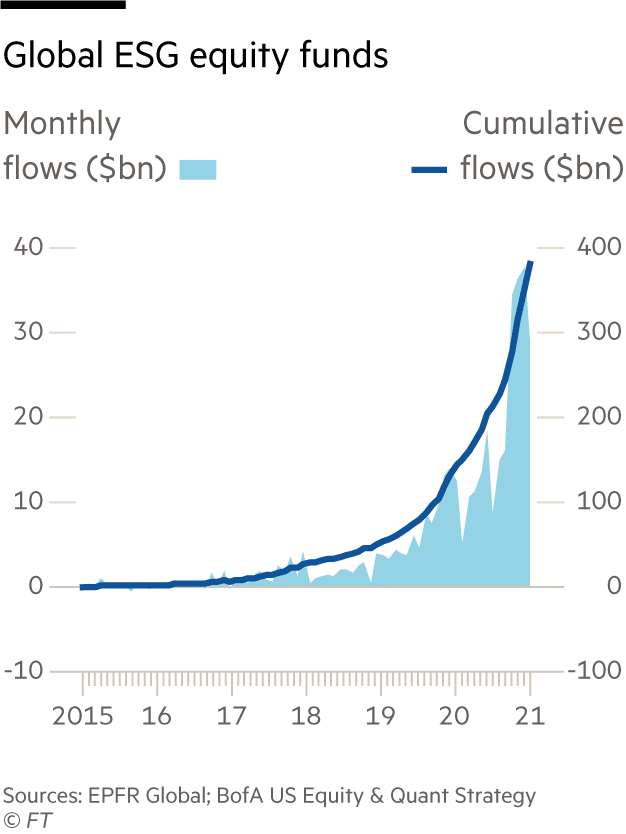

This week’s chart pulls from the Financial Times’ Moral Money newsletter, which references research from Bank of America highlighting the continued hockey-stick growth of ESG investment. Looking at the data from EPFR, we see that North American ESG equity funds raked in $12 billion through February 2021, up 122% from the year earlier, while Europe’s ESG equity funds recorded $853 million in inflows through February 2021, up 59% over the past 12 months.

Considering the chart above, it is hard not to look back at how much has changed since the beginning of 2020. We have seen flows into ESG funds go from roughly $5 billion to nearly $400 billion in that timeframe which begs the question many have asked: what constitutes an ESG fund?

The debate has been playing out for years now: How ESG is defined? To what extent must ESG be integrated into the investment process? How can we measure ESG impact? There are frequent claims in the media that ESG is entirely greenwashing – a term meant to label funds as sustainable investments for purely marketing and distribution purposes – from folks like the ex-CIO of Blackrock in USA Today. And we see counter-arguments from those like Jon Hale at Morningstar and Matt Christensen at Allianz in Barrons, debunking claims from naysayers and emphasizing that ESG investing will play a key role in addressing the most critical challenges of our time – from climate change to income inequality to racial equity.

Leaning on data to address the point of rebranding, Morningstar’s 2020 Global ESG Sustainable Funds Report points out that 253 existing funds were repurposed globally – 87% of which reflected the change by rebranding, representing one third of all new ESG products in 2020. Repurposed funds that rebrand add terms such as sustainable, ESG, green, or SRI to their names as a way to increase their visibility among investors who are looking to invest more sustainably. From the new prospectuses, it is easy to see that some strategies have truly repurposed and altered their underlying investment policy, but harder to discern how or if other strategies have changed.

Regardless, it is clear that we need a baseline for measurement globally. There is progress being made. The SFDR (Sustainable Finance Disclosure Regulation) finally took effect last month in the EU after three years of preparation. With the U.S. expected to follow suit, this is a first major step forward in mandated ESG disclosure that requires asset managers to disclose both the intended positive sustainability effects along with any negative externalities of their strategies. As the SFDR looks to better contextualize the ESG fund landscape, especially as funds continue to rebrand/repurpose, it makes it even harder for investors to understand if their money is having a positive impact.

Furthermore, the SEC, which over the past administration had failed to consider evidence that ESG considerations can improve long-term investment returns, issued an ESG Risk Alert this week published by the Division of Examinations to highlight that “ESG asset managers are put on notice that future exams will target ESG practices as they relate to three operational functions: portfolio management and proxy voting decision-making; performance advertising and marketing; and compliance programs for ESG investing and disclosures”

As new regulations like the EU SFDR continue to be adopted and the SEC finally starts to make progress on addressing ESG integration, we cannot wait for regulation to catch up. With proxy voting and AGM season on the horizon, a wide range of issues captured in ESG investment strategies – from climate change to workplace diversity – will be addressed and voted on. It is important that all shareholders – institutional or otherwise – voice their opinion and understand the ways in which investment funds are voting to ensure corporate commitments are enacted and investment policies are implemented in the right ways. It is the primary way that individuals can have a say in how public companies around the world are governed.

Lastly – to the point of understanding how companies are following through on commitments to issues such as systemic workplace inequality in light of AGM season, JUST Capital released the Corporate Racial Equity Tracker to measure how companies are walking the talk.

If you are interested in supporting our mission, we are happy to discuss data needs, index licensing, and other ways we can partner. Please reach out to our Director of Business Development, Charlie Mahoney, at cmahoney@justcapital.com to discuss how we can create a more JUST economy together.