For well over a decade, JPMorgan Chase has been developing a corporate responsibility arm that is integral to the bank’s business strategy rather than a silo of philanthropy.

CEO and chairman Jamie Dimon picked Peter Scher to lead this mission back in 2008, and Scher was so successful in this role that he was promoted to vice chair, where he continues to oversee the team he helped build. When it came time last year to choose his replacement, the firm chose Demetrios Marantis, who is tasked with maintaining the branch’s highly ambitious initiatives, including its $2.5 trillion, 10-year sustainable investment plan. And, as evidenced by the 2021 ESG Report released last month, he will also be leading the push to further crystalize his team’s corporate responsibility work as essential to JPM’s environmental, social, and governance goals.

Marantis comes to the role with a mix of experience in government, serving as deputy and acting U.S. trade representative under President Barack Obama, and the private sector, subsequently working for Square and Visa.

We recently caught up with Marantis to discuss what he’s learned in his eight months on the job, touching on how JPM developed its newly formatted ESG report and how he mobilized his team to confront the humanitarian crisis caused by the Russia-Ukraine war.

Do not allow headwinds to shift you off your long-term commitments

Dimon has spoken and written at length about the impact of the Russia-Ukraine war since it began in late February, from its effects on the global energy industry to its massive humanitarian crisis. In his introduction to the ESG report, he wrote, “A responsible approach to energy and climate, especially during a time of war, is to immediately help provide energy security around the globe while remaining focused on accelerating the development of affordable, reliable and lower-carbon energy solutions.”

As for the state of JPM’s investments in alternative energies, Marantis said that “this isn’t a question of either-or” when it comes to fostering short-term fossil fuel solutions while still plugging away at that $2.5 trillion goal. Progress toward it will happen despite how the U.S. and Europe figure out what to do with Russia cut off as an energy provider, Marantis said, reflecting what Dimon has also explained.

Develop processes that allow you to confront unexpected societal developments

Marantis’ 400-person global team were more directly responsible for how to respond to the devastation resulting from the war. He said that existing cross-team workflows based upon leveraging niche expertise allowed them to pivot quickly to Ukraine.

“We mobilized a cross-team group across corporate responsibility,” he said, including “our geopolitical experts, our government relations experts, our community engagement experts. And we worked with the business to craft a response that was very tailored to the immediate humanitarian needs at the time.” That included an initial $5 million commitment and employee-match that funded organizations providing emergency food, housing, and medical services. Last week, the firm allocated an additional $5 million to The Chamber of Commerce of the Polish Hotel Industry to assist the wave of refugees entering that country, and its employee-match continues.

Marantis said that much of this was built on the processes that evolved over previous corporate responsibility initiatives, resulting in a “muscle memory” that did not place the team at square one whenever a new crisis arose.

Make ESG-related initiatives intrinsic to the company’s success

JPM’s 2021 ESG report breaks down clearly each of its programs that fall into the E, S, and G, both internally and externally, and is introduced by Dimon.

In our discussion, Marantis was clear that Dimon’s mission to tie the success of corporate responsibility to the success of business overall was more concrete than ever. When talking about the bank’s diversity, equity, and inclusion (DEI) work, he pointed to its creation of demographic-centric centers of excellence that include both internal career development and external business development programs.

“We have a longstanding commitment to advancing an inclusive and sustainable economy, which is part of the firm’s DNA,” Marantis said. “This,” referring to DEI work, “has also become part of the firm’s DNA.”

Looking at the big picture, this year’s ESG report was the first to include an update on progress towards its $2.5 trillion sustainable development target – which is intended to foster economic conditions that will not only benefit communities, customers, and the environment, but shareholders, as well. The report notes that last year the firm invested $285 billion (11%) toward its target, with investments across initiatives such as underwriting sustainable bonds, supporting small businesses, and financing energy-efficient buildings. Much of its five-year, $30 billion racial equity plan launched in 2020 falls under its community development targets.

“What’s really exciting about where we are as a firm is this isn’t something that Demetrios Marantis from the corporate responsibility team thinks is important,” he said. “This is something that comes from Jamie, our CEO, and all of our business leaders.” He later explained that he was soon going to report to the board’s public responsibility subcommittee overseeing ESG progress, and expected to be grilled (in a way he looked forward to). “We take the full force of JPMorgan to address these challenges.”

Stakeholders want to see transparency, even if the results aren’t perfect

This year’s ESG report includes breakdowns of where JPM’s sustainability dollars went, as well as detailed, intersectional demographic data of its workforce. As ESG matures in the U.S., with the Securities and Exchange Commission preparing to codify a set of climate-related disclosure standards this year, and investors increasingly demanding data around the many green and DEI commitments companies have made over the past few years, transparency unto itself has value.

Marantis said that whenever he has interviewed candidates for a job recently, candidates ask him for details around the current state of and progress in DEI and corporate responsibility, rather than just accepting statements that sound good. “Applicants have a real choice of where they end up landing, and going to a place that takes these issues as seriously as we do is a differentiating factor.” This also applies to employees and managers already at the company, who demand the same level of transparency to ensure that the company is holding itself accountable.

“Advancing racial equity and promoting a sustainable economy – this isn’t going to change overnight,” he said. “It’s a sustained effort that we have to just keep plugging away at.”

Corporate America has played a defining role in responding to the crises of the last two years – whether protecting workers’ safety at the onset of the pandemic or addressing racial inequities in the workplace. JUST polling has shown that the public continues to look to corporations for leadership on these and other environmental, social, and governance (ESG) issues. But, as the war in Ukraine has highlighted, there’s no clear model for how companies should step up in these moments.

“The job of CEOs and leaders has become increasingly difficult, right? Because it’s a series of one crisis after the other with no playbook,” Hubert Joly, former CEO of Best Buy and JUST Capital Advisor said on how corporate leaders navigate these challenges at our event held Monday at Nasdaq, “The Strategic Imperative of the ‘S’ of ESG.” Joly was joined by PepsiCo EVP of Communications and PepsiCo Foundation President, Jon Banner, for a conversation on moving from commitment to action on ESG priorities.

Banner, who just returned from a trip to Poland around PepsiCo’s war relief efforts, and Joly, who authored the book “The Heart of Business” on his leadership philosophy, sat down with JUST Chief Strategy Officer Alison Omens to share how they’ve translated values into real action, with the outcomes to prove it. Read on for key takeaways and watch the full conversation below.

For PepsiCo, taking action on the company’s ESG agenda, PepsiCo Positive, has centered around “story-doing” instead of storytelling, Banner said. The company is focused on showing proof positive that it’s making progress on these goals, he said. That focus on story-doing has informed PepsiCo’s actions in response to the pandemic and, now, to the war in Ukraine.

“We spent close to a billion dollars to protect our workforce in the first year of COVID. It was a big investment, but we knew that unless we protected them and took steps to protect them, we didn’t have a company to run,” Banner said. In response to the war in Ukraine, the company is dedicated to protecting its 3,100 employees in the country – housing about a third of them, and their families, in its office in Warsaw. PepsiCo’s Warsaw office is now referred to as the “Warsaw hotel,” he said, and is equipped with 150 beds, washing machines, and a kitchen.

While the goal has first and foremost been the safety of its employees, PepsiCo’s also seen a unifying response from its actions. “The reality is there are, when you talk about story-doing, there are stories that coalesce the public in which there is so much divisiveness and hyper-partisanship, not just in this country, but there are certain stories that connect us on a human level. And that’s sort of what story-doing is all about,” Banner said.

Through the ongoing crisis in Ukraine, PepsiCo’s internal values are coming into play every single day, Banner said, and they reach into “every nook and cranny of the business,” including its factories’ walls. For him, living out those values puts a high bar and responsibility on leadership to embody them, particularly through crises like the pandemic or the war.

Joly echoed this sentiment, bringing up Best Buy’s immediate response to the onset of the pandemic. The company shut down stores to protect the safety of its workers and customers and while this meant a significant revenue hit, the board didn’t question it, Joly, who served as Best Buy’s board chair at the time, said. As the pandemic evolved, so did Best Buy’s response, continually guided by its values, he said. He raised the company’s partnership to expand broadband access in parts of rural Minnesota as one example.

“As leaders, when we go through a crisis, what do we go back to? We go back to our purpose. We go back to our values. We go back to understanding who are our stakeholders, and what good we can do for our stakeholders,” Joly said.

Omens raised the question of how best to measure or place value on these, in many cases, anecdotal ways companies are stepping up in times of crisis. For both Banner and Joly, the answer is not as straightforward. Banner, in particular, thinks that outcomes, instead of actions, are a better way of measuring how a company is living its values.

“I think when you look at what’s going on in Ukraine, when you looked at what certain companies did during COVID and certain companies did not, that wasn’t something you could measure. You could probably measure the outcome,” he said. In the case of war in Ukraine, PepsiCo has onboarded a dozen of its employees that have fled the country into new jobs in its Romanian operation. To Banner, that outcome of a dozen individuals with access to work is the measure of PepsiCo’s values in action.

Joly agreed and, on Ukraine, he thinks companies are being judged for their actions in a “naive” way, based solely on how quickly they are moving away from Russia. He contrasted the business of an oil and gas company, which may directly fund the Russian war efforts, to the business of Johnson & Johnson, a company where he and JUST board member Mark Weinberger sit on the board. “If you’re a pharmaceutical company. You’re not God, right? You don’t get to decide who’s going to die versus not die,” he said.

Joly also raised the importance of this nuance when it comes to looking at the materiality of ESG issues. “98% of questions that are asked as ‘either-or’ are better answered as ‘and,'” he said. He sees the role of business leaders as navigating this need to marry the short and long term, and not continue to operate as if people and profit are two separate entities. This is “the only way to run a business,” to him and he has future generations in mind with this outlook.

“I know in 10 years from now, 15 years from now, they’re going to ask me, ‘Happy, you knew right, the state of the world, you did know? What did you do?’,” he said, referring to his three granddaughters. “Not, ‘did you solve everything?’ but ‘did you do your best?’ ‘How did you behave?’ For me, that’s an important measure.”

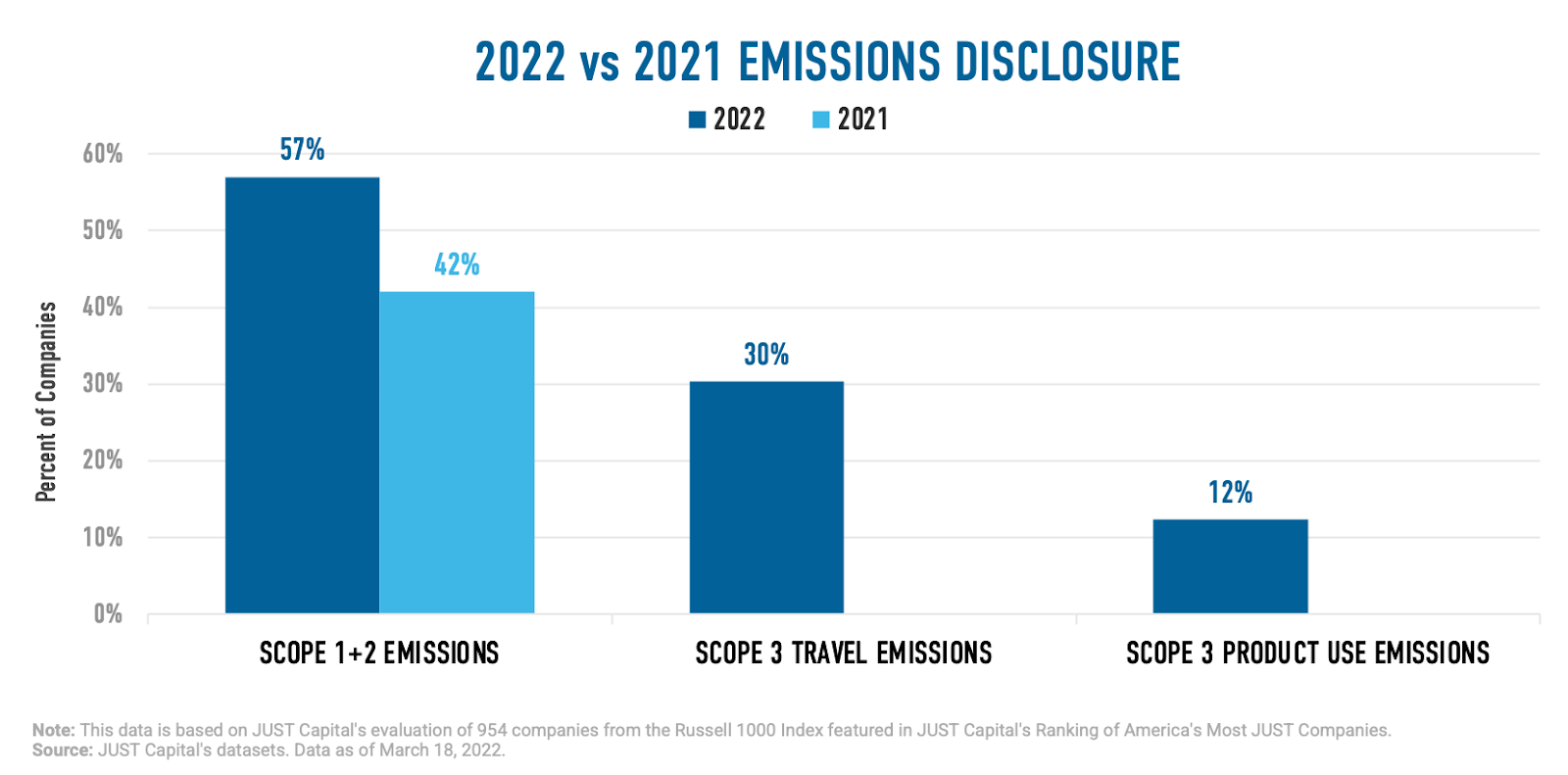

The SEC voted on Monday to propose a set of robust climate reporting standards that will move climate reporting from sustainability reports to 10-Ks, and the proposal will soon be open to public comment. This proposal includes requirements for greenhouse gas (GHG) emissions, and so we looked at the state of emissions disclosures of the Russell 1000 companies we track in our Rankings.

Scope 1 GHG emissions include direct emissions from company-owned operations, Scope 2 include indirect emissions usually from the generation of purchased energy, and Scope 3 are all indirect emissions not included in Scope 2 that occur in the value chain, including upstream (i.e. supply chain) and downstream (i.e. value chain) emissions. Scope 3 emissions can be broken down into 15 categories as specified by the Greenhouse Gas Protocol and the EPA.

A majority of companies (57%) disclose Scope 1 and 2 emissions. This represents an increase of 15 percentage points, from 42% in 2021. That means, then, that 43% of the country’s largest public companies have still yet to publicly release Scope 1 and 2 GHG emissions data.

Scope 3 data disclosure lags far behind, with only 30% of companies reporting these emissions from travel and only 10% of companies reporting these emissions data from use of products – the two categories that we looked at in our 2022 Rankings. This year, JUST Capital will be expanding our monitoring of all Scope 3 categories in order to build a more complete picture of the state of disclosure across the Russell 1000.

The SEC is not the only entity reassessing disclosure requirements. Last year, the European Unions unveiled its Corporate Sustainability Reporting Directive (CSRD), an expanded version of the existing Non-Financial Reporting Directive (NFRD), and it is set to be implemented in 2023, with the first reports due on January 1, 2024. The CSRD will cover more companies than the NFRD and also require assurances (audits) of disclosed data, starting off as limited assurance and using a progressive approach to widen the market for sustainability assurance services. JUST Capital will begin monitoring external verification statements of environmental data of Russell 1000 companies this year.

We will closely track how companies respond to the proposal, which following a public comment period may become policy as early as this fall.

The past few years have marked a generational shift in what it means for investors and companies alike to embrace ESG – environmental, social, and governance – factors, and among the most influential movers has been State Street Global Advisors. When we spoke last week with the giant asset manager’s CEO, Cyrus Taraporevala, and global head of asset stewardship, Benjamin Colton, the world was now contending with the ways the Russia-Ukraine war was going to affect ESG’s role in the future of business.

In his annual proxy voting guidelines letter to board directors of SSGA’s portfolio companies, representing more than $4 trillion in assets under management across 2,100 clients in 58 countries, Taraporevala asked readers to recognize the urgent need for clean energy transition clarity. He and Colton, who oversaw the development of this year’s guidelines, told us in our discussion that even though they sent the letter and guidelines in January, their guidance has not changed.

That’s because even though the war, the COVID pandemic, a reckoning with racial injustice, and alarming climate research have pointed out specific ESG risks, they’ve also highlighted that ESG is core to holistic investment strategy. As Taraporevala told us, “it’s very sloppy shorthand” to say that traditional “financially important metrics are somehow separate from ESG” with an ESG lens constantly shifting to meet an immediate ideological concern.

We discussed with Taraporevala the guiding principle of “value, not values” that he’s used in his six-year tenure as CEO (ending with his retirement later this year) and with Colton why and how SSGA has been a leading investor voice on increasing corporate diversity and transparency around it, and what both want and expect from this year’s proxy voting season, kicking off in April. Watch the full conversation below, and sign up for The JUST Report to get access to exclusive bonus clips not featured in the full interview:

The following interview has been edited for length and clarity.

JUST: I would say it’s safe to say that when you set up these guidelines for the year, that you likely weren’t predicting global conflict with Russia and a war going on in Europe. Does this war change your advisory or overall investment strategy for the near or long term?

Cyrus Taraporevala: When it comes to our proxy guidelines and ESG issues, by definition these are long-term issues that go over many, many, many years. We don’t react to things in the moment. Of course, what’s going on, like so many other things, does change our investment philosophies and tactics in the moment, including the fact that Russian securities are basically untradeable. But that’s separate and distinct. We will do what we need to do for our clients in the moment, but I just want to draw a distinction between the two topics.

JUST: Does there need to be a new set of expectations around the energy transition? With that being so fundamental to long-term climate strategies, and this conflict throwing the entire balance of oil and gas supplies around the world into disarray, how does that affect what you’d be advising to companies? Are these conversations that you’re having?

Taraporevala: In a sad way, because this conflict is terrible and tragic from a human perspective, it actually just reinforces what our proxy letter talked about when it comes to climate. We are pushing our portfolio companies to tell us not whether they want to get to net zero, but also as importantly tell us how are they going to get there. We also spend a lot of time talking about two concepts that I want to make sure you understand.

The first, which is very apropo of what you’re talking about, was this point that demonizing the fossil fuel industry and having this simplistic “green is good, brown is bad” approach was not something we subscribed to. We wrote about it in early January – we weren’t waiting for a war to talk about it. Our view is we are going to need fossil fuels for quite a long time through this transition. We believe the oil and gas companies are going to be part of the solution. They need to be part of the solution, so we need to engage with them. We need to work with them, support them, as they go through their transitions. And green versus brown is too simplistic. Think of it as a color spectrum, if you will. You’ve got dark brown – dare I say, dirty brown – forms of thermal coal, all the way to very light brown, think natural gas. And you’ve got green. You’re going to need some form of the lighter browns for quite a long time. And as I said, it’s sad but true, this recent conflict only reinforces and underscores that.

The second point we made about climate is this notion of what I coined in an op-ed in the FT last year “brown-spin.” Now, we all know what greenwashing is, right? So brown-spinning is basically where the pressure on publicly traded companies is becoming so heavy that they are looking at their highest emitting assets and basically saying, “You know what, I’m just going to sell them, get them off my books. I don’t have to deal with this topic of conversation with my shareholders.” But what does it really accomplish? Ultimately, they’re being sold to either private equity owners or some other form of maybe a state owned enterprise, or a hedge fund, et cetera. And in many cases, the level of emissions for the planet not only stays the same, but actually may increase because the new owner cares even less about it and doesn’t have the same pressures that a public company would have to make a transition on those emitting assets. Tragically for the shareholder of a publicly traded company, it’s often sold at a discount, i.e. the buyer sees a wonderful IRR.

So you have the worst of all worlds. You have the planet no better off, potentially worse off, and you definitely have the shareholder worse off. So what have we really accomplished? The frame I used in op-ed was imagine the world in 2050, where every publicly traded company can say they’re at net zero and have no emissions, but the total amount of emissions in the air and on the planet are the same.

These are themes that we have been talking about for a long time, and again, this current conflict simply underscores them.

JUST: Do you think that as it underscores it, it also sets back the timeline?

Taraporevala: I don’t know about that. I think it’s too early in this moment and probably very speculative depending on what scenario comes to pass. Right now when it comes to this conflict, our focus is on our clients and our people. We have quite a lot of people in Europe, people not too far from Ukraine and Poland, and people all over the world with family ties and loved ones there. The rest will come.

SSGA’s guiding principles

JUST: Can you tell me how the proxy voting priorities have changed over your tenures at SSGA and what stands out as unique about 2022’s guidelines?

Taraporevala: There are three core beliefs that we hold very strongly to.

The first is that strong, capable, and independent boards are truly the linchpin for driving long-term shareholder value, and that has not changed. We are steadfast in that belief.

The second is that when it comes to our asset stewardship activities, it is about value, not values. And this is a difficult one because we all do have values. We’d love to espouse them, but when it comes to other people’s money, which we are the fiduciary for, we have to ask ourselves, how does this drive value? How does it either increase the returns or mitigate the risk? That is our North Star.

And then the third, starting to get to the other part of your question, is we’ve been at this for a long, long time. We’ve been at many of the topics we are talking about in our proxy letter for well over a decade. We have been pushing our portfolio companies to improve their disclosure on topics that we believe, in addition to the more traditional financial metrics, do drive long-term risk-adjusted value. We’ve been pushing them on effective board oversight.

So if you just do a quick checklist of what’s stayed the same, what’s changed, and how has it evolved? You could say broadly on ESG that “G” is the furthest along. That’s where a lot of this started. And really, this goes back to Graham and Dodd. Well-managed companies with good boards do better and should be accorded a premium. There’s nothing particularly “ESG” or new about it. On climate, we have believed for a long time in the systemic risks around the “E.” But I would say certainly the level of focus and emphasis more broadly has increased over the years, and we think will continue to increase over the years. And the “S” is probably the epicenter of where the greatest change has happened over the last several years.

We’ve been ahead of the curve in terms of asking our portfolio companies for more disclosure on human capital management, but I would say all else being equal, the clarity of our expectations has increased. The way we are holding boards accountable, using not just our voice, but even our vote, that has gotten sharper.

When we think about our proxy guidelines, we don’t actually start with what’s going to be unique and super different every year. In some ways that would drive our portfolio companies crazy and is not really in the best long-term value creation interest. They are slow burn issues that take years, and we want to signal to our portfolio companies well in advance that these are the issues we’re going to talk about. We believe consistency is a good thing, because otherwise you just rip some of your portfolio companies around and nothing happens year over year.

Ben Colton: In the past decade, we said that climate change is a material risk for all companies, that it’s an issue that belongs with the board, and we published guidance on effective oversight of climate change and climate-related risk. And this year we’ve escalated it to really articulate what we’re expecting from a climate transition plan. We’re going to have targeted engagement campaigns on some of the most heavy emitting companies in our portfolio.

You can also see this on the social side. When we launched our Fearless Girl campaign, which held companies accountable for having at least one female director on the board, it wasn’t about having a token female director, this was really about diversity in thought – a critical mass of diverse perspectives that lead to benefits of seeing risk differently and having less groupthink, more innovation, and better business outcomes overall. We’ve escalated our expectations for companies not only on gender diversity, but to have directors from underrepresented communities. This year our voting guidelines expect 30% female representation on boards in addition to one director that’s from an underrepresented community, in developed markets, and the expectation of one female director is expanded to all markets.

The other trend that we’re seeing is a lot of blending between the issues. We’re seeing how corporate governance issues are also mixing with environmental and social issues. How does the board oversee a climate transition, or think about risk management related to racial and ethnic diversity, and human capital management? We’re also seeing shareholder proposals asking for more disclosure on how the board is overseeing these issues. And with a just climate transition, that’s a combination between social and environmental issues. How are our companies thinking about the transition and also about their workforce and the communities in which they’re operating in that context? How are they going to reskill and retool their employees when their business lines change? How are they going to think about those communities in which they’re impacting and operating within?

‘Value, not values’

JUST: Something that tie this all together is, Cyrus, what you said about value, not values. Can you unpack that a bit? Every week you’ll see debates around, “Oh, is this ‘woke capitalism,’ are companies getting too ideological?” And you see pushback from either side, from those saying companies aren’t doing enough to those saying they’re doing too much.

Taraporevala: Look, that narrative is definitely out there. But as I said, for us, this is not about politics. This is not about what’s “woke.” This is about the best risk-adjusted return. A huge part of our business is indexed assets. And in many ways, index equities are quasi permanent capital. As long as the company’s in the index, my index managers, unlike my active managers, have to hold that company in their portfolios, which means they don’t have the luxury of saying, “I don’t like what’s going on, let me just press a button, let me get out.”

And for some strange reason, my clients don’t like the S&P 499 worth of returns, they expect the S&P 500 worth of returns. So we have to engage with these companies, we have to think about the long-term risk adjusted returns.

For us, this “value not values” compass really helps us. It’s human, it’s natural, to want to sometimes have your values reflected. But we have to catch ourselves and say, no, no, no, that’s not this topic. We have to focus on value. We don’t subscribe to the idea this is political, and it’s actually a shame that narrative is being framed as such.

JUST: Reading the guidelines and hearing everything that both of you are saying, these arguments are very much tied back to a common sense assessment around risk and value creation. A lot of what this would be considered though, too, is ESG. Is it still useful now in 2022 to consider ESG as an alternative lens to assessing a company, or are lines blurring between what is just smart management, smart investing, and what is ESG?

Taraporevala: We’ve never actually bought into this ESG/non-ESG dichotomy. It’s just not binary. Here’s the way I think about it. An investor puts together a rich mosaic of different data and information that drives her decision about whether or not to invest in a company. (And I’m purposely focusing on the active side for this part of the conversation.) Different investors can look at that same rich mosaic of data and information and reach different conclusions. That’s cool. My equity value managers have a very different portfolio than my equity growth managers. So we are not suggesting the answer needs to be the same, but we do believe that having the right data and information disclosed is important, from which different people can reach different conclusions. That’s the wonderful thing about markets. It’s very sloppy shorthand to say financially important metrics are somehow separate from ESG.

There are traditional financial metrics – think FASB. And there are ESG metrics that also ultimately drive risk-return tradeoffs, so they are very meaningful financially. To us, it’s putting it all together. For example, when we engage with our portfolio companies, we don’t have just our asset stewardship team engaging with companies. We have our portfolio managers on the active side, side by side with our asset stewardship team at meetings with companies, and when the time comes to decide our votes, there’s a discussion and perhaps even a debate among our folks.

My hope, maybe it’s my naive dream, is that in seven to 10 years, and I fear it might take that long, we’re not even talking about ESG as a separate thing.

When I go around the world, I don’t have clients say to me, “Do you think about price to earnings? What about dividend yields? How are you thinking about price to book?” That’s part of the mosaic, right? And just given the newness of ESG, parts of it do feel a little different, and it’s going to take a little time for folks to adjust to it. But again, I go back to governance. I grew up studying Graham and Dodd, and it was always very clear that good companies should be accorded a premium and governance was part of what a good company was. Good management, good boards. So we never said, oh, but that’s separate, let’s take that out of the regular Graham and Dodd analysis and have it in a separate bucket and we’ll come up with different portfolios based on that.

Colton: One of the crucial factors of this ESG discussion is more quality and consistent data, as well. As we have more historical data, as we all coalesce around common standards – we think SASB is a really good starting point – that conversation will continue to evolve as we get more clarity around how we’re measuring outcomes. We joked one time with a company, where they said the quickest way that we’re going to reduce our carbon emissions is by just changing our data provider. And that shouldn’t be the case, but sadly that is the reality.

We can’t even get consistency among the same data points that we’re looking at. But we do think that is improving, and one of the ways to continue to get more consistency is by having asset managers and asset owners be clear on what their expectations are, be clear to companies on what kind of disclosure they want to see and what’s going into their analysis. How are we thinking about net zero as an asset manager and what kind of disclosure do we want to see? We need to understand the guardrails, and the interim goals of achieving those long-term expectations.

What the ‘S’ means in 2022

JUST: You mentioned how much the “S” has changed in recent years. Can you tell me how State Street defines it now?

Colton: Cyrus’s letter three years ago underscored the importance of board oversight responsibility in thinking about corporate culture. That is so closely connected with human capital management. How is the board monitoring, enhancing, and overseeing corporate culture? How are they holding management accountable for identifying hotspots within their organization, or integrating the voice of employees and using not only the risk KPIs, but also synthesizing information? What a company needs to be successful for the next 10 years is probably known somewhere within the organization already. How do we track that information and how does the board utilize their employees to the fullest?

Now we’re also seeing the Great Resignation, and this competitive landscape for talent, and also a work from home environment for many companies. Attracting and retaining talent and creating a corporate culture, maybe in an untraditional way, is more important than ever. These are the types of things that we’re talking about with companies, and we’re trying to be clear on what our expectations are and what kind of disclosure we want to see. And that really comes through in some of those guidance pieces that were attached to Cyrus’s letter this year.

JUST: On that note of how companies are navigating the challenges around labor over the last year, where there really seems to have been a shift in dynamic between workers and management of companies, what are you advising in regards to how much a company should be investing in its workforce while also navigating the fears of inflation and the overall difficulties of this economy?

Taraporevala: We are mainly asking questions of companies – we are not here to dictate. That’s between management and their boards. How are you thinking about it? How important is talent and labor to being able to enable your strategy? Where are you seeing the major pressure points? How is your attrition? How is your ability to attract new talent? How is your ability to attract diverse talent? We hold boards accountable, boards hold management accountable.

JUST: Target announced in their last earnings call they are planning a major investment in their workforce, where starting salaries are going to range from $15-24 an hour. Other companies have made similar investments recently. Do you expect to see more companies investing in their workforce in this moment?

Taraporevala: I’m not commenting on individual companies, but will talk generally.

I don’t really buy into this narrative of companies are now suddenly, over the last one or two years, investing in their workforce. We believe great companies have invested in their workforce for a long, long time. The specific tactics may vary, but investing in the workforce – which is a lot more than just compensation, it’s about helping people think about their careers, it’s about advancing their careers, it’s about mobility, it’s about the culture of the organization to attract, retain, and motivate a great workforce – that’s always been a huge competitive advantage for some companies.

JUST: Ben, broadly speaking, what do you expect of this year’s proxy season? And should we expect some more ESG-centric battles similar to what we saw with Engine No. 1 and ExxonMobil last year?

Colton: That was really about long-term strategy and finding and determining which directors are best suited for overseeing such strategy. What I will say is that as human capital management becomes more and more important, and get more disclosure around those issues or see the lack of disclosure from some companies, I would suspect that you’re going to see the social issues appear more and more in those discussions when you see contested situations, because it really is a material issue for all companies.

JUST: So issues like around pay or gender diversity, equity, inclusion, those types of issues.

Colton: I think broadly human capital management, how a company is looking at their workforce, its composition, all of the issues we’ve underscored as material. I would expect to see companies disclosing more information, and also in those contested situations, that information being further up in the pitch deck, so to speak, than it was in the past.

We filmed this interview and will be releasing clips like the one below, along with a lightly edited full Q&A video, including material not included in the above feature. To make sure you don’t miss any, subscribe to our newsletter and follow us on Twitter and LinkedIn.

Meta, Facebook’s parent company, saw its stock plunge 26% on Thursday, for a massive market capitalization loss of $250 billion. The fall came a day after an earnings call that gave investors cause to worry about the company’s transition to a focus on the virtual reality-driven metaverse.

There are multiple reasons analysts have cited for this, primarily around growth and strategic direction. However, several are tied to the decline of Meta’s standing over the last couple of years within the ESG (environmental, social, governance) space, including in our own Rankings of America’s Most JUST Companies.

As CNBC’s Eric Rosenbaum asked in a piece last month about the 2022 Rankings, “Can any ESG investor own Facebook?” He pointed to Meta’s fall all the way from #21 in our 2021 Rankings to #712 on account of “unique and extraordinary actions.” His CNBC colleague Kristina Partsinevelos noted in a recent television segment, Meta and its previous incarnation of Facebook can be seen as a prime example of the importance of “G” in ESG.

In JUST’s model specifically, Meta actually performed well across issues that took into account investments in workers, communities, and the environment. Its governance, broadly speaking – on account of scandals concerning lack of transparency and misleading information to shareholders and customers – so far outweighed its positive stakeholder scores that our Research team incorporated significant penalties. Meta ended up ranking it #901 out of 954 companies on Customer Issues and ranked #666 on Shareholder and Governance Issues.

Facebook told CNBC it takes its responsibilities around customer privacy and its impact on the potential spread of misinformation seriously, and indeed Meta is still included heavily in ESG funds from the likes of Vanguard and Flexshares. For others, however, the governance concerns required intervention. As CNBC’s reports noted, MSCI downgraded Meta’s ESG rating to B, its second to lowest score; S&P dropped the company from its ESG index in 2019 over privacy concerns; and ESG investor Trillium dropped it over a year ago on account of what it deemed a reluctance to address its biggest scandals.

On top of all this, analysts also noted that the market seems to be losing confidence that Meta’s long-term plan built on the metaverse is going to work. As Mike Isaac put it in the New York Times, regarding Meta CEO Mark Zuckerberg’s ability to innovate his way past a challenge, “In the past, Mr. Zuckerberg might have been given the benefit of the doubt that he would be able to do so. But on Thursday at least, faith was in short supply on Wall Street.”

Meta, née Facebook, may have been able to weather the storm of scandals past thanks to its ability to deliver on expectations. As for its current predicament, it faces the not insignificant challenge of rebuilding trust with the public and convincing the street about its future. Perhaps it’s time for Meta to formally and fully embrace the stakeholder model?

(PwC; Evgenia Eliseeva)

Last year, in the depths of the pandemic, Americans looked to the heads of business for leadership in a frightening, uncertain time.

Our polling found that 90% of Americans believed that the spread of COVID and societal unrest provided an opportunity for companies to hit “reset” and focus on doing right by their workers, customers, communities, and the environment. Separately, Edelman reported in its 2021 Trust Barometer that business was the most trusted institution among those it tracks. If companies were going to take their commitments to stakeholder capitalism seriously, a pandemic and renewed push for racial justice appeared to be an ideal test case.

But we’re seeing signs that confidence is slipping. As our CEO Martin Whittaker highlighted of our sixth annual Americans’ Views on Business Survey: “Only 49% of those surveyed believe companies have a positive impact on society (down from 58% in 2018); nearly 60% said capitalism is not working for the average American; only 36% believe companies are having a positive impact on the financial well-being of their lowest paid workers; and a mere 22% believe business is headed in the right direction.”

If companies want to come out the other side of this pandemic and its recovery strong, it is clear that they need to build trust among all their stakeholders. That’s why we reached out to PwC’s U.S. chair, Tim Ryan, who’s overseeing the firm’s Trust Leadership Institute, and one of its guest speakers, Harvard Business School management professor Sandra Sucher. PwC developed the Institute as a way to train executives on stakeholder- and ESG-driven leadership, and launched its first session – with 184 companies represented – last month. Ryan told us that PwC is using these same techniques for its own organization, and Sucher was a natural fit as a keynote speaker, given her specialization in how corporate leaders develop trust.

We’ve collected lessons from our interviews with both, drawing from what’s taught in the institute and in Sucher’s recently published book, “The Power of Trust,” coauthored with Shalene Gupta.

Developing confidence and stronger relationships with stakeholders requires, of course, an ongoing process, but the lessons below are intended to set leaders in the right direction, and touch on what Sucher says are the four elements of trust – competence, motives, fairness, and impact.

“My biggest advice is don’t let the past encumber your thinking,” Ryan said of his discussions with leaders on the subject of trust.

“The world is changing, work is changing, the relationship with workers and employees is changing,” Ryan said. “Old-school thinking is a bit of an excuse.” He mentioned the example of how business leaders are having to decide which aspects of flexible work they are going to maintain as pandemic restrictions continue to loosen. The pandemic has inspired frontline and office workers alike to demand more from their employers, and it would be a mistake to ignore their voice.

Ryan said that he pushes against those who insist that there is a correct way – the traditional way – to develop culture at work, requiring all employees to be in the same physical space. As the recovery continues to be messy and unpredictable, leaders need to maintain the trust of their workforce by acknowledging that the goal should not necessarily be a full return to “normal,” but that learnings on flexible work can continue to be beneficial and lead to higher engagement and productivity among office workers.

Sucher said that companies need to own the discomfort that comes with rebuilding trust in the wake of a major scandal, setback, or poor performance. “People want to know that you see the reality that they see,” she said.

She said a simple three step process can help guide this repairing of trust both internally and externally: Recognize the mistake without glossing over its impact and apologize for it, explain exactly what went wrong that led to that mistake, and then set a clear and detailed path on how the company is going to correct its course.

Chipotle CEO Brian Niccol pulled this off quite successfully. When the board brought him into the company in 2018, Chipotle was marred by a succession of food safety scares. Niccol made health and safety across all aspects of the business fundamental to his leadership style, and regularly communicated to the public exactly what broke down in its supply chain that led to customers buying tainted food. His embrace of, and then reaction to, the potentially fatal setback not only led Chipotle’s stock to eventually hit new highs, but placed the chain in a position to weather the pandemic better than many of its competitors.

Our survey research over the past year has made clear that the majority of Americans support efforts to develop racial and gender equity in pay and representation across different levels of companies, but transparency across all human capital metrics at America’s largest companies remains quite low.

Ryan said that he applauds business leaders who are willing to make commitments or statements on issues that their stakeholders value, but he then asks them, “Have you changed the way you’ve done business?” and, “Are you willing to tell a transparent story, even when it’s not perfect?”

Your workforce, potential employees, and investors are not going to trust your words, he explained, if you are not willing to provide a look at the reality of the situation. For example, when PwC US announced a new set of diversity, equity, and inclusion (DEI) efforts last year, it also released its first report detailing demographic breakdowns across its organization. Ryan noted in a blog post that the numbers were not ideal, but were important for tracking progress and holding itself accountable.

Similarly, there is a wealth of climate commitments out there, but very little accessible insight into how these plans will be achieved. According to DataDriven EnviroLab and the New Climate Institute, only 8% of companies that have net-zero emissions goals have interim targets.

It’s no wonder, then, Sucher said, that investors aren’t assured, after we shared with her the Edelman statistic that “86% of U.S. investors believe that companies frequently overstate or exaggerate their ESG progress when disclosing results, and 72% of investors globally don’t believe companies will achieve their ESG or DEI commitments.”

Speaking specifically about the many net-zero targets targeted between 2030 and 2050, Sucher said, “There’s nothing else in business we do on that time horizon,” and so “that skepticism is warranted.” If you want investors and other stakeholders to trust that you are taking their desires seriously, you should complement your big-picture goals with milestones and explain how you will meet them, she said. Our Research team has identified Microsoft as a standout in this regard.

In this year’s Americans’ Views on Business survey, we found that 63% of respondents believe that CEOs should take a stand on social issues. As we’ve seen over the past year, several companies have struggled with this, afraid of losing trust among certain stakeholders through either a stance or lack of one in regard to a major political debate in the country, such as the controversial Georgia voting bill passed in April.

Sucher said that companies have to acknowledge now that whether they make a statement, take action, or choose to be silent, there will be people unhappy with their decision. Rather than try to read which option would be most popular, Sucher said, “The question is who are we with respect to this issue?”

The answer to this question can be quite complex and difficult, but a company’s trustworthiness is built on its relationships with its stakeholders, and those relationships rely on that company working toward its purpose.

PwC has doubled down on educating clients on matters of ESG investing and how that is tied to long-term, sustainable corporate leadership.

“This is only increasing in size in magnitude, and we’re encouraging clients to own this opportunity for what it is – but also appreciate that this is not a quick fix, to simply put it off into the corner with a chief sustainability officer,” he said.

ESG investing and corresponding stakeholder leadership is not a fad, he explained, but something that will only grow more popular, as well as formalized with federal ESG standards on the horizon. But if companies are going to convince their stakeholders that they are taking it seriously, they need to integrate these initiatives into the core of their business.

“Change your supply chain, change your reporting, change your infrastructure, change the way you run your business,” he said.