Each year, we survey the American public to learn their views on business today, and we’ve learned that Americans consistently agree – year after year – that the top priority for companies should be their workers. And the public doesn’t necessarily distinguish between different types of workers – whether full-time, part-time, or contracted – showing that temporary, contract, and vendor (TVC) workers should be prioritized alongside a company’s permanent workforce.

Since 2018, JUST Capital has been working to better understand how companies think about their TVC workforces – and we’ve found that corporate leaders continue to grapple with key questions around these workers. Concretely: are TVC workforces a risk to be managed, or a potential asset that hasn’t been properly explored?

Over the last year, the impacts of COVID-19 have accelerated these questions – with companies asked to carefully consider how to support their contract workforces through the pandemic, and with the world of work writ-large on the cusp of transformation, as companies grapple with whether and how to reopen their workplaces and what a return to “normal” might look like for their employees. With TVC workers an increasingly urgent topic for corporate America, we recently sat down with Teresa Huston, Vice President and Deputy General Counsel at Microsoft, and Tauseef Rahman, Partner at Mercer, to explore their work on these issues.

At the start of the pandemic, #1 Most JUST company Microsoft committed to continue paying its contractor workers – many of whom work on-site at the company’s campus in Seattle – and the company continues to compensate these employees today. Huston explained Microsoft’s journey to this decision, which began long before the pandemic with a path that included a seminal lawsuit and now has led to Microsoft extending key benefits to its temporary employees. “We learned some pretty hard lessons from that case,” Huston shared – and in the years since, Microsoft has become a pioneer on these issues, requiring its vendors to offer paid sick leave and paid parental leave to their workers. With these foundations in place, Microsoft’s choice to continue paying its TVC workforce was a natural next step, and served once more as a model for how corporate leadership can and should support these employees.

Mercer – a consulting firm whose mission serves, in part, to help companies redefine the world of work – often explores the issues of TVC workforces in conversation with its clients. In March of 2020, Mercer learned that about ⅔ of companies say they employ contractors – but also found that the majority did not provide compensation during the pandemic. Rahman explained that the nature of contract work holds significant risk for TVC workers, particularly during more challenging times, but emphasized that this moment represents a significant opportunity to ask “Are there different ways to work for a company?”

Key takeaways are emerging from our conversations with companies – including Microsoft and Mercer – about how corporate leaders should consider their TVC workforces, as we continue to talk about building a more resilient economy in the future:

In recent years, more and more contract workers have become core to companies’ operations – sitting alongside their permanent counterparts as colleagues and taking part in work that is central to their company’s operation and mission. With Americans expecting companies to prioritize their workers, corporate leaders must consider how they support not just their employees, but the contract workers who share space with them and contribute considerably to their collaborative work. Huston emphasized that, while the unique legal and contractual considerations of contract workers can’t be ignored, corporate America needs to move away from the mindset that contractors are “a risk to be managed” and toward a more integrated understanding of how TVC workers contribute to the resiliency of their business, shape the experiences of the permanent workforce, and advance the company’s mission through their efforts.

Before we can truly consider what might need to change for America’s contract workforce, we need to understand the current state of play for these workers. Human capital disclosure – particularly around demographic issues – is becoming increasingly important across corporate America, but TVC workforces present unique challenges when it comes to disclosure and transparency. With many contract workers employed through vendors, Huston emphasized that there are different legal considerations at play – in regards to both the demographics of these workers and even what kinds of jobs they hold – when asking companies to share details on their contract workforce. Furthermore, Rahman shared that contract hiring and human capital issues might not even be centralized with HR departments, making it difficult to collect information about these workers and factor them into strategic workforce planning. In the coming years, a core question for corporate America must be around how we build a clear and consistent portrait of our nation’s – and each company’s – contract workers – so that we might better understand what is working and what is not.

Over the years, our research has shown that treating workers well not only benefits a company’s employees but its bottom line. Understanding, again, that contract and permanent employees are part of the same workforce, the unique challenges faced by TVC workers can negatively impact their own productivity as well as the productivity of their permanent colleagues – and the challenges of retention and retraining contract workers can significantly slow or hamper a company’s operations. Huston emphasized that, for Microsoft, “Making decisions to be responsible and aware has been good for our business,” a guiding principle that led them to set specific contract standards for their TVC workers – like paid sick leave and parental leave – that allow these employees to be more present and effective members of Microsoft’s overall workforce and to contribute more significantly to the company’s growth.

As we look ahead to the reopening of businesses across corporate America, the question of how contract workers are supported today can profoundly impact our eventual return to work. Most tangibly, there are key questions of occupational health and safety – if paid sick leave is not available to contract workers, the risks of outbreak are potentially greater, and the ways that contract and permanent employees share space can impact critical health concerns. But there are also important questions about operational resiliency – if an entire contract workforce has been laid off, corporate leaders face significant challenges to resuming normal operations and scaling back up, needing to rehire and retrain workers across many areas of their business. Finally, it’s critical for companies to recognize how decisions around their contract workforces can have tremendous impact on their communities. Huston shared that, for Microsoft, a major way that the company contributes to its community is by providing jobs to the people who live there. “We really are responsible for how our region emerges from this catastrophic event,” she emphasized – suggesting that support for contract workers shapes not only the future of our nation’s businesses, but the future of our nation’s communities.

Embedded within this question of how we rebuild following the pandemic is the consideration of what the future of work writ-large might look like. Rahman hypothesized that our “full-time-or-bust” mentality might become a thing of the past, as more employees core to companies’ operations are employed on a contract basis and we begin to more deeply question whether there are different ways to work for a company. And questions of flexibility and types of employment are relevant not just to lower-wage, lower-skill work, but must be central in how we think about all our nation’s workers. This moment represents an opportunity for companies to consider, coming out of the pandemic, what groundwork they might lay now to ensure that their full supply chain is resilient and connected to the operations and purpose of the broader company.

Corporate leaders are increasingly seen as societal leaders, responsible for what’s happening not only within their own organizations but within their communities and the world of work writ-large. It’s clear, and becoming clearer, that these issues are not limited to the on-demand economy or to lower-skilled workers, but to TVC employees across industries and the wage ladder who have become deeply integrated in their company’s core operations. In our ongoing conversations with C-suite leaders – focusing on issues like worker financial well-being and racial equity – we will continue to apply this lens of consideration, asking how a company’s TVC workforce must shape strategic decisions around these issues, as well as the future of work overall. There’s a real question about mindset-shift on this issue, where leaders must begin to ask and understand their contract workers. In the meantime, we will continue to contend with the fragmentation of America’s workforce, and the implications that fragmentation has for our nation’s businesses, the communities in which they operate, and the world of work overall.

Explore more of JUST Capital’s work on the TVC workforce here, and watch the full conversation with Microsoft and Mercer below:

COVID-19 has transformed our cities, our jobs, and our economy. It’s also fundamentally transforming businesses – from the urgent need to address operational and financial challenges to turning broadly pronounced statements of stakeholder purpose to precise examples about how companies are treating their stakeholders in a crisis.

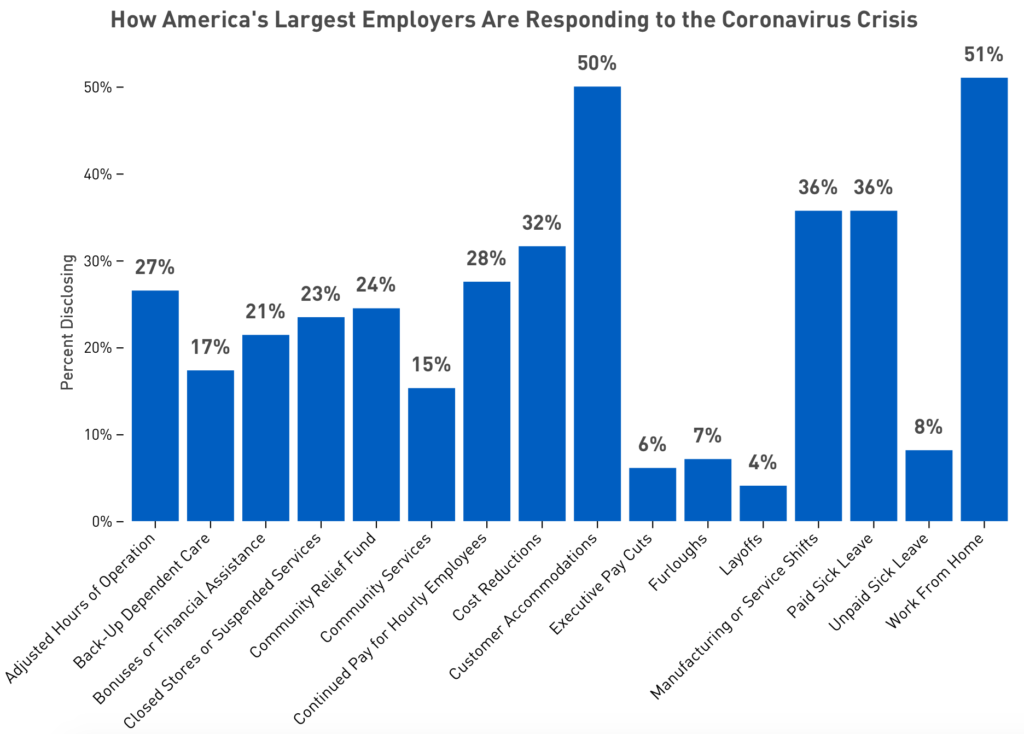

We’ve been tracking the actions taken by companies in response to coronavirus, and as of April 1st, we’ve tracked that 29% of the 100 largest U.S. employers have announced some kind of bonus, grant, or financial assistance to help curb income volatility and compensate people for their work in this time, including Target and AT&T.

Those payments are increasingly being referred to as hazard pay because workers in grocery stores and pharmacies are literally on the frontline of this pandemic, sacrificing their health and safety for companies to stay open and for consumers to continue to have access to essentials like food, internet, and basic services.

Paid sick leave is another critical benefit for workers. According to our assessment, 38% of the largest employers have announced implementing or extending a paid sick leave policy in response to COVID. Many of these policies are reliant on an employee having a confirmed case of COVID, which in a limited testing environment, is a high bar.

We’re also seeing the relationship among businesses and their stakeholders change. We’ve seen employee activism explode in recent days, from strikes at Instacart and Whole Foods, to reports from worker groups hearing from workers in droves. We’re seeing communities and governments ask companies to step up in new, profound ways around making medical equipment and other necessities not experienced since wartime.

It may be too early to ask but here’s what’s on my mind: What comes next? This crisis has shown how vulnerable many Americans are, and that many companies either didn’t or don’t have policies in place to ensure people’s well-being and financial security. A number of companies have really stepped up to the plate – clearly considering their workers’ full, lived experiences in enacting policies that range from wage increases and bonuses to paid sick leave and dependent care to more flexibility on working hours.

Whenever this ends – spring, summer, or later – companies will face a choice: Do they continue to compensate their workers at the level they have been through this crisis, or do they withdraw those wages and benefits because the immediate crisis is over?

JUST Capital has done extensive polling of the American people, and before the pandemic, 80% of people thought companies were not sharing enough in their successes with their workforce.

Workers on the frontline – nurses, doctors, and also grocery, pharmacy, and delivery workers –- have recently been celebrated and championed, but will they all see wage cuts? Are we really going to roll back paid sick leave for all the workers that just received it for the first time? Or is this the moment that we can recognize that the way out of this crisis in a sustainable way is to grow the pie for more people?

This is a moment for companies at the forefront of stakeholder capitalism – that have been talking about their commitment to their stakeholders – to actually show that commitment, keeping benefits and higher wages in place. This is a moment where we don’t aspire to return to normal. But rather we build something better, and create a stronger, more interconnected system that supports all stakeholders over the long term. Where companies and workers alike are better equipped to weather future storms, and where companies become more resilient against future shocks and disruptions like this one.

This article was originally published at Forbes.com.

The world is gripped by fear. The market is plunging. Governments are locking down cities. Many of us are refreshing news sites and Twitter to understand the latest update. Of course, I’m talking about the coronavirus, or COVID-19, an international pandemic that’s leaving everyone anxious.

There’s been much (welcome!) talk about stakeholder capitalism, purpose, and a commitment to workers in the last year, from the Business Roundtable’s new statement of purpose to its presence as a main topic in Davos. The reality is that this is the moment for companies to put stakeholder capitalism into practice – to demonstrate their commitment to an American public that is increasingly skeptical about promises (according to our polling, less than half of Americans currently trust large companies). Every company – from the 181 that signed the Business Roundtable’s pledge to those espousing purpose and a commitment to workers and communities – should be acting now.

What should companies be doing?

First, paid sick leave. Every worker, regardless of classification, needs access to paid sick leave. And with too few tests available and concerns about hospital overuse, it can’t only be available when a worker has a proven case of COVID-19. We’re seeing announcements from companies like Walmart and Darden Restaurants on new sick leave policies. Fundamentally in this environment, workers need 14 days of leave. Companies should also press Congress to implement sick leave universally. This will level the playing field for those companies that are committed to doing the right thing for their workers and communities.

Second, we’re seeing many tech and white collar companies encourage or require employees to work from home. Those companies must also be thinking about their contractors, vendors, and suppliers. We’ve seen companies like Microsoft and Alphabet pledge to cover lost wages of hourly workers at their headquarters. Every company should include this as part of their calculation over the coming days and weeks. Stakeholder-run companies connect the interests of their workers to their suppliers and communities, and this is a critical example of that.

And third: Companies need to know the financial security of their workforce and ask if their workers are making ends meet each month. JUST Capital can help with conducting a financial stress test. This is the moment where recommendations like storing up a month’s worth of food is simply not possible for workers in financial distress. We know that 40% of Americans can’t afford a $400 emergency and according to our initial estimates, 10.4 million people (of the 20 million overall) who work at Russell 1000 companies do not make enough to support a family of three, even with a spouse working part time. It goes without saying that a pandemic is one of those emergencies – necessitating that people obtain additional medication, food, and healthcare.

More fundamentally, as a recession feels more likely, companies (and investors) must recognize that the last 10+ years of growth, buybacks, and tax cuts can and must cover the costs of keeping jobs and workers in those jobs. There is some evidence that an investment in workers, rather than layoffs and cost-cutting measures, along with operational efficiencies and agility can support the long-term resilience of companies. Studies have also shown that stakeholder-driven small businesses, post-2008, were more likely to rebound due to their stakeholder approach in a downturn.

This is a once-in-a-generation moment. Business leaders should be acting quickly to be sure they’ve defined their vision for and commitment to their workers, communities, suppliers, and long-term interest of investors. This is the social license to operate; this is stakeholder capitalism.

Last week, JUST Capital hosted a briefing call on the growing importance of quality jobs in America, and the ways that investments in frontline jobs can lead to better business outcomes. We dug into this topic in conversation with Michael Mussallem, Chairman and CEO of Edwards Lifesciences – a JUST 100 company that prioritizes the pay, benefits, and opportunities of its employees – and Sarah Kalloch, Executive Director of the the Good Jobs Institute, which was co-founded by Professor Zeynep Ton of MIT Sloan and focuses on shifting business performance by focusing on creating good jobs in low-wage industries (particularly retail).

With worker pay and well-being a core priority for the American public when it comes to just business, JUST Capital is committed to continuing to surface the business and investor case for good jobs. Our own analysis shows that companies who treat their workers well consistently outperform their peers at the market level.

Check out four key takeaways for corporate leaders from the call:

For many companies, employee engagement and dedication to its mission are top priorities. The Good Jobs Institute outlines a hierarchy of workers’ needs that shows that, if companies seek to meet these goals, they must first start by creating good jobs.

A medical technology company based in California, Edwards Lifesciences has 14,000 employees globally and a notable manufacturing workforce in the U.S. Mussallem, in describing the company’s culture, emphasized that its company-wide commitment to patient outcomes – and the connection it fosters between employees and the patients they serve – is vital to Edwards’ success.

Ranked 20th overall on worker issues in our 2020 Rankings of America’s Most JUST Companies, Edwards is first in its industry when it comes to paying workers a living wage and top in class for providing good benefits. Given these achievements, it’s not surprising that Edwards’ employees report feeling a strong sense of commitment to patient health and outcomes, and have higher retention rates than employees at other companies in their industry.

Too often businesses view their human capital as a cost to the company, but a core tenet of the Good Jobs Strategy is around reversing this view, which Kalloch explained can trigger a vicious cycle that harms business outcomes. Beginning with low investments in people, this cycle often starts with operational problems, which lead to low sales and profits as a result. From there, companies might look to reduce expenses, and too often cut costs from their workforce, further reducing investment in their people. The cycle repeats. Kalloch encouraged companies to turn this cycle on its head – suggesting that when corporate leaders view their workforces as an investment from the get-go, they improve rather than hinder business operations and outcomes.

After companies break this cycle and invest more meaningfully in their workforce, they should create an operating system that fosters and maximizes the talents of their workers. Kalloch explained the Good Jobs approach to doing so – a three step process: First, focus on the work employees need to do to meet customers’ needs and simplify processes. When workers are juggling unrelated tasks, stretched thin, or spending too much of their time on non-customer activities, they are less effective and productive on the job. Beginning with this area of work – and simplifying employees’ day-to-day – helps workers become more effective in their interactions with customers, in turn supporting the bottom line. Second, standardize systems and empower workers. By creating a clear line of communication between frontline workers and corporate management, companies can more quickly receive feedback that impacts business decisions. Finally, develop systems for cross-training employees. Training employees on a handful of jobs that are more focused in scope will not only help build a more engaged workforce but also better position stores to respond to variability or unexpected workforce needs. Combined, these operational changes will improve worker productivity and customer satisfaction.

This is the bottom line of the Good Jobs Strategy. Analysis of companies that have implemented the strategies described above – including Walmart and Quest Diagnostics – shows that when these businesses broke the cycle of viewing people as costs and started implementing new practices that maximize the potential and talent of workers, they observed significant business improvements. At Walmart, for example, turnover declined by more than 10% over the last five years, and at Quest Diagnostics, it decreased by 35%. Over the same period, store sales were up at Walmart and Quest Diagnostics saw a $1.3 million annualized run-rate savings. In short, when companies start by investing in workers, they are able to more easily achieve their core mission, and see measurable returns on their investments.

Check out the full conversation on quality jobs here:

For more information on the Good Jobs Institute, and our work in collaboration to build the case for quality jobs, read more here. If you’re interested in speaking further about this research, please contact our corporate engagement team at corpengage@justcapital.com.

For centuries, businesses and their workers have been the engine of economic growth in the United States, broadly sharing in the prosperity they created together.

Today, that is the exception to the rule.

Despite rising productivity and profits, many workers have been left behind. 40% of Americans can’t afford to cover an unexpected $400 expense, 6.9 million are among the “working poor,” and 1.7 million workers are making at or below the federal minimum wage of $7.25.

It’s clear the system that has consistently rewarded shareholders over all other stakeholders is broken. We need a new model that builds prosperity and financial security from the factory floor to the trading floor, that serves all stakeholders of our economy, and supports a fairer, more just capitalism in America.

The solution is stakeholder capitalism, where we expand our definition of business success. We must make sure that we’re creating value for all stakeholders – employees, customers, communities, the environment, and shareholders – rather than simply focusing on short term profit maximization. At $19 trillion, the private sector is 4x the size of government and 40x the size of private philanthropy. There have been many promising signs on movement here, from the Business Roundtable’s statement to individual corporate actions. Now, 2020 is the year to shift aspirations into action, and put the promise of stakeholder capitalism into practice.

As CEOs and boards are asking what it means to deliver on stakeholder capitalism, we at JUST (through the American people) have an answer: perform a financial distress test of your workforce to really understand what percentage of workers aren’t making enough to cover their bills each month.

That’s what we’ll be saying this week at the World Economic Forum as world leaders descend to talk about the future of stakeholder business, and that’s what we’ll be working directly with companies on throughout the year.

We know through conversations with C-Suite leaders that they are committed to creating and supporting quality jobs, yet we also know that assessments like these are rare, and that most haven’t done the analysis to know whether their workers are earning enough to support their families.

This assessment can have profound impacts on workers and the business. Earlier this year, we sat down with PayPal CEO Dan Schulman for our first Quarterly JUST Call to discuss what efforts he and his company have made to support the needs of all their stakeholders, most importantly their workers. To ensure PayPal was living its values around financial inclusion, Schulman asked for an audit of his hourly and call center employees, and found that 60% struggled to make ends meet and were living paycheck to paycheck, despite earning at or above market-level wages. Schulman took action – raising wages, reducing healthcare costs, making all employees shareholders and owners of PayPal, and driving financial wellness through education.

“If we ever aspire to be a good company, we have to have passionate employees who believe in what our company mission is, believe in our values, and — really importantly — are financially secure,” Schulman said recently.

We applaud Schulman’s exceptional leadership – and his efforts must become our social norm, not the north star. CEOs and Boards of Directors should take stock of their employees’ financial security.

Because it’s also good for business. When workers are more financially secure they are less likely to miss work and are more productive on the job. And we have years of research demonstrating that the companies that perform well in serving stakeholder needs create better returns for investors. They generate a higher return on equity (e.g. the JUST 100 have 6% higher ROE than peers), display higher net margins, higher operating margins, and higher valuation from investors.

JUST will be working through the coming year to support the C-Suite in their efforts to conduct this kind of analysis, providing guidance around what a financial stability assessment entails and what steps corporate leaders can take to ensure that their workers are able to cover their basic needs. We will also be developing tools and case studies, release ongoing research on which workers in America are earning a living wage, and build the business case for raising wages. We will work together with corporate leaders to ask better questions about the state of the stakeholders, and ultimately to build a more just economy not simply through words, but through action.

Following the 125th anniversary of Labor Day in the U.S. – celebrating workers’ contributions to companies and the economy – JUST Capital is excited to announce a new initiative dedicated to increasing the prevalence of quality jobs in America.

Each year, we poll the American public to find out what matters most to them when it comes to just business practices. And each year they prioritize worker- and job-related issues above everything else. This transcends partisanship, geography, and income – in other words, the American people are aligned.

Importantly, the majority of Americans think companies are falling short when it comes to their workers: 80% of Americans believe that companies do not share enough of their success with employees, and nearly 60% think companies are putting their shareholders above everyone else.

The public’s desire for change is understandable when you consider the current economic climate. Wages are slowly rising, but inequality is rising faster, exacerbating longer-run trends. Since the Great Recession, more than half of total income growth has gone to the top 10% of Americans. There are signs that such fundamental change is happening: the Business Roundtable took an important step last week, stating that the purpose of a corporation is to provide value to all stakeholders from employees to customers to communities, not just their shareholders. Business leaders have an opportunity to pursue practices that will make this vision for corporate America a reality.

That’s why JUST Capital is excited to be investing in a new Quality Jobs Initiative as part of our mission to align the market with the values of the American people. The key purpose of the Quality Jobs Initiative is to tie together all the work we’re doing on worker- and job-related issues, surface the business case for good jobs, and showcase the current state of play – from corporate leadership to new insights about types of work and practices – on quality jobs. We’ll be conducting new research on workers, contractors, and quality job practices, engaging companies in a series of one-on-one conversations and small group convenings, working to create more clarity and case studies on human capital standards and practices, and celebrating companies leading the way.

Our FREE weekly newsletter about the future of capitalism and the movement to build a more equitable marketplace in America.

The Quality Jobs Initiative will comprise four key areas:

Transparency and Disclosure: We believe that human capital disclosure is the first step of performance analysis and a key step toward change. Already this year, JUST Capital launched the Win-Win of JUST Jobs and the JUST Jobs Policy Tracker, which surfaces worker policy data across all 890 companies we track on nine issues – including diversity and inclusion policies and targets, tuition reimbursement, and work-life balance – representing hundreds of hours of work from our research analysts. This tracker enables anyone – from workers to corporate leaders to investors – to see, for example, every company that has conducted and published the results of a gender pay equity analysis. Over the next year, we will engage companies that do not yet disclose all their policies to make the business case for greater transparency and serve as a thought-partner as they work to achieve higher disclosure.

We are also pleased to be partnering with NYU Stern Center for Sustainable Business to provide their researchers with data on quality jobs so they can assess correlation between quality jobs and corporate financial performance across different sectors, as well as assess how well the “S” in ESG is capturing quality jobs.

Frontline Workers: Business leaders know that frontline workers are crucial to the success of their businesses. We are engaging companies with significant frontline workforces to identify and share policies that ensure frontline jobs are good jobs. In partnership with MIT Sloan Professor Zeynep Ton’s the Good Jobs Institute, we will be co-hosting corporate leaders in a workshop for companies to detail the business case for transitioning to a good jobs strategy. We’ll also be working with companies in surfacing best practices in training, scheduling, and other management policies.

Contract Workers: Increasingly, companies are contracting with vendors, temporary help agencies, and other entities to contribute to and support the production of their goods and services. We are exploring the role of corporate America in creating economic opportunity for workers reliant on these companies regardless of their employment status. Through engagement with companies we seek to advance research on the business dynamics driving the utilization of contractors and alternative work arrangements.

Mapping Wages: Underpinning all of the work described above is the research that shows that many workers in America don’t earn enough to cover life’s expenses. In addition to engaging companies on specific policies that would improve the economic outcomes of workers, we will be putting forth new ideas for how to measure, quantify, and think about wages. That includes mapping companies’ wages in America, assessing intra-firm inequality, developing a “Living Wage Index” to track progress, and modeling the economic benefits of businesses paying their workers a living wage.

We’re incredibly excited about this new work, and believe that by partnering with companies and foundations on this new Initiative, we can introduce new insights that make the business and investor case for quality jobs, thereby supporting a shift in corporate practice toward more just business behavior as defined by the American public.

We’d like to thank our foundation partners for their support of elements of the Quality Jobs Initiative, including: the Robert Wood Johnson Foundation, the Ford Foundation, the Annie E. Casey Foundation, the Surdna Foundation, the Nathan Cummings Foundation, the Alfred P. Sloan Foundation, and others.

by Alison Omens with contributions from Patrick Oakford.