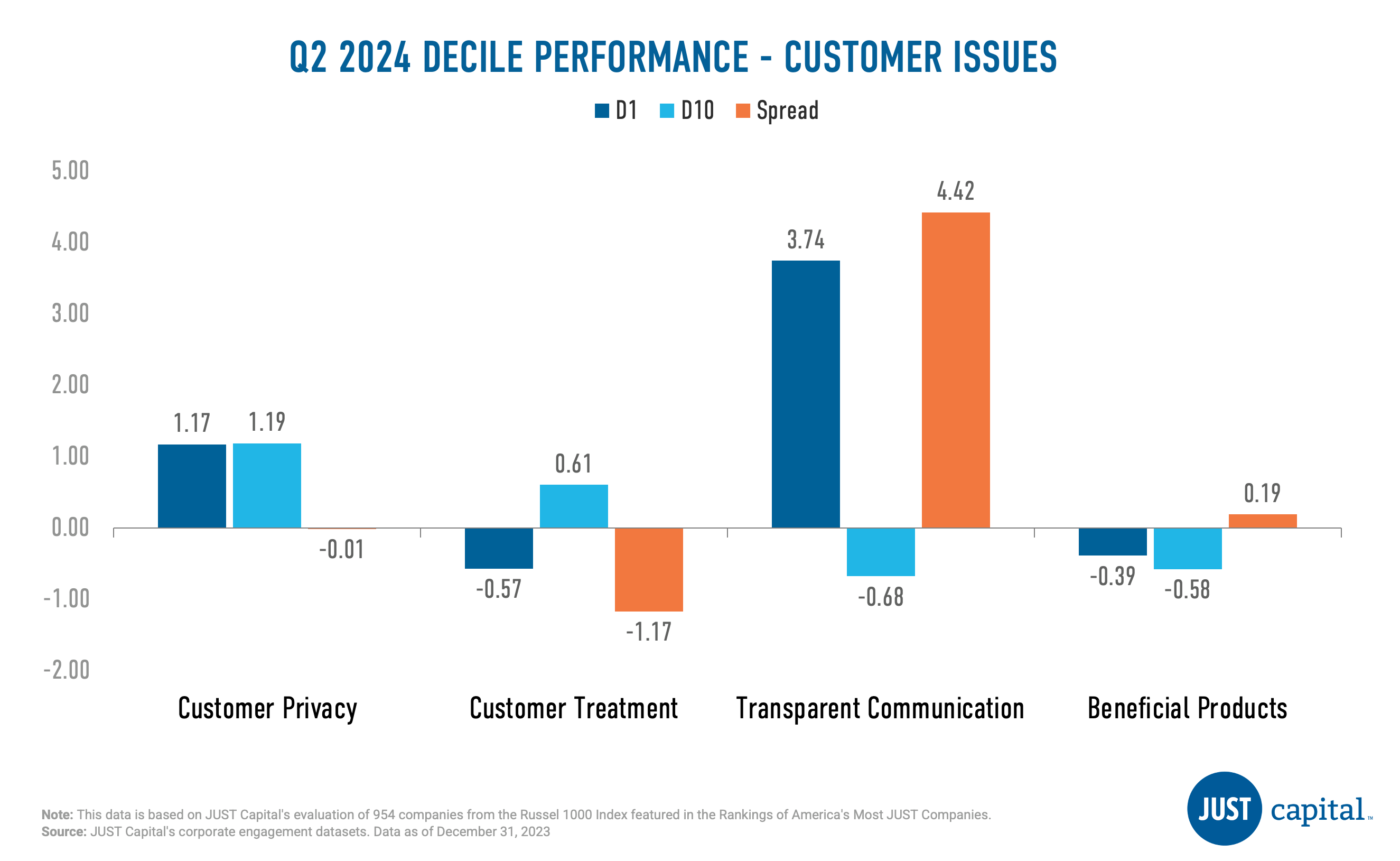

The Customers stakeholder measures a company across four Issues:

In Q2 2024, two out of 4 Customer Issues delivered negative performance. Transparent Communication was the best performer followed by Beneficial Products.

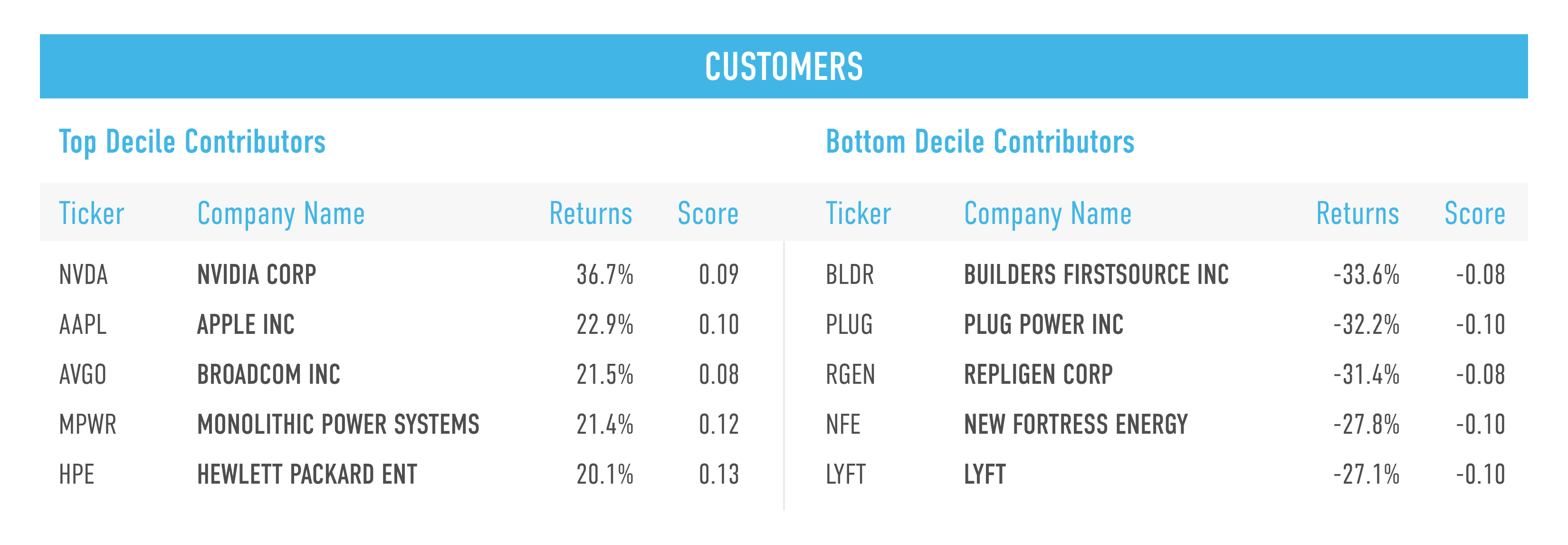

Shown below are the top and bottom five contributors to the top decile (D1), the best-ranked companies as measured by their Customers score, and the bottom decile (D10), the lowest-ranked names as measured by their Customers score.

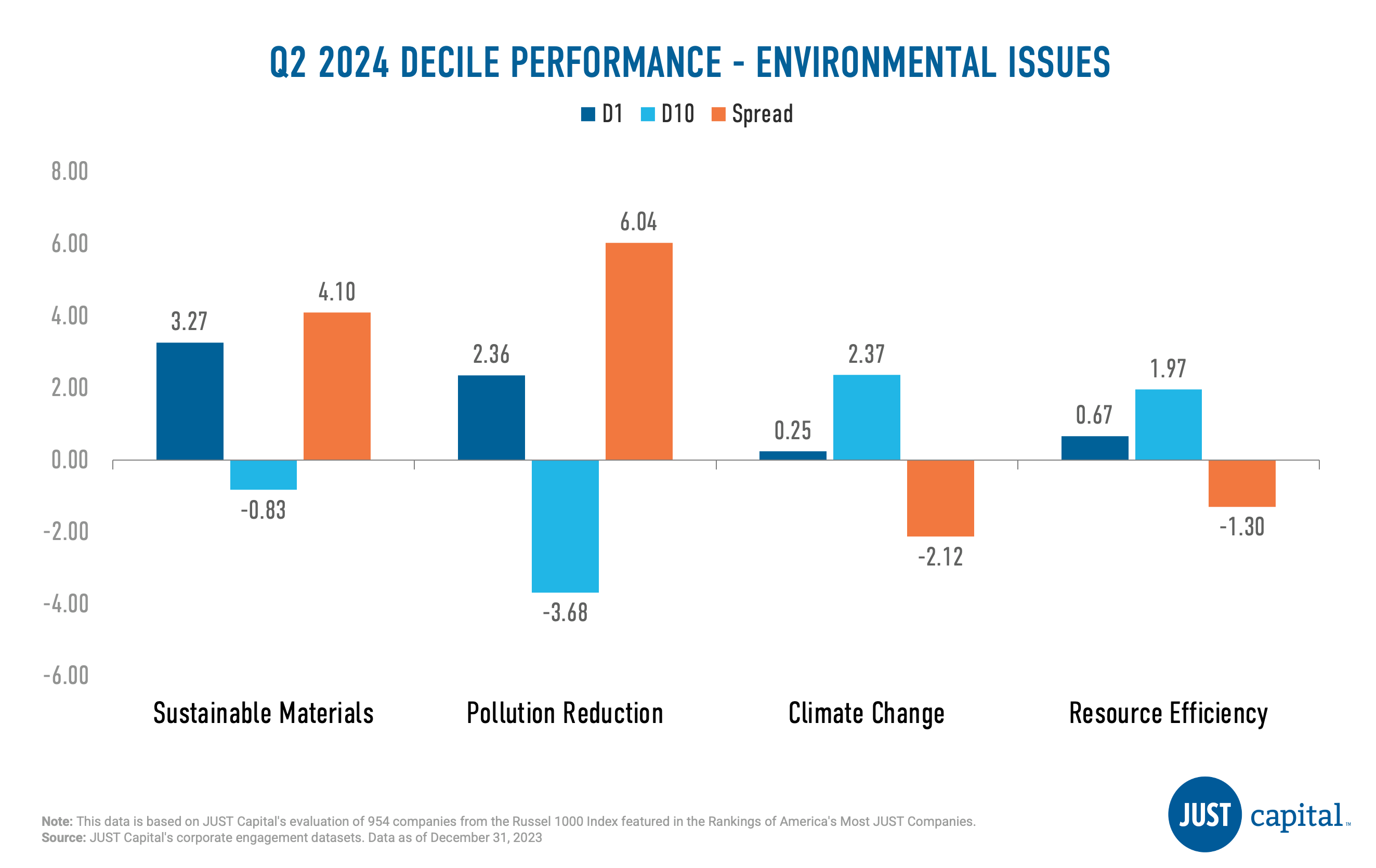

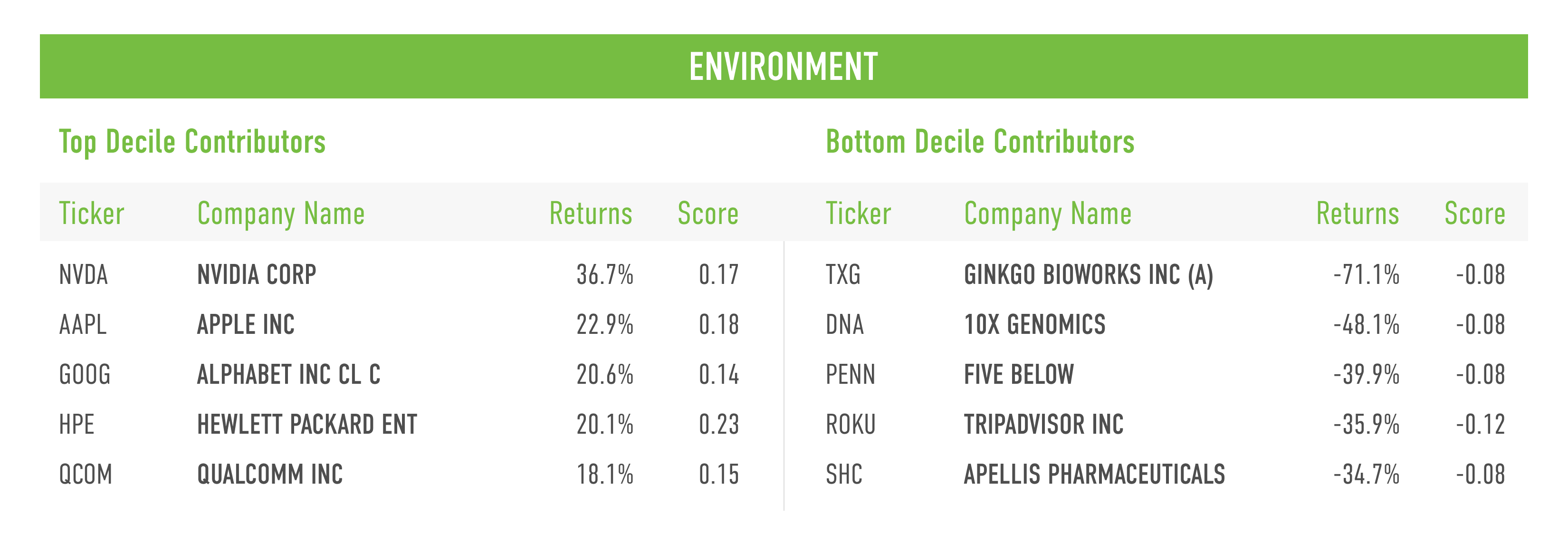

The Environment stakeholder measures a company across four Issues:

In Q2 2024, we saw two of four Environment Issues deliver positive performance. Pollution Reduction was the top contributor followed by Sustainable Materials in Q2. Climate Change and Resource Efficiency delivered negative performance this quarter.

Shown below are the top and bottom five contributors to the top decile (D1), the best-ranked companies as measured by their Environment score, and the bottom decile (D10), the lowest-ranked companies as measured by their Environment score.

Computation Methodology

We monitor the performance of these stakeholders and Issues on a long-short basis. The long and short portfolios are selected based on the factor scores as the top and bottom deciles within the universe of companies we track in the Russell 1000. Top decile (D1) companies are those that rank highest based on the factor score, and bottom decile (D10) companies are those that rank lowest based on the factor score.

D1 Performance is computed as

(Equally weighted average of returns of stocks in D1 bucket) – (Equally weighted average of returns of all stocks within the Universe)

D10 Performance is computed as

(Equally weighted average of returns of stocks in D10 bucket) – (Equally weighted average of returns of all stocks within the Universe)

Spread is computed as

D1 Performance – D10 Performance

Following a remarkable 2023, stocks have once again surged in 2024, with the S&P 500 achieving its most impressive first-quarter performance since 2019, boasting a year-to-date return of 10.55%. This notable upswing can be attributed to encouraging economic indicators, alleviating concerns regarding a potential U.S. economic downturn. Investors have shifted their focus towards the Federal Reserve’s anticipated transition from monetary policy tightening to easing.

The Nasdaq experienced a significant uptick of 9.3% in the first quarter, propelled by a sustained rally in artificial intelligence-related stocks and optimistic remarks from Federal Reserve officials. Notably, the Magnificent Seven, comprising 29% of the S&P 500’s market value, contributed 37% to the year-to-date return. However, a new group, dubbed the Gang of Four, including Nvidia, Microsoft, Meta Platforms (formerly known as Meta), and Amazon.com, emerged, accounting for 18% of the S&P 500 and 47% of the year-to-date return.

Market breadth remained robust with 369 stocks advancing and 134 declining, showcasing a broad-based rally across sectors. Of the 11 sectors, 10 experienced gains, underscoring the market’s overall strength.

In terms of sectors, technology, consumer cyclical, and consumer defensive sectors led the market gains, each yielding total returns of approximately 8% or higher. Notably, the real estate sector was the sole sector to finish the quarter in negative territory, while the broader stock market rally exhibited resilience and breadth.

As of March 29, 2024, our flagship index – the JUST U.S. Large Cap Diversified Index (JULCD) has out-performed the Russell 1000 (Cap-Weighted) benchmark by 0.35% year-to-date and by 10.7% since its inception. Additionally, the JUST 100 (equally weighted index) has outperformed the Russell 1000 (Equally-Weighted) index by 4.47% year-to-date and by 43.46% since its inception.

JUST Capital found that three of the five stakeholders we track delivered positive performance in Q1 2024. The Communities stakeholder delivered the strongest performance over this period with a long-short spread of 5.19%, while the Customers stakeholder fared most poorly at -2.73%. Within the Workers stakeholder, outperformance was driven by the top decile whereas for Communities & Shareholders & Governance stakeholder outperformance was driven by both deciles. For the Customers stakeholder, underperformance was driven by both deciles whereas for Environment stakeholder negative contribution was driven by bottom decile.

JUST Capital’s Overall Weighted Score takes into account the 20 core Issues determined through our annual survey research – including paying a living wage, creating a diverse, inclusive workplace, and helping combat climate change – across key business stakeholders: Workers, Communities, Shareholders & Governance, Customers, and Environment. This Overall Weighted Score had a positive long-short spread of 4.9% over the period ending March 31,2024.

The Workers stakeholder measures a company across five Issues:

In Q1 2024, we saw all five issues deliver positive performance, with the Workforce Advancement Issue faring the best. Diversity Equity & Inclusion was the weakest performer amongst the Worker issues.

Shown below are the top and bottom five contributors to the top decile (D1), the top-ranked companies as measured by their Workers score, and the bottom decile (D10), the lowest-ranked companies as measured by their Workers score.

The Communities stakeholder measures a company across four Issues:

Local Job Creation was the strongest performer followed by Human Rights. All issues were positive in Q1 2024.

Shown below are the top and bottom five contributors to the top decile (D1), the best-ranked companies as measured by their Communities score, and the bottom decile (D10), the lowest-ranked companies as measured by their Communities score.

The Shareholders and Governance stakeholder measures a company across three Issues:

Investor Return Issue was the strongest performer in Q1 with a long-short spread of 13.77% followed by Accountability to Stakeholders issue whereas Ethical Leadership was negative this quarter.

Shown below are the top and bottom five contributors to the top decile (D1), the best-ranked companies as measured by their Shareholders and Governance score, and the bottom decile (D10), the lowest-ranked companies as measured by their Shareholders and Governance score.

The Customers stakeholder measures a company across four Issues:

In Q1 2024, three out of 4 Customer Issues delivered negative performance. Customer Privacy was the only positive contributor in Q1. Transparent Communication was the weakest performer followed by Customer Treatment.

Shown below are the top and bottom five contributors to the top decile (D1), the best-ranked companies as measured by their Customers score, and the bottom decile (D10), the lowest-ranked names as measured by their Customers score.

The Environment stakeholder measures a company across four Issues:

In Q1 2024, we saw two of four Environment Issues deliver positive performance. Resource Efficiency was the top contributor followed by Climate Change in Q1. Pollution Reduction and Sustainable Materials delivered negative performance this quarter.

Shown below are the top and bottom five contributors to the top decile (D1), the best-ranked companies as measured by their Environment score, and the bottom decile (D10), the lowest-ranked companies as measured by their Environment score.

We monitor the performance of these stakeholders and Issues on a long-short basis. The long and short portfolios are selected based on the factor scores as the top and bottom deciles within the universe of companies we track in the Russell 1000. Top decile (D1) companies are those that rank highest based on the factor score, and bottom decile (D10) companies are those that rank lowest based on the factor score.

D1 Performance is computed as

(Equally weighted average of returns of stocks in D1 bucket) – (Equally weighted average of returns of all stocks within the Universe)

D10 Performance is computed as

(Equally weighted average of returns of stocks in D10 bucket) – (Equally weighted average of returns of all stocks within the Universe)

Spread is computed as

D1 Performance – D10 Performance

This report was written by Mona Patni, Director of Quantitative Research & Analytics.

After a strong start to 2023, the Russell 1000 was down 3.15% in Q3, bringing its year-to-date gains to 13%. On a sector level, nine of the 11 Russell 1000 sectors finished the third quarter with negative returns, a stark reversal from the broad gains of the second quarter. Energy was, by far, the best-performing sector, thanks to a surge in oil prices driven by oil production cuts from Saudi Arabia and Russia. Communications Services also finished Q3 with a slightly positive quarterly return, driven in part by hopes that advanced artificial intelligence would boost search and social media companies’ future advertising revenues.

Looking at sector laggards, the impact of rising bond yields was again clearly visible as Consumer Staples, Utilities, and Real Estate were the lowest-performing sectors in the third quarter. Those sectors offer some of the highest dividend yields in the market, but with bond yields quickly rising, those dividend yields become less attractive, leading investors to rotate out of the high-dividend sectors and into less-volatile bond funds as a result. The IT sector also was one of the weakest this quarter.

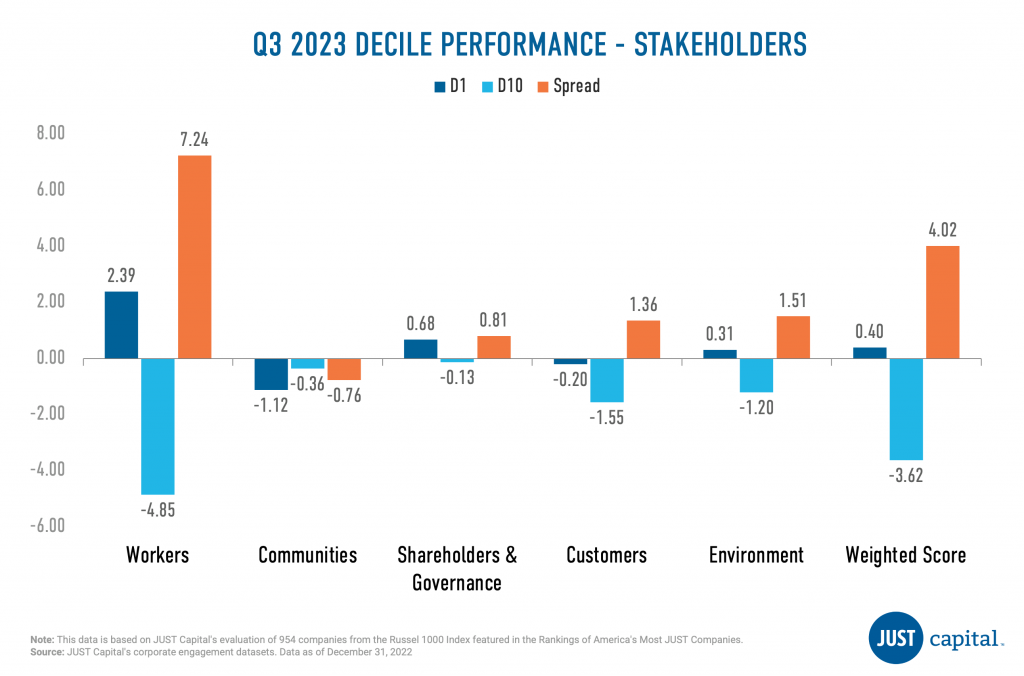

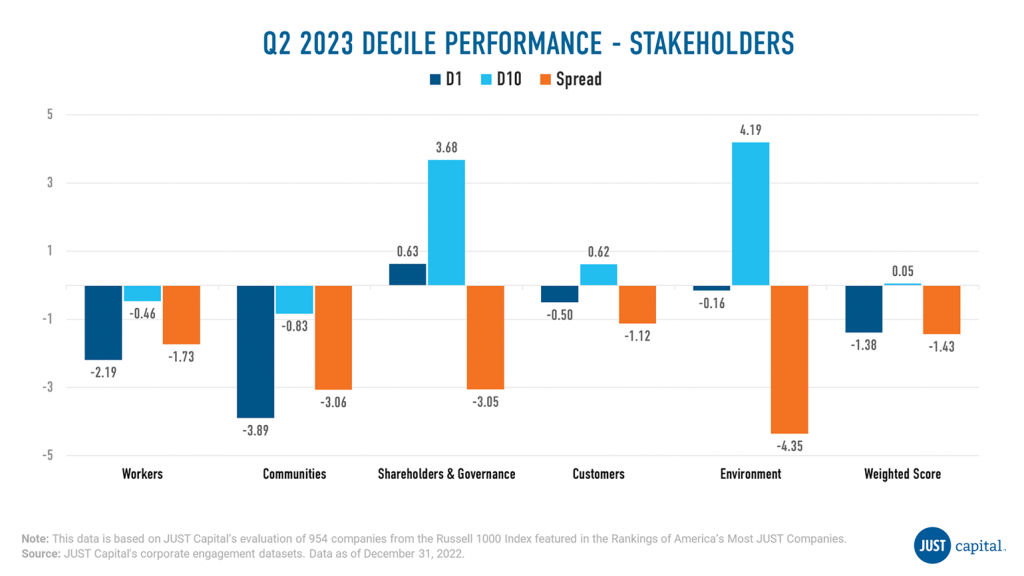

JUST Capital found that four of the five stakeholders we track delivered positive performance in Q3 2023. However, over the longer term from Jan 2018 to September 2023, the leaders in corporate stakeholder performance across all five stakeholders have outperformed the laggards by 56.5% as measured by JUST Overall Score. In Q3 2023, the Workers stakeholder delivered the strongest performance over this period with a long-short spread of 7.24%, while the Communities stakeholder fared most poorly at -0.76%. Within the Workers, Shareholders & Governance, and Environment stakeholders, outperformance was driven by both deciles, with the top decile outperforming and bottom decile underperforming. For the Communities stakeholder, underperformance was driven by the top decile, whereas for the Customer stakeholder, the top decile underperformed.

JUST Capital’s Overall Weighted Score takes into account the 20 core Issues determined through our annual survey research – including paying a living wage, creating a diverse, inclusive workplace, and helping combat climate change – across key business stakeholders: Workers, Communities, Shareholders & Governance, Customers, and Environment. This Overall Weighted Score had a positive long-short spread of 4.02% over the period ending September 30, 2023, which was an improvement from Q2 2023 at -1.43%.

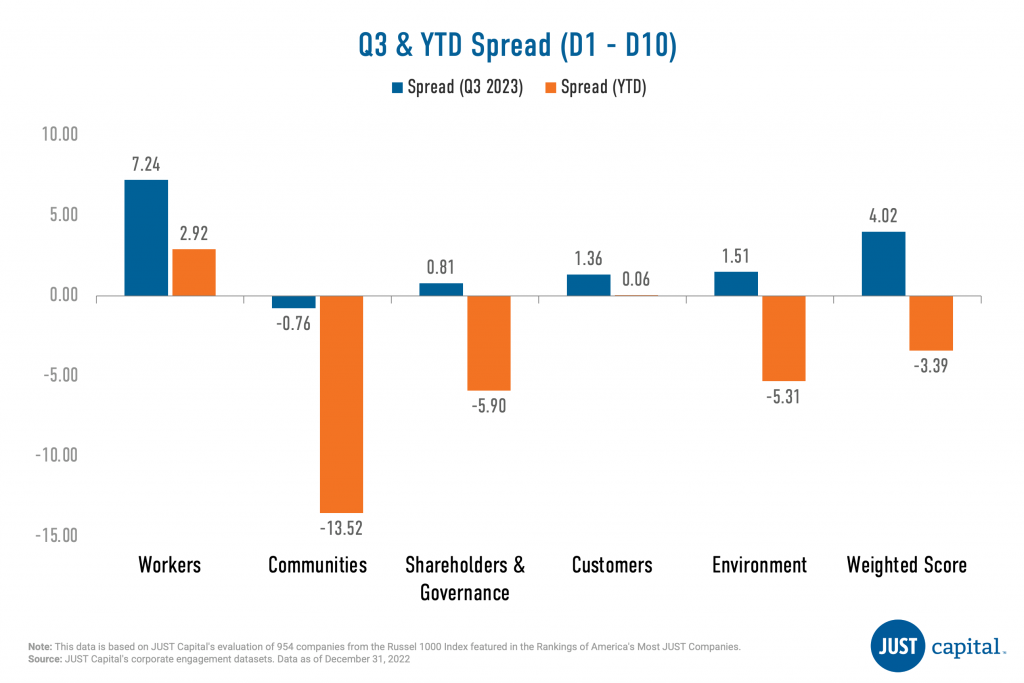

Shown below is the Year-to-Date (YTD) and Q3 performance, which is quantified by the spread between the top and bottom deciles for each stakeholder as well as the overall weighted score. Year-to-date, the Workers stakeholder has delivered the strongest performance and the Communities stakeholder has delivered the weakest.

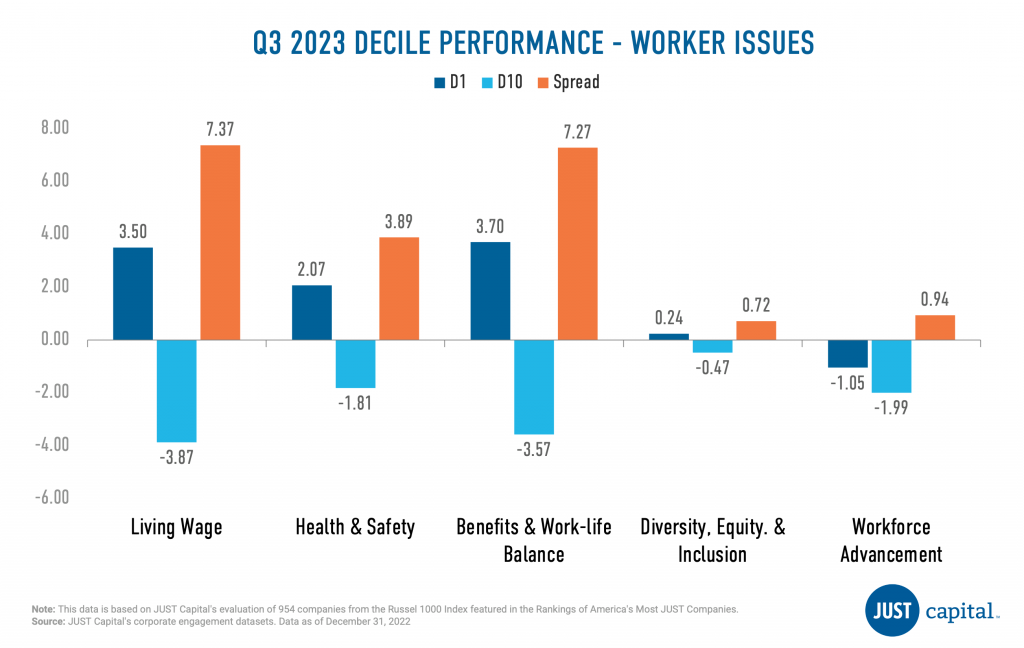

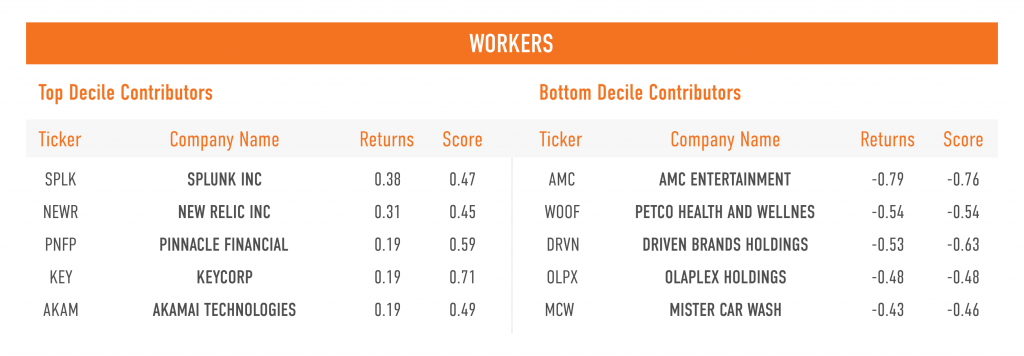

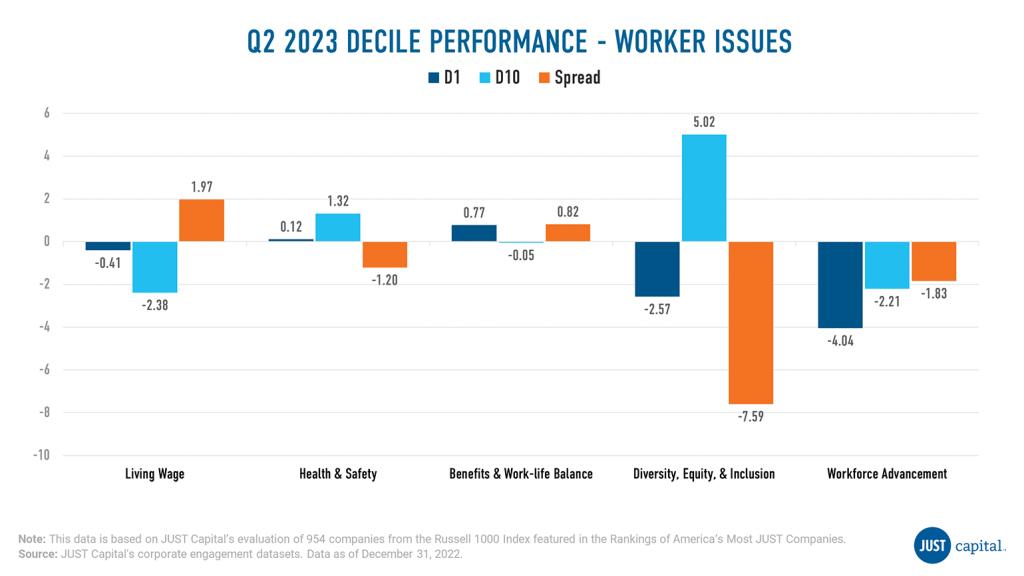

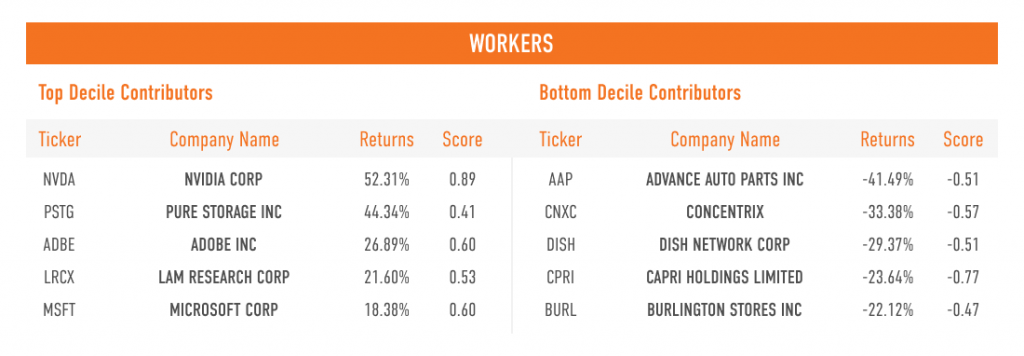

The Workers stakeholder measures a company across five Issues:

In Q3 2023, we saw all five issues deliver positive performance, with Living Wage and Benefits Issues faring the best. Outperformance in all Issues – except Workforce Advancement – was driven by contribution from both top and bottom decile companies, whereas within Workforce Advancement, positive contribution was driven only by the bottom decile.

Shown below are the top and bottom five contributors to the top decile (D1), the top-ranked companies as measured by their Workers score, and the bottom decile (D10), the lowest-ranked companies as measured by their Workers score.

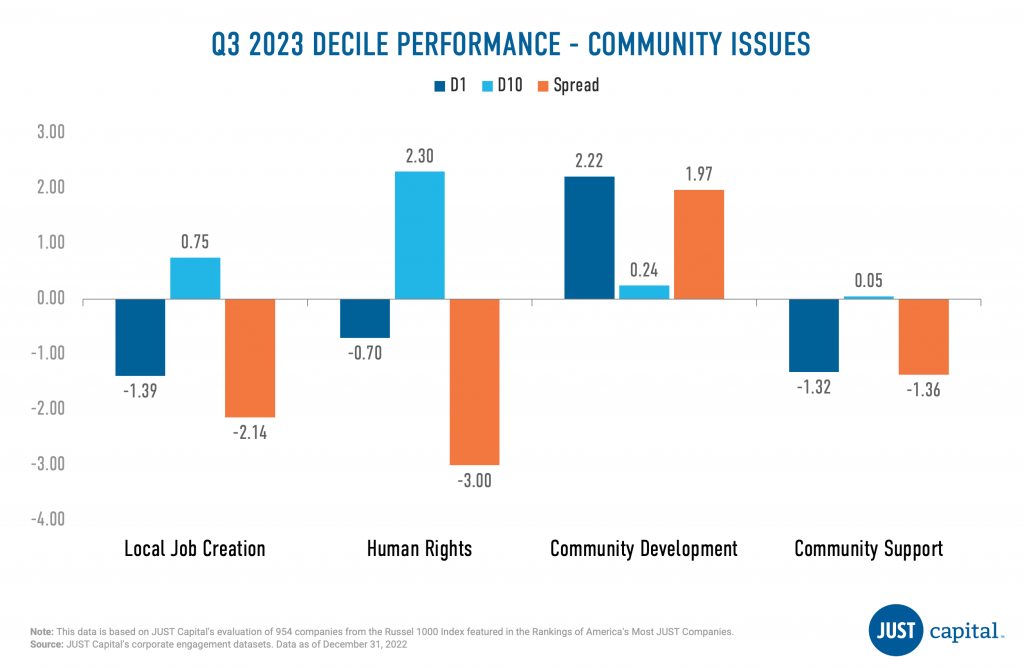

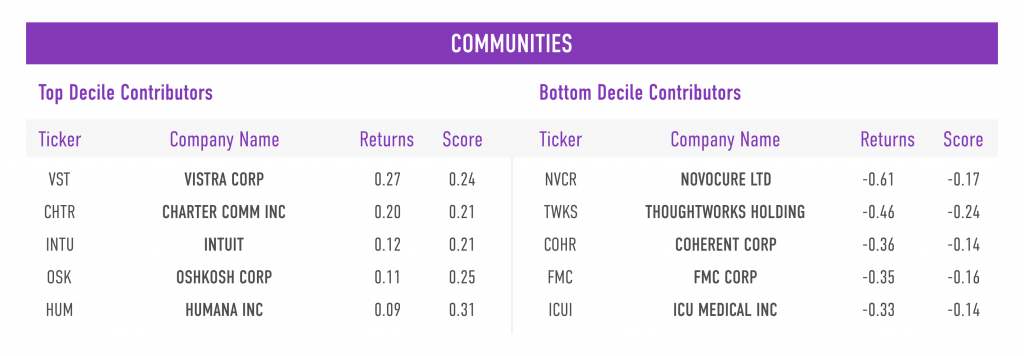

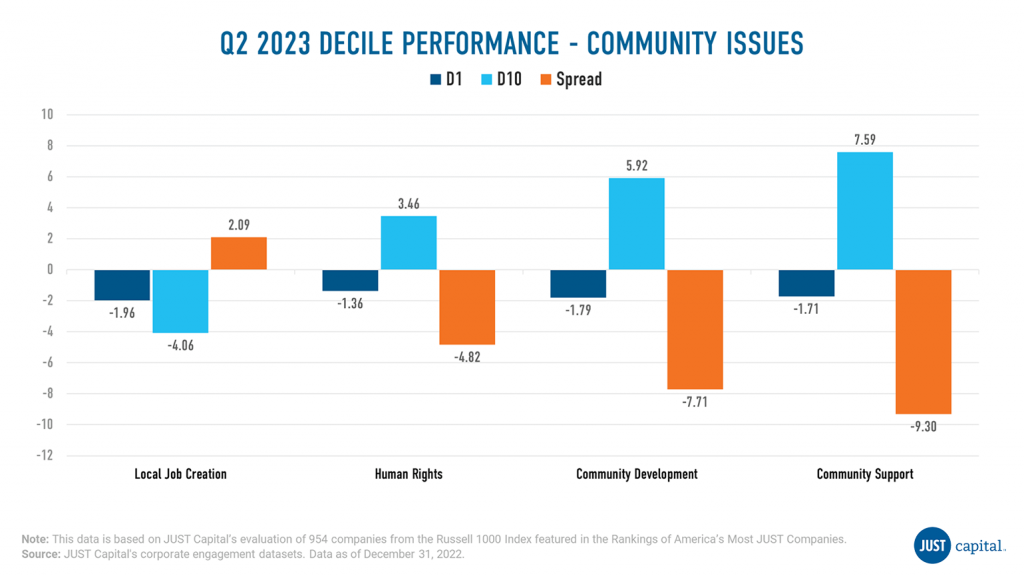

The Communities stakeholder measures a company across four Issues:

Human Rights was the weakest performer followed by Local Job Creation, with negative contributions coming from both top and bottom decile companies.

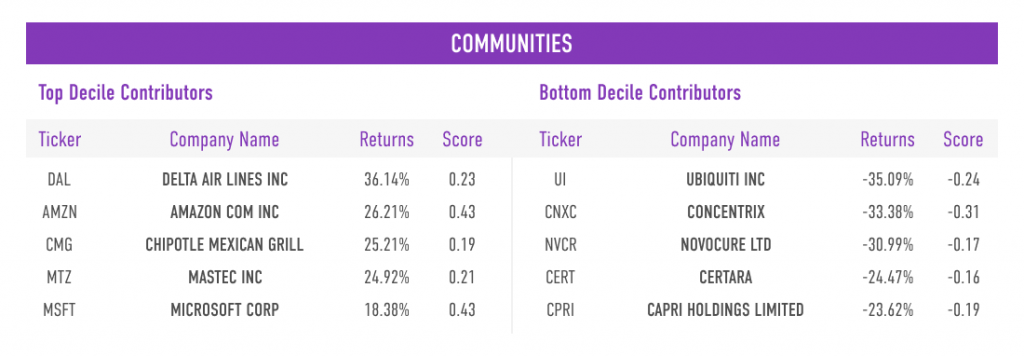

Shown below are the top and bottom five contributors to the top decile (D1), the best-ranked companies as measured by their Communities score, and the bottom decile (D10), the lowest-ranked companies as measured by their Communities score.

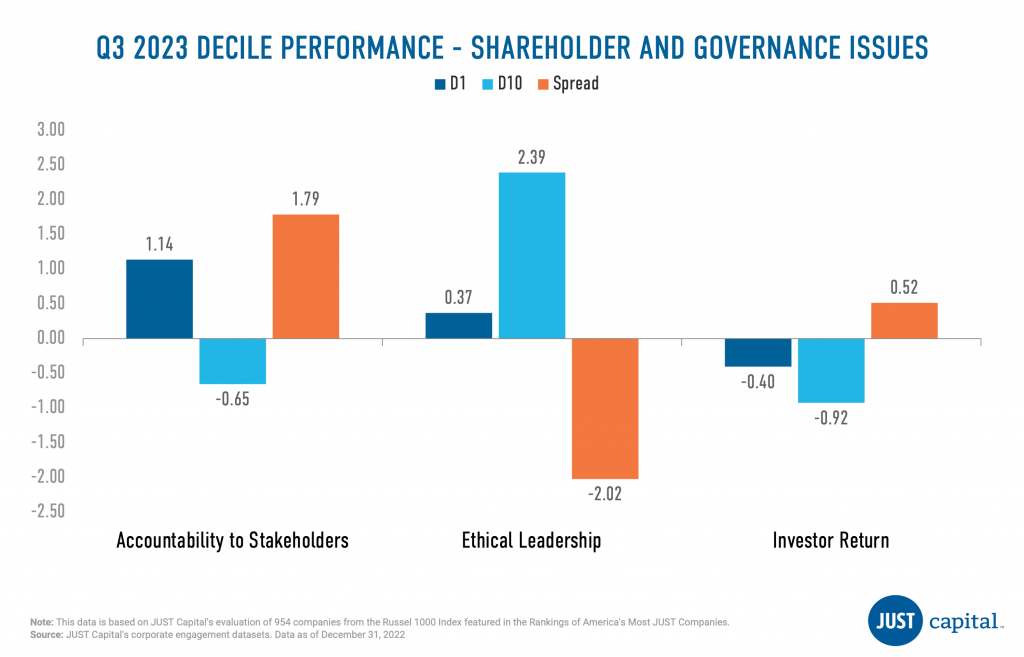

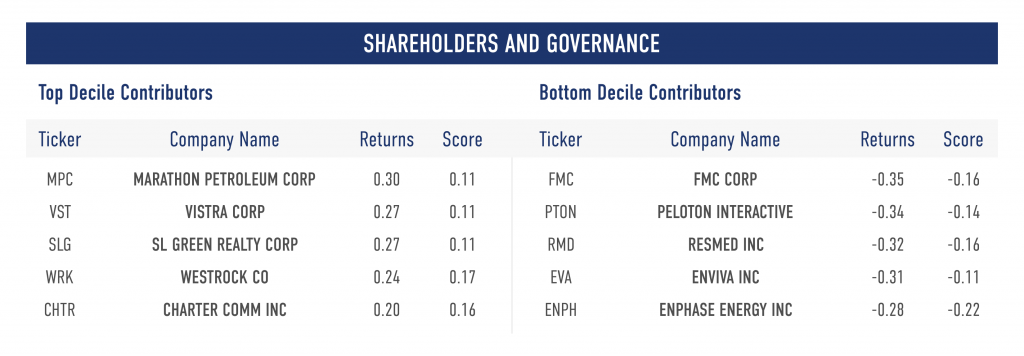

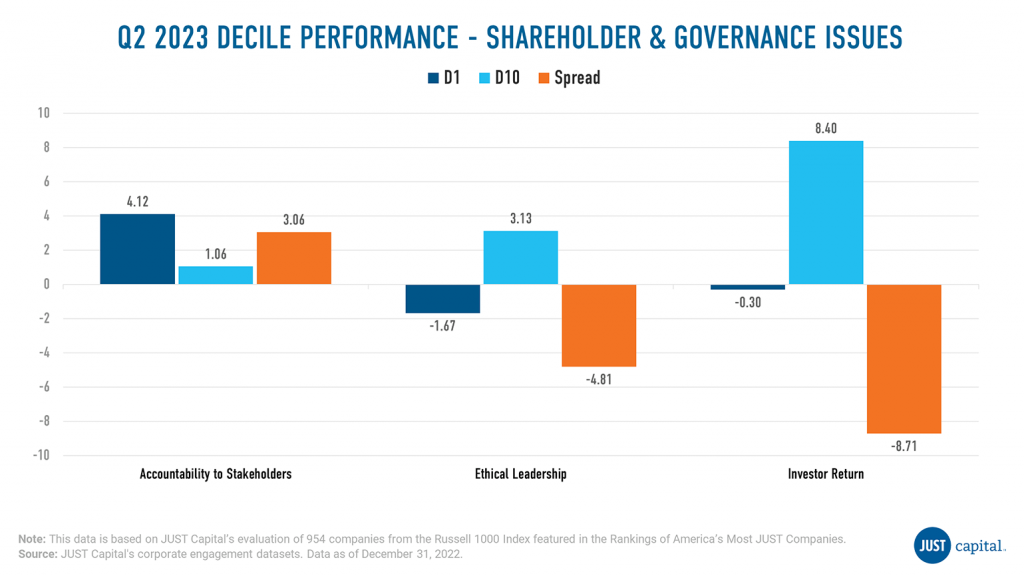

The Shareholders and Governance stakeholder measures a company across three Issues:

In Q3 we saw the Accountability to Stakeholders Issue deliver positive performance, with a long-short spread of 1.79%, whereas Ethical Leadership performance was negative. Investor Return was also positive this quarter.

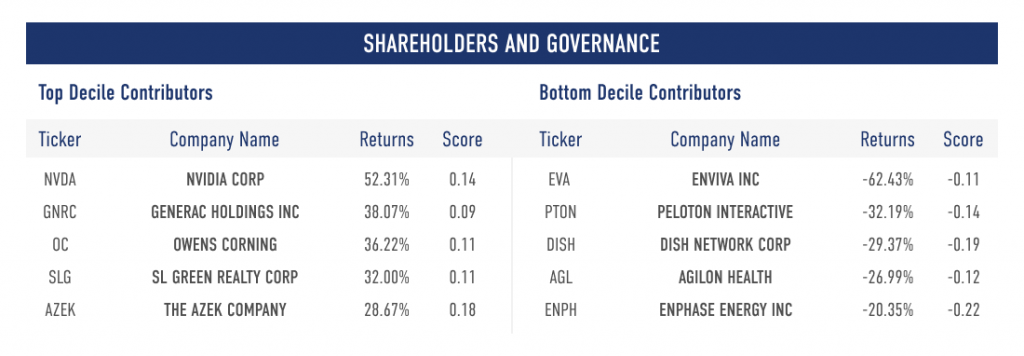

Shown below are the top and bottom five contributors to the top decile (D1), the best-ranked companies as measured by their Shareholders and Governance score, and the bottom decile (D10), the lowest-ranked companies as measured by their Shareholders and Governance score.

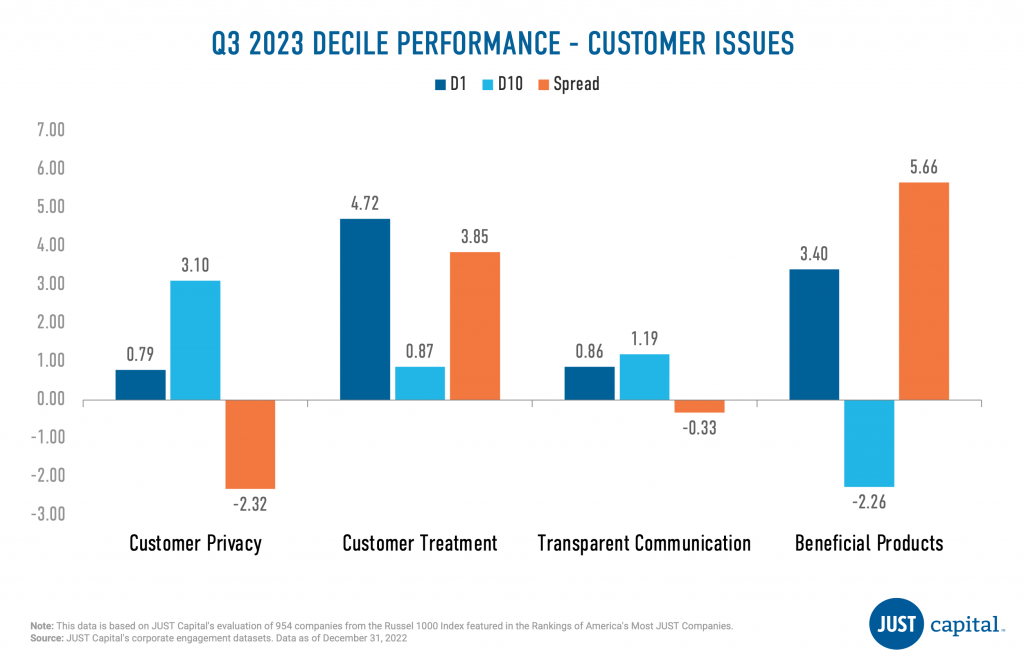

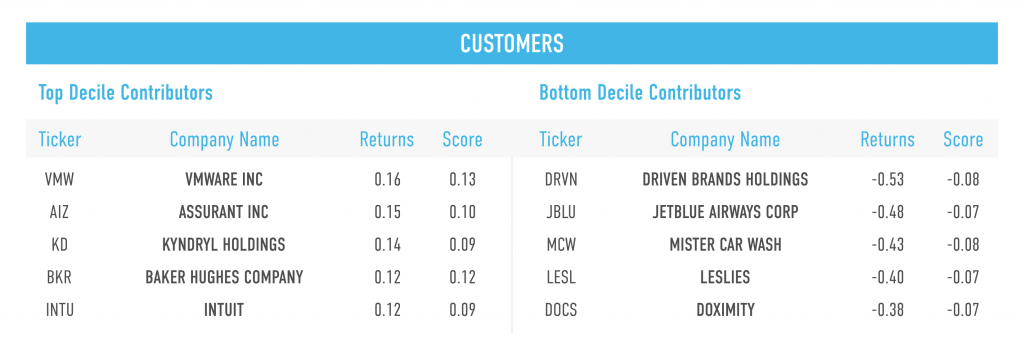

The Customers stakeholder measures a company across four Issues:

In Q3 2023, we saw Beneficial Products outperform the other Customer Issues, with a long-short spread of 5.6%. Customer Treatment was also positive whereas Customer Privacy and Transparent Communication were negative contributors to Customers performance.

Shown below are the top and bottom five contributors to the top decile (D1), the best-ranked companies as measured by their Customers score, and the bottom decile (D10), the lowest-ranked names as measured by their Customers score.

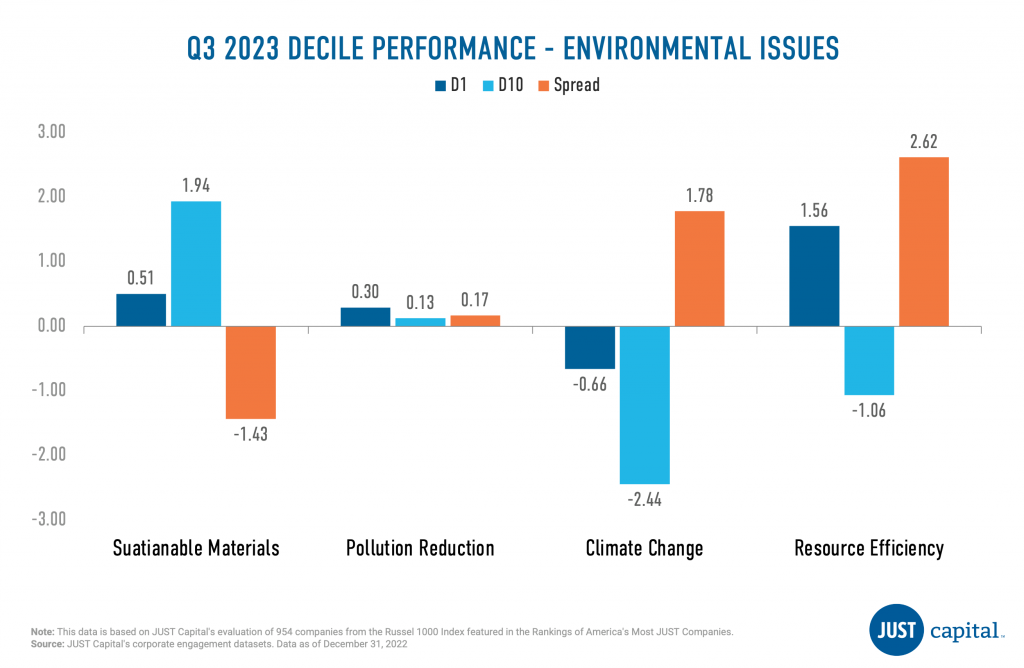

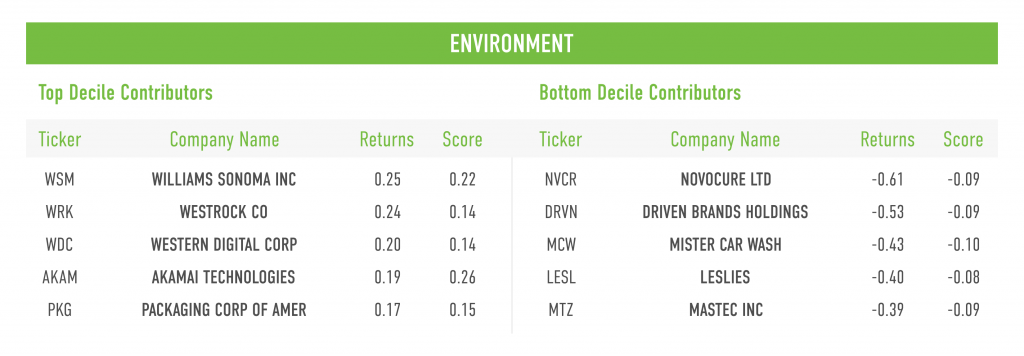

The Environment stakeholder measures a company across four Issues:

In Q3 2023, we saw three of four Environment Issues deliver positive performance, with Sustainable Materials being a negative contributor this quarter.

Shown below are the top and bottom five contributors to the top decile (D1), the best-ranked companies as measured by their Environment score, and the bottom decile (D10), the lowest-ranked companies as measured by their Environment score.

Computation Methodology

We monitor the performance of these stakeholders and Issues on a long-short basis. The long and short portfolios are selected based on the factor scores as the top and bottom deciles within the universe of companies we track in the Russell 1000. Top decile (D1) companies are those that rank highest based on the factor score, and bottom decile (D10) companies are those that rank lowest based on the factor score.

D1 Performance is computed as

(Equally weighted average of returns of stocks in D1 bucket) – (Equally weighted average of returns of all stocks within the Universe)

D10 Performance is computed as

(Equally weighted average of returns of stocks in D10 bucket) – (Equally weighted average of returns of all stocks within the Universe)

Spread is computed as

D1 Performance – D10 Performance

This report was written by Mona Patni, Director of Quantitative Research & Analytics.

Stocks extended their rally in the second quarter, boosted by cooling inflation, the prospect of a shift in monetary policy, and enthusiasm over artificial intelligence, with the bulk of the gains made in June. The Russell 1000 Index was up 8.6% in Q2 2023, bringing its YTD return to 16.67%. With respect to sector performance, IT companies led the stock market advance in the quarter, while the consumer discretionary and communication services sectors also performed strongly. Underperforming sectors included energy and utilities.

JUST Capital found that all five stakeholders we track delivered negative performance in Q2 2023. However, over the longer term from Jan 2018 to June 2023, the leaders have outperformed the laggards by 52.13% as measured by JUST Overall Score. In Q2 2023, the Customers stakeholder delivered the strongest performance over this period with a long-short spread of -1.12%, while the Environment stakeholder fared most poorly at -9.11%. Within the Customers and Environment stakeholders, underperformance was driven by both deciles, with the top decile underperforming and bottom decile outperforming. For the Workers and Communities stakeholders, underperformance was driven by the top decile, whereas for the Shareholders & Governance stakeholder underperformance was driven by the bottom decile.

JUST Capital’s Overall Weighted Score takes into account the 20 core Issues determined through our survey research – including paying a living wage, creating a diverse, inclusive workplace, and helping combat climate change – across key business stakeholders: Workers, Communities, Shareholders & Governance, Customers, and Environment. This Overall Weighted Score had a negative long-short spread of -1.43% over the period ending June 30, 2023 which was an improvement from Q1 2023 at -7.14%, but still not positive.

Negative contribution to the top decile of the Overall Weighted Score was driven primarily by the Industrials and Consumer discretionary sectors. Basic Materials, Real Estate, and Technology companies were positive contributors to the top decile. Overweight stocks like Illumina (-19.38%) and Target (-19.82%), and underweight companies like Carvana (164.76%), didn’t help the performance of the top decile of the Overall Weighted Score. On the other hand, the bottom decile, which consists of low performers as measured by stakeholder performance, delivered close to neutral performance. Negative contributions largely came from Financials and Health Care names, while bottom decile companies like Carnival Corp (Consumer Discretionary) and Builders FirstSource Inc (Industrials) rallied during this quarter.

The Workers stakeholder measures a company across five Issues:

In Q2 2023, we saw Living Wage and Benefits Issues deliver positive performance whereas DEI fared most poorly. Underperformance in DEI & Workforce Advancement was driven by negative performance from both top and bottom decile companies, whereas negative performance in Health & Safety came from bottom decile names.

Shown below are the top and bottom five contributors to the top decile (D1), the top-ranked companies as measured by their Workers score, and the bottom decile (D10), the lowest-ranked companies as measured by their Workers score.

The Communities stakeholder measures a company across four Issues:

Community Support was the weakest performer followed by Community Development and Supply Chain, with negative contributions coming from both top and bottom decile companies.

Shown below are the both top and bottom five contributors to the top decile (D1), the best-ranked companies as measured by their Communities score, and the bottom decile (D10), the lowest-ranked companies as measured by their Communities score.

The Shareholders and Governance stakeholder measures a company across three Issues:

In Q2 we saw the Accountability to Stakeholders Issue deliver positive performance, with a long-short spread of 3.1%, whereas Ethical Leadership and Investor Return performance was negative.

Shown below are both the top and bottom five contributors to the top decile (D1), the best-ranked companies as measured by their Shareholders and Governance score, and the bottom decile (D10), the lowest-ranked companies as measured by their Shareholders and Governance score.

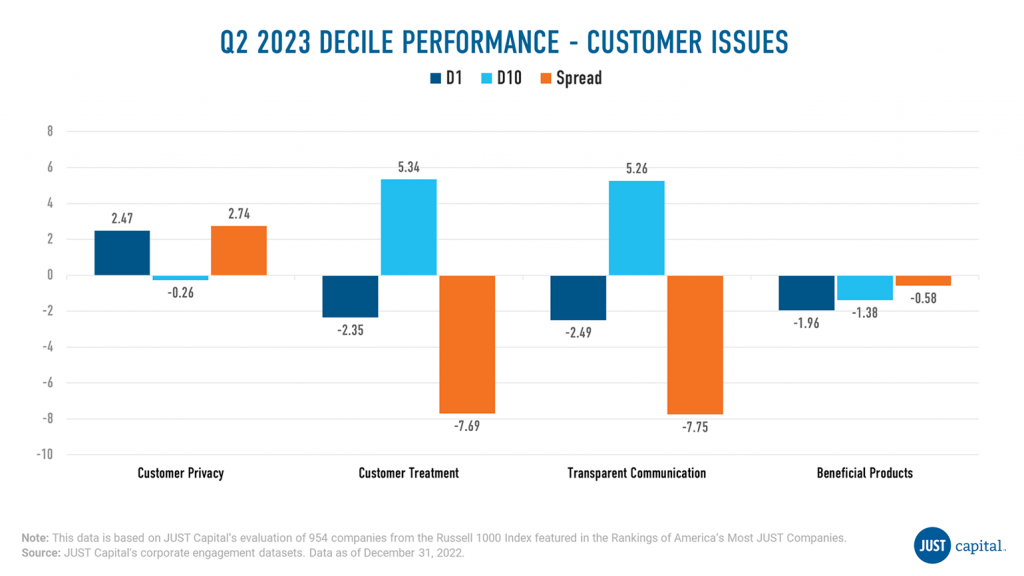

The Customers stakeholder measures a company across four Issues:

In Q2 2023, we saw Customer Privacy outperform the other Customer Issues, with a long-short spread of 2.7%. Beneficial Products, Customer Treatment, and Transparent Communication were negative contributors to Customers performance.

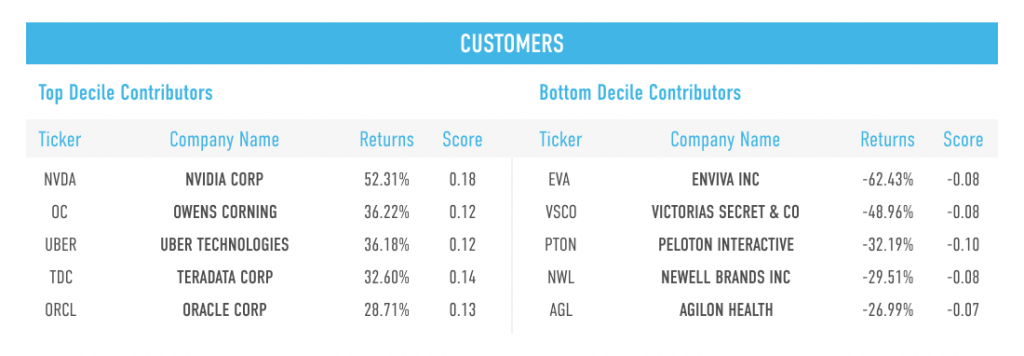

Shown below are both the top and bottom five contributors to the top decile (D1), the best-ranked companies as measured by their Customers score, and the bottom decile (D10), the lowest-ranked names as measured by their Customers score.

The Environment stakeholder measures a company across four Issues:

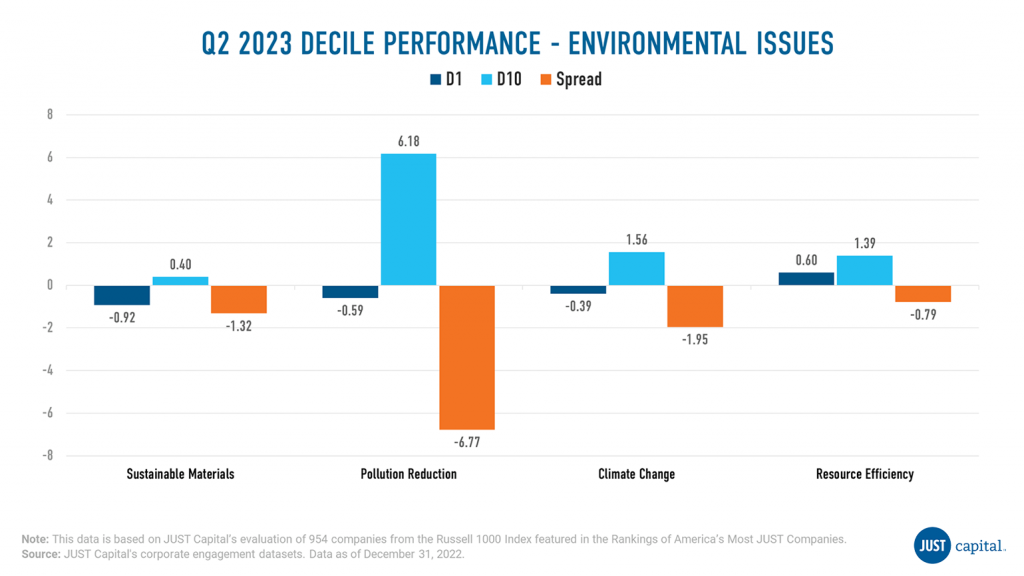

In Q2 2023, we saw all Environment Issues deliver negative performance, with Pollution Reduction being the weakest.

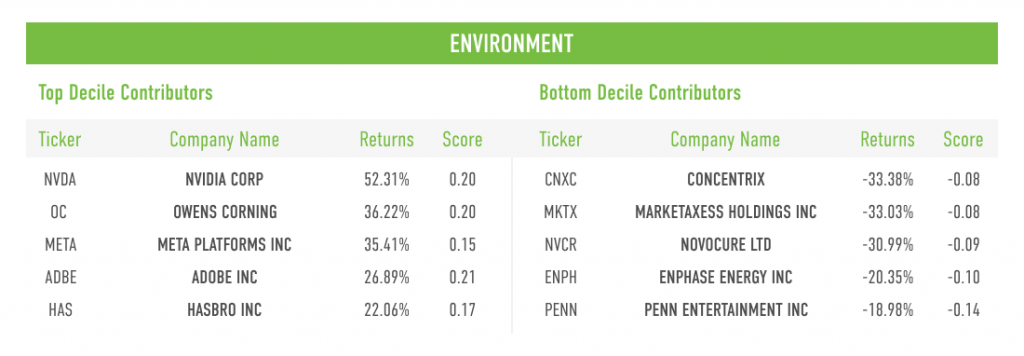

Shown below are both the top and bottom five contributors to the top decile (D1), the best-ranked companies as measured by their Environment score, and the bottom decile (D10), the lowest-ranked companies as measured by their Environment score.

Computation Methodology

We monitor the performance of these stakeholders and Issues on a long-short basis. The long and short portfolios are selected based on the factor scores as the top and bottom deciles within the universe of companies we track in the Russell 1000. Top decile (D1) companies are those that rank highest based on the factor score, and bottom decile (D10) companies are those that rank lowest based on the factor score.

D1 Performance is computed as:

(Equally weighted average of returns of stocks in D1 bucket) – (Equally weighted average of returns of all stocks within the Universe)

D10 Performance is computed as:

(Equally weighted average of returns of stocks in D10 bucket) – (Equally weighted average of returns of all stocks within the Universe)

Spread is computed as:

D1 Performance – D10 Performance

Earlier this week, JUST Capital marked its five-year anniversary of the JUST ETF with a panel series at the New York Stock Exchange. The ETF was launched in 2018 in partnership with Goldman Sachs Asset Management to track the top 50% of Russell 1000 companies according to the priorities of the American public.

At the event, CNBC’s Leslie Picker moderated a riveting conversation titled “The Value of Investing in Just Business” featuring Priscilla Sims Brown, CEO of Amalgamated Bank, the financial institution self-described as “America’s socially responsible bank” with $7.8 billion in assets and $53.6 billion in custody and investment assets under management, as well as Roy Swan, Director of Mission Investments at the Ford Foundation, one of the largest private foundations in the U.S. with a $16 billion endowment and a commitment to addressing inequality. (Note: Ford Foundation is a JUST Capital Foundation Partner).

Brown and Swan delivered multiple key insights on how CEOs and business leaders can create shareholder value while also prioritizing other stakeholders like workers, communities, and the environment.

CNBC’s Picker kicked off the discussion by asking Brown and Swan to weigh in on the bottom-line case for just business behavior.

Swan discussed how prioritizing workers and communities is at the heart of American capitalism. He explained that visionary economist and “Wealth of Nations” author Adam Smith’s theory of the “invisible hand” was not intended to keep markets completely unchecked, but to advance the success of the economy through self-interest that creates mutually beneficial, interdependent outcomes.

Swan added that he uses the phrase “patriotic capitalism” to encapsulate the business case for just corporate behavior.

“Patriotic capitalism is a capitalism that puts the interest of country, democracy, and the common good first,” he said. “It is enlightened self-interest that understands that capitalism is best optimized and sustained when our country, democracy and the common good are prioritized. Otherwise, there is no American economy.”

Amalgamated Bank CEO Brown agreed that value for workers and their families lies at the center of American capitalism.

“At Amalgamated Bank, we’re a living experiment of doing well by doing good. And it’s working,” she said.

“We’re making the business case by taking stands on a few core issues like gun violence in America and reproductive rights. We’re transparent in our values, you can read about them on our website. That transparency is key to driving good business and financial outcomes,” she added.

Both Brown and Swan underscored the importance of leveraging more data to continue building the case for just business behavior.

“The more we show the numbers underscoring the business case for doing good, the stronger the case becomes,” Brown said. “We need more research and data, especially on costs and controls for externalities.”

Swan cited research showing how prioritizing workers, specifically worker engagement, results in shareholder value. Loyal, engaged workers produce more, are out sick less, and have lower turnover, research has shown. That translates into “billions of dollars in profits” for a corporation and its shareholders, he explained.

Swan and Brown agreed that ESG and impact investing have come under intense scrutiny over the past several months, and acknowledged that it’s creating more questions for CEOs. However, both leaders agreed that the move toward transparency and corporate disclosure is here to stay.

“The term ‘ESG’ has been weaponized by polarizing opportunists who want to divide us,” Swan said. “A lot of arguments against ESG are actually arguments against impact investing which, unlike ESG disclosures, actually does seek specific outcomes.”

He explained that while impact investing might want to increase the number of good jobs for workers, or increase the number of companies that produce renewable alternatives to fossil fuels, ESG is a disclosure framework. “The movement of governments around the world who value a framework to disclose non-GAAP information isn’t going away.”

Brown added that she’s hopeful about the future of just corporate behavior. Swan concurred, citing JUST Capital’s recent newsletter highlighting a shift among some Republicans toward embracing a stakeholder model, pointing to what he calls a potential “thawing” of the movement against what’s been labeled “woke capitalism.”

“Call it ESG. Don’t call it ESG. Call it global warming. Don’t call it global warming,” Brown said. “The point is – keep pushing forward on issues that matter on a values level.”