UVA Darden School of Business

That there is even a mainstream debate about stakeholder capitalism is good news to R. Edward Freeman, professor at the University of Virginia’s Darden School of Business. “I’ve been at this since 1977,” he said, laughing, referring to his first paper on the subject. “Eventually, some people start to pay attention. I don’t mean to me, but to the idea.”

Freeman has been quick to point out from the beginning that he did not coin the term “stakeholder” in a business context – he points to the work of the Stanford Research Institute and others in the 1960s – but his work in the ’80s developed an idea of business with responsibilities to more than shareholders into a practical management theory. It’s why we spoke to him ahead of the second anniversary of the Business Roundtable’s stakeholder-centric Statement on the Purpose of a Corporation. It was a statement that surprised him when it was released in 2019, but one that also made him happy.

We discussed some of the accompanying critiques of stakeholder capitalism that have been frequent over the past couple weeks, whether alleging the approach is misguided, impossible to truly achieve, or nothing more than “woke” nonsense. To him, these are variations of the same arguments that have existed for decades, from critics who are unwilling or unable to see shareholder and stakeholder value as linked. He also believes that the stakeholder movement has momentum beyond a tipping point. “There’s no going back,” he said.

By the time Freeman arrived at the Wharton School of the University of Pennsylvania as a postdoctoral researcher in 1976, he had spent years studying mathematics and philosophy, both economic and otherwise. His next challenge was management theory, and his boss at the time wanted him to see what was behind the stakeholder ideas being tossed around. That led to 1984’s “Strategic Management: A Stakeholder Approach.” The text is now regularly referred to in management research as foundational to an increasingly popular approach, but at the time failed to make an impact.

It wasn’t until the ‘90s, when shareholder primacy was the norm, even for the BRT, that he saw a renewed interest in his work. That accelerated with the financial crisis and then with what he calls “a perfect storm” of social movements, rising inequality, and political instability that followed. Freeman joined the board of Whole Foods founder John Mackey’s Conscious Capitalism organization, and has spent years consulting corporate leaders.

Early in our discussion, Freeman alluded to the way many Business Roundtable CEOs said their latest statement was less reactionary to these forces than a proclamation of how they had long been approaching business. Critics have latched onto that point as proof that the statement was a marketing gimmick, but Freeman explained his interpretation before jumping to one of of stakeholder capitalism’s prominent critics, Vivek Ramaswamy, whose book “Woke, Inc.” was released the day Freeman spoke with us.

The following interview has been edited for length and clarity.

Prof. R. Edward Freeman: Now that we realized this, we can get better at it. We can improve it. We can look for how creating value for customers affects communities or suppliers, etc. And there are lots of companies out doing that. So I’m extremely optimistic about that.

And no, I haven’t read “Woke, Inc.,” because a review I read pissed me off so much. “Woke” [used by critics to mean disingenuously or suffocatingly progressive] is one of those phrases like “political correctness” – it stops arguments. “Oh, you’re woke, so therefore I’m going to discount you.” I’m a philosopher by training and phrases that stop arguments like that are formal fallacies.

On the other hand, over the years, I’ve managed to piss off the left and the right. Left, they think I’ve sold out to business, and they don’t think business can do anything good.People on the right, on the other hand, think I’m a socialist. But I actually think what stakeholder capitalism is, it’s about the business model. It’s about how business actually works in the real world.

But there are a lot of people who are in the grip of this old story. They just can’t imagine business as anything but a duality between stakeholders and shareholders. I’ve never thought that was interesting.

JUST Capital: When you see recent pushback, are they the same arguments that you’ve been seeing for decades at this point?

Freeman: Oh, God, yes. I mean, none of this stuff is new. It’s a little bit like Wall Street and the academic world, finance and accounting people, have discovered ESG. Well, wait a minute. That’s been around since Abt Associates [a research institution that began using “social audits” in 1971 as a way of measuring benefits and costs of its research on its stakeholders]. Let’s get out of the grip that it’s only economics that counts. Let’s look at business as a societal institution.

JUST: There is another form of pushback that can start with, “We agree with these theories, but the companies that say they are following them are lying.” Harvard’s Lucian Bebchuk and Roberto Tallarita have argued that there is no evidence BRT companies are following their statement of purpose.

Freeman: Arguments like, “Everybody’s lying, here’s what’s really going on,” are problematic. Even if all you care about is making money for shareholders, how are you going to do it? You’re going to have great products and services for customers, suppliers who want to make you better, employees who want to be engaged in the company, and communities who want you or at least allow you to operate. I’ve only looked very briefly at the Bebchuk paper, but I’ve heard for a lot of years he’s very much caught up in the sort of standard way to think about governance. I read the law, even, differently. I read it as saying directors have a duty of care to the corporation. And what’s the duty of care to the corporation? Well, I’d pay attention to how they create value for their stakeholders.

Again, I think seeing it as a duality between stakeholders on the one hand and shareholders on the other is a mistake. That’s not to say that there aren’t some people acting in bad faith. But for the most part, I don’t believe businesspeople are like that.

JUST: Do you reject the premise of the argument, then, that for stakeholder capitalism to be real, that governance and bylaws within a company would have to be changed?

Freeman: I don’t think that at all. There’s this idea that you have to eschew shareholder value, but that that’s ridiculous. Companies have to make money. It’s a lie to say, well, they’re only stakeholder capitalists if they put making money second. No, what they might do is see them as connected.

JUST: Arguments do exist that a full rethink of how companies make money and function is needed – like Sen. Elizabeth Warren’s “Accountable Capitalism” message bill – but I’ve never seen that as the primary stakeholder capitalism take. Critics often do, however, and I wonder if they’re conflating those positions by mistake or in bad faith, because it’s easier to turn down for a broader audience.

Freeman: I think there’s some of both.

There are at least four ways you can understand stakeholder capitalism. The first way is this is just PR – greenwashing and virtue signaling. The second way is well, people mean it, but this is really just CSR [corporate social responsibility], just dealing with social issues. The third way is around top-down elites and government policy shaping business.

The fourth way is about the business model, and this is about understanding how business actually works. And that’s been my view for 40-plus years.

There’s a great back and forth with Milton Friedman and John Mackey a number of years ago, before Friedman died. [Freeman considers Friedman a “hero” for his research on markets, but believes he misunderstood how corporations operate.]

And it was clear that Mackey understood this the same way I did. We might need some top-down stuff, we might need to change how we think about capital markets, we certainly need better PR, and we need to worry about social issues – but fundamentally we need to change the story about business.

JUST: To me, the rise of stakeholder capitalism is linked to the rise of ESG investing. SEC chair Gary Gensler has said there’s going to be standardized ways of reporting climate impact from companies and then it’s highly likely that there will be some human capital metrics standards after that. Do you think companies should be run in the way where you’re looking at potential value creation and risks in things like climate and the composition of your workforce, or should ESG analysis be relegated to a form of investment? How do you see it?

Freeman: I would look at it slightly differently. The perfect storm here is a function of what happened in the global financial crisis. Add global warming, Black Lives Matter, Me Too, inequality on a global level, and political instability. What you get is a recognition that we need to change the way we think about this.

If you think the right way to think about a business, evaluating it from the outside, looking at the risks to the future cash flows, then you’re going to see risk in all of those things. And there’s nothing wrong with that – that’s right. If you’re on the inside, you’ve got to probably start from a different perspective.

Some people will look at that just in terms of the risks of the future cash flows, but some people will look at it in terms of what they stand for while they’re here. Purpose matters to most human beings. And I think, [BlackRock CEO] Larry Fink would say purpose might drive profitability. Again, we’re realizing how those things are intertwined.

There’ll be some standardized versions of ESG, but I’m a little skeptical of having that too standardized. When you do that you lose opportunities for people to do it differently. And one of the things we know about businesses is they’re not all the same. And so their ability to deal with things like global warming or inequality are different. From the company perspective, we need companies innovating.

ESG is great. I’m all for it. I’m a little amused by it, because it’s a new toy that people think they have just invented. But I’m also like, “Great, welcome to the big tent of stakeholder capitalism.”

JUST: I’ve seen the same arguments around management repeated in articles and research over the past century of American business. And in the ’70s, you can find almost identical arguments to today around CEOs getting too bold in taking political stances. But we’ve also seen in our polling research that the public, across demographics, does want CEOs to take stands. Yes, they tend to want them to take stands that they agree with, but they are looking for them to step up, which I think is fascinating. How do you believe this has evolved?

Freeman: Well, I’ve recently had conversations with a number of CEOs who have said things like, “I know I have to do stuff here. I just don’t know how.” That’s been an issue – I’ve started a new course called “Societal Issues in Business,” trying to help students figure out how to do it. Look, not taking a position is taking a position. So the idea that you can escape from this by saying, “Well, I only deal with economic issues,” that’s a political position – it’s a position that says economics and politics are completely separate, which we know certainly from Adam Smith on is a foolish idea.

Now, Friedman said we elect officials to do this. He was worried for the most part about corporate philanthropy, about executives supposedly giving away owners’ money. But setting that aside for a minute, he was also worried about companies doing stuff that they didn’t know anything about – and I agree that’s worrisome. I much rather see companies trying to figure out, for instance, how they can offer up opportunities with their business model to people who’ve been shut out of the system, or how they can encourage their employees to be community builders in the communities where they live. One of the other vectors that we have going on here is the multi-sector, multi-stakeholder partnerships where you have NGOs, governments, and companies sharing their expertise to deal with societal problems. I think that’s an equally important thing that’s going on.

And around polling – of course, you’re right. The public is firmly behind stakeholder capitalism. There’s not much ambiguity about that.

JUST: Do you see this moment as a turning point, similar to the way that shareholder primacy gradually went from fringe to mainstream ideologically, and then became ingrained through corporate leadership, judgments, and deregulation? Is the pendulum swinging back?

Freeman: Yeah, I think it is. I actually think we’ve gone past the tipping point. Nobody’s arguing that what we really need to fix everything is to double down on shareholder value. And for good reason – it doesn’t work. The best you can say about it is it’s incomplete.

What causes a company to be profitable is how it manages its other stakeholder relationships. We’ve come to understand that. One of the other things that goes on, at least here in the U.S., is of course younger people are demanding this of where they work, and that’s a good thing. The forces are such that I don’t think there’s any going back.

(John Moore/Getty Images)

Someone asked me a great question during a presentation earlier this week: “How can the stakeholder model lend American corporations a competitive advantage on the world stage?”

The more I ponder this, the more I realize it is in fact a defining proposition.

Most obviously, it speaks to the fact that solving major societal challenges – climate change, say, or a global pandemic – is a massive business opportunity that can drive top line growth. If American businesses lead the world in clean power (as noted in our Quarterly JUST Call with American Electric Power’s CEO) or COVID-19 vaccine production, the value creation for both shareholders and stakeholders alike is immense.

But it also speaks to business philosophy, and the belief that investing in workers, supporting local communities, creating good jobs, prioritizing inclusive work cultures – all the things we hear via our public opinion research – can lend companies a sustainable edge versus their global competitors. Our Worker Financial Wellness Initiative, for example, is a growing coalition of businesses, and Chobani joined PayPal as an anchor partner last week. These organizations believe that supporting workers experiencing financial hardship isn’t just the right thing to do, it’s also driving lasting commercial success and strengthening American democracy.

Finally, the question provokes an important discussion about the ways in which governments can promote national competitive advantage by incentivizing businesses to invest in their stakeholders. Getting this right is not easy. Former Best Buy CEO and JUST advisor Hubert Joly talked this week to our editorial director, Rich Feloni, about his new book, “The Heart of Business,” and noted the dangers of overburdening companies with too much bureaucracy. Regarding incoming ESG reporting standards, he said that “the general idea of a broader set of metrics is good, but the danger is to create unnecessary and irrelevant complexity.”

Proponents of the stakeholder model must take an international perspective to see its full potential. As Harvard Business School professor Rebecca Henderson told us, “If the U.S. could combine its agility and ability to innovate with a deep investment in high road business models, we would be unstoppable.”

Be well,

Martin Whittaker

Activision-Blizzard’s CEO is taking a 50% pay cut to his base salary and bonuses after shareholders complained about his pay being too high.

Business Roundtable teams with the U.S. Chamber of Commerce to create a Global Pandemic Response to help India’s escalating coronavirus crisis. Immediately on the agenda? Delivering 1K ventilators and 25K oxygen concentrators.

Goldman Sachs asks employees to return to the office on June 14th, making them one of the first Wall Street firms to push for a return to in-office work.

Citigroup, Vanguard, and several other financial companies are embracing a hybrid work model.

Live Nation’s CEO is under fire for quietly bringing back his salary less than two months after saying in April 2020 he would take no pay to deal with losses due to COVID-19.

Today at 12:15PM ET: Register for Just Brands ‘21 to hear our Senior Director of Research, Kavya Vaghul, sharing insights from our Corporate Racial Equity Tracker.

Tuesday, May 11th at 4:00PM ET: How are business leaders grappling with America’s racial injustice reckoning? What can CEOs do to center racial equity and justice within their companies, communities, and society? Join PolicyLink President and CEO Michael McAfee, Ben & Jerry’s co-founders Ben Cohen and Jerry Greenfield, and former Patagonia CEO Rose Marcario to discuss the courageous business leadership we need today to build an equitable nation for all of us. Register here.

On May 13th, Catalina Caro joins a panel previewing our upcoming Blueprint for Racial Equity 2.0with members of FSG, PolicyLink, Rhino Foods, and Lorraine Wilson discusses the ins-and-outs of designing a racial equity investment portfolio with Natixis. Then on May 17th, Alison Omens joins US SIF and The Aspen Institute for a conversation on leadership and policy opportunities for a more sustainable economy for the next 100 days of the Biden administration.

Our Worker Financial Wellness Initiative partner, PayPal’s CEO Dan Schulman, was profiled in conversation with Chobani CEO Hamdi Ulukaya in Barron’s discussing why Ulukaya was inspired to join the Initiative and assess his employees’ financial health and well-being. We’re biased, but it’s a great read!

The Financial Times looks at whether or not CEOs are living up to their promises after George Floyd’s murder, featuring our Corporate Racial Equity Tracker; GreenBiz also includes a mention of the Tracker in its roundup of “whats on the menu” this proxy season, and Martin was quoted in an Insider feature that polled 614 business decision-makers on rising expectations around ESG, data, and accountability.

Three academic researchers – Rebecca Lester from Stanford Graduate School of Business, Ethan Rouen from Harvard Business School, Braden Williams from University of Texas at Austin – received a shout out from Alan Murray in CEO Daily this week for their new paper showing how companies that have demonstrated a commitment to their workers (measured through JUST Capital’s Workers’ scores), took better care of their employees when times got tough during the first few months of the pandemic. You can read more here and download the study here.

(Financial Health Network)

“It’s really important to set appropriate metrics that are within the control of the business and then make sure that you’re making progress over time. It’s what CEOs do in every other part of their business. Why should, the way they manage their employees and the expense of their employees be any different?”

“You see people in the plant happy, but you don’t know what happens when they go back home. What’s the condition of the home? What’s the condition of the people who live in that house with their children? What’s the condition of retirement thinking? Those conditions really affect how they are in the factory.”

The legal document says explicitly that our duty is to the financial shareholders, but the truth of the matter, now recognized by the Business Roundtable and elsewhere, is that the world has changed. … And people do feel like corporations, because of their size, because of their scale and imports, they have a bigger role to play. It’s also the asset owners – the pension funds and insurance companies. This is our money that we put to work. We want to see better outcomes in society.

The Washington Post chronicles how “the two Kens” – Kenneth Chenault, former head of American Express, and Ken Frazier, head of Merck – created a movement over the last two months to get major corporations to take action on voting rights.

The New York Times reports on two new coalitions of companies – including HP, Microsoft, Unilever, Salesforce, and Patagonia – calling for expanded voting access in Texas, wading into the debate over proposed new restrictions.

Forbes reports that several prominent business leaders are teaming up on a coalition to tackle AAPI hate with a $250 million campaign over the next 5 years.

Reuters reports that the Biden administration blocked a Trump-era rule that would have made it easier to classify gig workers as independent contractors instead of employees, signaling a potential policy shift toward greater worker protections.

Quartz shows why pandemic aid actually led to the biggest jump in middle-class disposable income ever.

Our latest chart of the week looks at new research from S&P Global on the rise of Sustainability-Linked Bonds, and how they are a unique win-win opportunity for companies to show quantifiable progress toward the S in their ESG goals.

Walmart

This week, JUST convened a virtual gathering of current and former corporate leaders to explore, in part, our Worker Financial Wellness Initiative.

While the discussion was under the Chatham House Rule, I can share some of the biggest takeaways from this highly impressive group, which are that CEOs must be courageous enough to take a short-term hit in order to create value for stakeholders in the long term, and that investing in the financial security and overall well-being of workers is perhaps the single most critical investment a company can make right now.

As you can read in my latest Forbes article, Walmart has seen both sides of the stakeholder vs shareholder debate over the last seven days, losing $25 billion off its market cap after a mixed earnings call. What made Wall Street especially upset was CEO Doug McMillon’s announcement of a $14 billion investment in operations – which included raises for 425,000 of its associates, from $13 to $19 per hour, depending on location and market. Costco, which followed suit yesterday by announcing it was lifting its hourly minimum wage to $16 per hour, saw similar short term stock declines.

Since becoming CEO in 2014, McMillon has been laser focused on keeping Walmart competitive with its rivals – notably Amazon, Target, Costco – in a rapidly changing retail landscape. Having the courage to invest in their workforce is a key part of this. When he raised wages for 1.2 million workers in 2016, the stock took a hit then too. It took two days to recover, and six months later was up 23%.

The key point is this: Building value for investors – and for all stakeholders – takes time, but the rewards for shareholders and society at large are much greater. CEOs need our support when they are punished in the short-term for their foresight.

Be well,

Martin

Aetna, UPS, Starbucks, UPS, and Whole Foods showcased as companies that offer health insurance to part-time employees.

150 CEOs, including those of BlackRock, Google, Goldman Sachs, and Intel, signed a letter urging Congress to pass President Biden’s $1.9 trillion coronavirus bill over Republican objections.

Costco will raise its starting wage to $16 an hour, officially paying higher than their competitors at Amazon, Best Buy, or Target.

Glassdoor launches a new product feature that reveals employee provided company ratings and salary reports broken out by specific demographic groups, specifically, salary data is broken out by gender identity and race/ethnicity.

JPMorgan Chase announces new investments as part of its $30 billion commitment to lift up Black and brown communities, including $350 million to support underserved small businesses, a $42.5 million to a “Entrepreneurs of Color Fund,” and new “lounges” serving entrepreneurs.

Nielsen announces that they will begin tracking diversity and inclusion on TV.

Walmart backed a McKinsey study – Race in the Workplace: The Black Experience – examining racial inequity in the private sector, particularly in higher-wage, higher-growth industries.

Throughout the coronavirus pandemic, companies faced new challenges in maintaining employee well-being. We teamed up with AARP to create a set of guides focused on three critical issues – paid sick leave, dependent care, and work from home – to help explain the current state of play, best practices, as well as benefits to employers and employees for implementing expanded programs. We hope they are a helpful resource.

A Corporate Guide to Dependent Care: By creating sustainable dependent care options for both eldercare and childcare, companies can greatly improve quality of life for their employees and their families and see significant savings and reduced turnover.

A Corporate Guide to Paid Sick Leave: By implementing paid sick leave policies, companies are not only protecting their workers’ health and financial security, but also the health of customers, communities, and their supply chain.

A Corporate Guide to Working From Home: By creating greater flexibility and better work-life balance, companies can reduce costs and turnover, and increase productivity and happiness.

JUST’s Yusuf George highlights nine Black women who are championing stakeholder capitalism across America’s largest companies, including Rosalind Brewer and Thasunda Brown Duckett, who will be the only two Black women CEOs of Fortune 500 companies.

The Reimagining Capitalism newsletter on LinkedIn featured a sit down with Martin exploring ideas for designing a more fair, inclusive, and sustainable capitalism. Explore other great interviews here.

Jennifer Tescher of the Financial Health Network invited JUST Board Member and National Urban League president Marc Morial onto her “Emerge Everywhere” podcast to discuss Economic Justice for All.

JUST Board member Arianna Huffington penned a byline in Thrive talking about new S.E.C. guidelines on human capital reporting, demonstrating a growing recognition of employee well-being as a key driver of business performance.

“Addressing stark disparities in income and wealth doesn’t just benefit Black families and marginalized populations. It benefits our neighborhoods and our entire economy. It is our collective responsibility to address this challenge and break down structural barriers to opportunity.”

“Thinking about employees shouldn’t be a function of human resources – it’s a competitive differentiator, and it’s needed now more than ever. …By advocating for internal safety measures, effective policy, and racial equity, companies can put purpose-driven leadership into practice to protect their workers and fuel an inclusive recovery.”

“I want to note this isn’t altruism. At Costco we know that paying employees good wages … makes sense for our business and constitutes a significant competitive advantage for us. It helps us in the long run by minimizing turnover and maximizing employee productivity.”

A Financial Times opinion piece explains why businesses should not be afraid of the calls to raise the minimum wage: “Almost all Americans, whether they live in Texas or California, admit that it is impossible to live on $7.25 an hour.”

In their State of Working America 2020 wages report the Economic Policy Institute shows that wages grew historically fast in the last year because the bottom fell out of the low-wage labor market: “Wages grew largely because more than 80% of the 9.6 million net jobs lost in 2020 were jobs held by wage earners in the bottom 25% of the wage distribution. The exit of 7.9 million low-wage workers from the workforce, coupled with the addition of 1.5 million jobs in the top half of the wage distribution, skewed average wages upward.”

The challenges of child care is getting the attention it deserves with an in-depth feature in The Lily explaining that a full economic recovery will only be possible if we invest heavily in our nation’s patchwork dependent care systems. Also a new report from the think tank Third Wayexplains that the costs of child care centers have gone up nearly 50% since the onset of the pandemic and that lack of child care is now the third-most cited reason for not working, behind layoffs and furloughs. CBS reports that the Marshall Plan for Moms is picking up steam in Washington.

Meanwhile, The New York Times believes that, no matter what, an economic boom lies at the end of the pandemic.

The Stagwell Group hosted a webinar featuring some of the most interesting findings from The Harris Poll’s survey work on CEO reputation. One of the most interesting insights? Ethical standards are the highest valued quality in a CEO.

This week, we look at Morningstar’s most recent analysis from Jackie Cook, diving into the C-suite Gender Pay Gap analysis that explores pay data of corporations’ named executive officers (NEOs).

(Redpixel/Adobe Images)

After yet another election cycle where the pollsters seemed off the mark, many Americans were left wondering whether they can trust not only political polls, but polling in general. As Managing Director of Survey Research at Just Capital, I take this concern very seriously. Research is at the heart of our work, but it differs in both methodology and substance from political polling. Just’s survey research, fielded in partnership with The Harris Poll, strives to present the most accurate assessment of what the public expects from America’s largest companies and their business leaders. I talk about the means by which we achieve those insights in more detail below.

In 2020, presidential polls and forecasts showed that Joe Biden would not only beat Donald Trump, but by a wide margin, and that Democrats had a better-than-average chance of picking up enough seats to change the balance of power in the Senate. Even though the outcome of the presidential election was eventually close to what was projected, there were key misses in predicting which states would flip (like Florida and Texas) as well as in down ballot races (such as Maine’s senate seat).

Rarely have political polls forecasted presidential elections by a pinpoint margin; in fact, the margin of error has been remarkably consistent throughout the modern era of polling. Polling around the 2016 election is largely remembered as a failure, but as Nate Silver wrote in a 2018 article in FiveThirtyEight, “polls of the November 2016 presidential election were about as accurate as polls of presidential elections have been on average since 1972.”

Now, in an already tumultuous year, the perceived mis-projections of 2020 have been compounded by those of 2016, leading to a new narrative that “the polls cannot be trusted.” This means that the polling profession in general and my work specifically will surely come under increased scrutiny. But although I cannot control the media narrative about the industry at large, I can offer increased insight into the work we do at Just Capital.

I am responsible for managing the design and execution of all stages of the research that drives forth our mission. A critical piece of our work involves capturing the sentiments, preferences, and values of the American people regarding just corporate behavior to help align their priorities with the priorities of corporate America.

All of our work is informed by public opinion research, which we refer to as “polling” as a form of shorthand. While public opinion research and political polling are of the same stripe, they ultimately are very different animals. Specifically, the research that Just Capital undertakes does not predict outcomes (e.g. the winner of a political race), but is a means of understanding the American public’s opinion about the issues that matter most to them regarding business behavior. In this sense, it is more akin to consumer market research than political polling.

While political polling and our research both take a snapshot of the opinions of a random sample of Americans at a moment in time, the approach we take with our Annual Survey is in actuality a form of consumer choice modeling, which requires respondents to discriminate between items and make tradeoffs between most and least important among a subset, yielding the relative priority of each item. The methodology of our Annual Survey is arguably more robust than political polling in the following ways:

In a nutshell, Just’s public opinion research differs from political polling because of who we survey and the methodologies we use.

Now that we’re a couple weeks removed from Election Day (or Week, really), the assessment from many reputable sources is that in actuality the polls were pretty accurate. However, elections are habitually high stakes, with the public demanding a level of precision that is virtually impossible to realize. Nate Silver of FiveThirtyEight cautioned that we all should modify our expectations of what polls do because, “if you want certainty about election outcomes, polls aren’t going to give you that.” What transpired in both 2020 and 2016 is that the polls couldn’t deliver an adequate level of accuracy to satisfy the court of public opinion. So what went wrong?

Fundamentally, an election poll must be representative of the people who actually vote. This year saw historic levels of voter turnout, both in-person and via absentee ballots. Past voting habits and likelihood to vote are key questions from which polling projections are estimated, yet both metrics are self-reported and thus subject to error. One key challenge of 2020 – much the same as 2016 – is that most polls did not survey enough Trump supporters to be representative of that group, resulting in an overestimation of Biden’s lead at both the national and state level.

Why didn’t pollsters find enough Trump supporters? The case of the “Shy Trump Voter” (the idea that Trump voters would rather lie to a polling outlet perceived as liberal) is a popular narrative, but is far less likely to drive sampling error than the increasingly pervasive problem of non-response. Non-responders are those who either cannot or will not respond to surveys, and it is unfortunately a growing problem for the survey community at large. The profile of non-responders generally differs in a meaningful way from that of responders, leaving pollsters with a higher level of sampling error. In the case of the 2020 election, non-responders were significantly more likely to be Trump voters. As the New York Times’ Nate Cohn noted, there is more evidence, then, that Trump supporters suspicious of an outlet they think is ideologically opposed to them would rather not participate than lie.

One way to ensure the representativeness of underrepresented groups is to use probability-derived samples, which simply means any American has an equal probability of being chosen as a respondent as any other American. This equal probability applies to folks in sparsely-populated areas, or those without internet access, or those who do not generally respond to surveys. But data reliability is costly, and as such many political pollsters instead rely on upweighting certain demographics to overcome challenges in not reaching enough of a population.

For the past five years, Just Capital has drawn the sample for its Annual Weighting Survey from the National Opinion Research Center (NORC) at the University of Chicago, which uses probability sampling methods to achieve a representative sample frame projectable to 97% of U.S. households. Representativeness of the sample is based on two factors: oversampling of traditionally underrepresented populations, and follow-up efforts to ensure that traditionally non-responsive households are included. As such, we capture perspectives across generational and ideological divides, varying income and education levels, race, gender, and more, giving us the utmost confidence that our public opinion research is truly representative of all Americans.

Though many political polls vary in length, complexity and construction, most political polling is derived from the methodology standardized by Gallup, which matches the country’s demographic mix to voter intent to make predictions. This methodology may have worked well in the past, but in recent years it has resulted in little more than yielding a strong signal toward who has the better chance of winning versus a definitive call on who absolutely will win.

A central tenet of research holds that the more information you have about a target audience, the more accurate your projections. Market researchers are really good at sizing an audience they want to sell to, and a key part of that involves building attitudinal and behavioral questions into their modeling. Conversely, in most political polling, scrutiny of voters’ motivation is pretty deficient. In other words, a lot of polls miss the nuance about how and why people behave the way they do. In The New York Times postmortem, “a fundamental mismeasurement of the attitudes of a large demographic group,” is one key reason contributing to the errors in the 2020 polls.

Take for example the “Latino vote.” Most pollsters expected to see the same patterns of voting behavior throughout this demographic group. Yet one of the biggest surprises on election night was the GOP’s performance in Florida, particularly among Cuban Americans in Miami-Dade County. Here we see in stark relief the dangers of modeling outcomes based solely on ethnicity: The misconception that Latinos are a homogeneous population resulted in a miscall for Florida. If pollsters had bothered to look closer at Latino subgroups, they would have learned that the reasons that drove Puerto Ricans from New York to vote for Biden (e.g. social justice issues, the possibility of future Puerto Rican statehood – are very different from the reasons that turned out Cuban Americans to vote for Trump ( e.g. the perpetual hangover of life under Castro’s Communist regime drove voters away from Biden’s agenda, branded as “socialist” by the right).

Writing in the New York Times, David Shor agreed that making too many assumptions is akin to “garbage in, garbage out,” saying, “Demographic factors are not enough to predict partisanship anymore.” If the polling profession wants to right its reputation by improving its level of accuracy, it’s time that pollsters take a page out of the market researcher’s playbook and broaden their mix of methodologies to include more qualitative and attitudinal research.

The President of Pew Research Center, Michael Dimock, recently wrote a blog outlining how the industry can and should move forward. “Good pre-election polls try to get inside people’s heads,” he wrote. “They attempt to understand the reasoning behind Americans’ values, beliefs and concerns. They explore…which factors are motivating them to vote for a particular candidate, or whether to vote at all.”

One recent discussion thread among members of The American Association of Public Opinion Research (AAPOR) put it even more bluntly: “Where was the qualitative research to be added to the quantitative polling of voters in the 2020 campaign?”

Just’s mission is supported by a robust and rigorous research program that polls Americans on the issues they believe U.S. companies should prioritize in order to embrace just business behavior. Though the research that we do is very different from political polling, the fundamental goal is the same, to represent the voice of the public. We do this by capturing the sentiments, preferences, and values of the American people through qualitative discussions coupled with quantitative surveys. This mix of methodologies allows us to mine insights that help us help companies build a more just marketplace and become a positive force for change.

We continuously strive for diversity in our methodology, and to that end, in 2021 we will be forging a path forward by pairing traditional polling with broader insights gathered from other methodologies, such as additional qualitative work, sentiment analysis, natural language processing, and social media listening. Taken together, they can, according to Emilio Ferrara of the University of Southern California Information Sciences Institute, “give us a window into enthusiasm among populations that polls are missing.” In addition, Just will be adding a layer of oversight to our research by forming an independent Polling Committee composed of industry leaders and academics.

I am supremely confident of the quality of our public opinion research, but now more than ever we approach that work with humility as we strive to make our public opinion research even more robust, allowing us to have a deeper and richer insight into the thoughts and opinions of the American public.

For a deeper dive on the 2020 election and polling more broadly, I recommend the following sources:

Photo by Adam Schultz

When last week’s newsletter went out, we were a day away from the AP calling the election for Joe Biden. It’s worth noting that Biden will be the first president to embrace “stakeholder capitalism” by name. As I told Business Insider for a Q&A on the subject, the president-elect will find a private sector poised to step up, an investment community increasingly on board, and an American public substantially united behind the idea. Importantly, the Business Roundtable and other business groups have already signaled their intent to work with a Biden administration, and sent a clear message. “Our country faces great challenges in the months ahead to defeat the pandemic and rebuild our economy,” the BRT wrote. “We will meet them only by working together.”

Critical to doing this is rethinking how business and government might work together. The traditional model holds that public and private sectors are locked in a constant struggle, with the pendulum swinging between regulation and taxation on the one side, and free enterprise and profits on the other. For the good of the country, this has to change.

What’s needed now is a new vision for harnessing the power of the private sector to tackle society’s most intractable problems. That vision is stakeholder capitalism. To be clear, this is not about partisan politics. And it’s not about socialism, wealth redistribution, or regulatory reform. It’s about incentivising companies to create meaningful, lasting value for all their stakeholders and in doing so, growing the pie for everyone. One thing that is crystal clear from our research during 2020 is that whereas the United States is still very much divided politically, when it comes to what we want from the economy we are on the same page: good jobs, fair pay, a liveable wage, the right to be treated equitably and with respect, strong communities, a clean environment, and a path to upwards economic mobility. These are the hallmarks of a just economy, and in that, the public, business and government can be united.

The Biden Administration has a once-in-a-generation opportunity to chart a new, better, more inclusive course for capitalism. Brad Smith, president of Microsoft, three-time America’s Most JUST Company, phrased it perfectly in his open letter to the president-elect; “we believe that Americans share more common ground than many pundits acknowledge,” noting, “there is an opportunity to separate policies from politics so we can make a real difference in people’s lives.”

The American people agree.

Be well,

Martin Whittaker

Amazon pledges to double its number of Black leaders this year and ban non-inclusive language from documents.

Estee Lauder announces that it has achieved net-zero emissions ahead of schedule, sourcing 100% renewable energy globally for its direct operations.

VF Corp acquires the clothing brand Supreme for $2.1 billion.

Twitter announces a $100 million investment in community development financial institutions (CDFIs), in a new initiative aimed at combating “racial injustice and persistent poverty.”

Whole Foods’ CEO defends its wage transparency policy, explaining how it provides employees with a path to move up the ladder by working harder.

Join Martin Whittaker, Byron Loflin, and David Motley – President & CEO, MCAPS LLC, and Founder of the African American Directors Forum-Pittsburgh – for an engaging conversation around racial diversity in the boardroom, the rise of stakeholder capitalism in improving diversity and inclusion, and more. Register here to join the conversation.

Our own Steffen Bixby will be speaking at Pittsburgh CFA Society along with members from Goldman Sachs on ESG Investing Strategies. Sign up to join here.

Martin spoke to Marguerite Ward at Business Insider on what a Biden presidency might mean for stakeholder capitalism, ESG regulations, and more.

Last week, NYSE and JUST Capital joined forces for a virtual event exploring how companies and investors can lead in building a more just and inclusive economy that works for all Americans. Watch the replay here.

At the Forbes JUST 100 Virtual Summit we discussed why worker financial wellness must be a priority for corporate leaders, now more than ever, in conversation with PayPal CEO Dan Schulman, JUST Capital Co-founder & Chairman Paul Tudor Jones, and Chief Strategy Officer Alison Omens. View the talk and key takeaways here.

Quartz is going independent once again. Their mission? Make business better.

Yahoo Finance reports that in a stark shift from just a few years ago, companies are three times more willing to hire remote workers.

Our latest ESG Chart of the Week comes from Bloomberg Green. As companies increasingly face the prospect of needing to incorporate carbon emissions and emission reductions when doing internal cost-benefit analysis for new projects, Bloomberg takes a look how they’re dealing with decarbonization targets.

(Business Roundtable)

On Tuesday, a study from the new Test of Corporate Purpose (TCP) initiative shone a welcome light on how the largest American and European companies responded earlier this year to the COVID-19 pandemic and mass protests against racial injustice. The report underscored the importance of shifting to a stakeholder-led approach and holding companies to account for their commitments. After six years of polling, we know this is precisely what the American people want.

Yet the report also provides a vivid illustration of just how hard it is to definitively evaluate stakeholder capitalism as a movement. Declarative statements like the headline the New York Times used for writing it up – “Stakeholder Capitalism Gets a Report Card. It’s Not Good” – are not only premature, they deflect away from the real task of determining what exactly stakeholder capitalism is and how we can better measure it.

Take as an example one of the key conclusions of the TCP analysis. As it was framed in the Times piece: “‘Since the pandemic’s inception,’ the study concludes, the Business Roundtable statement ‘has failed to deliver fundamental shifts in corporate purpose in a moment of grave crisis when enlightened purpose should be paramount.'”

The story is much more nuanced than that.

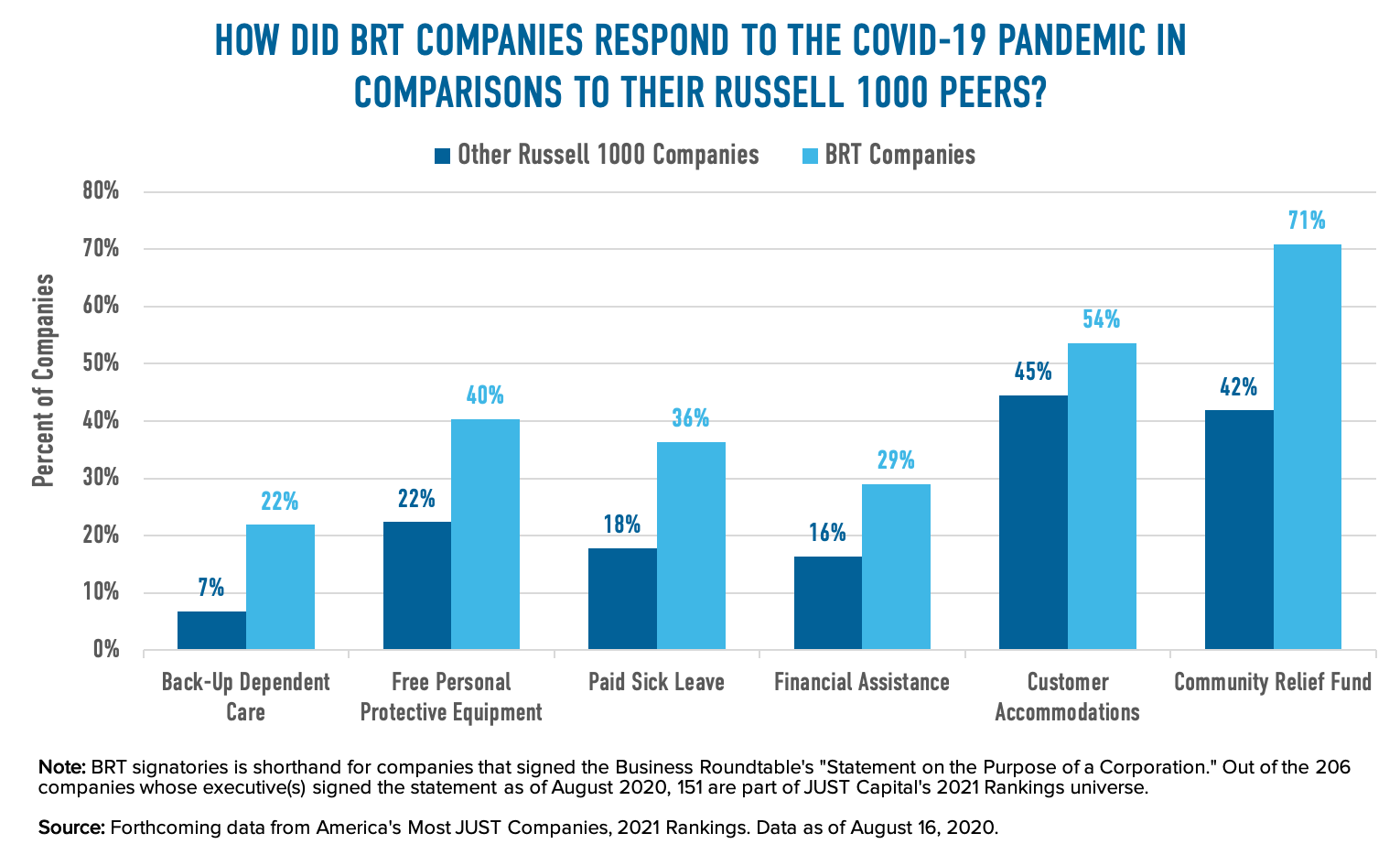

On the one year anniversary of the BRT purpose statement this past August, we released new polling in partnership with The Harris Poll and ran an analysis of several key COVID-19 and racial equity data points to test how BRT companies were doing on serving their stakeholders against their Russell 1000 peers. (Stay tuned, as we’ll be releasing additional analysis after our annual Rankings release on October 14.)

Overall, we found that BRT companies actually out-performed their peers, even if they didn’t fully match the expectations of the public. Specifically:

We also looked at how the BRT companies responded to four critical issues regarding advancing racial equity in the workplace. Once again, their performance was, on a relative basis, superior to peers:

Different approaches to measurement naturally produce different results and help drive progress overall. For example, the sentiment analysis on which TCP’s study partly depends – supplied by TruValue Labs, a pioneer in the ESG space – can be an important piece of the overall picture in our view and is a welcome innovation in an ESG data industry not renowned for creativity.

Our approach takes a different tack, and looks at what companies are disclosing as well as myriad other sources of public information on their relative performance. It’s a painstaking process. This year we’re tracking 928 companies across 19 issues, five stakeholders, and 336 unique data points, and we have been closely tracking corporate responses to COVID-19 and racial equity issues throughout the spring and summer. We estimate our team has spent over 15,000 hours gathering and analyzing granular data; combing through proxy statements, CSR reports, internal communications, and press releases; reaching out to and engaging corporations; and factoring in publicly-reported controversies.

Our COVID-specific analysis, recorded in the JUST COVID-19 Corporate Response Tracker, covers over 80 types of corporate action including paid sick leave policies (with details about policy type, eligibility, weeks of leave, and barriers to access); health and safety precautions for workers and customers, including provision of free PPE to workers; and whether companies had expanded emergency grants for workers, offered bonuses, offered temporary or permanent wage increases (and how much), or increased the pay rate for overtime work, among other details about the financial assistance provided.

The point is that measuring corporate stakeholder performance is complicated, and without standardized and disclosed metrics, along with a common understanding of what precisely is being measured and why it’s being measured, real progress will remain elusive.

Operating from a common framework is one way we get there. We celebrate the World Economic Forum’s International Business Council report on ESG metrics, also released Tuesday, as an important milestone on the journey towards shared measurement standards.

And we vow to continue our own efforts to bring greater overall transparency and accountability to the corporate stakeholder performance world in order to put stakeholder capitalism itself onto a practical, solid foundation.