This week’s chart looks holistically at the broader trends in sustainable finance to evaluate the ESG fixed income space. Our commentary pulls two charts from the S&P Global’s market overview published last week, Environmental, Social, And Governance: How Sustainability-Linked Debt Has Become A New Asset Class.

Before diving into this analysis, it’s important to understand the current state and growing trends in the sustainable debt market. Over the past five years, ESG debt issuance has gone from the niche market of government-issued bonds, used to finance local renewable energy projects, to a $732 billion dollar industry1. Per BloombergNEF, sustainable bond issuance grew 29% in 2020 from 2019, driven by a sevenfold increase in social bond issuance of $147.7 billion for social projects amid fallout from the pandemic. This growth is continuing at a pace in 2021 set to surpass last year’s record.

Organizations are continuing to iterate the types of bonds they’re issuing to drive sustainability forward. But one type of issuance, green bonds, captures the majority of the sustainable debt market with $305 billion issued globally during 2020. A green bond is a fixed-income instrument issued by companies with the explicit purpose of financing environmental or climate-focused expenditures. This can include financing for expansion of the subway system, like the New York MTA did, or even the sovereign expenditures, including the green bonds Italy recently issued that received over 80 billion in orders for 8.5 billion euros in debt to finance sovereign expenditures related to low-carbon transport, power generation, and biodiversity.

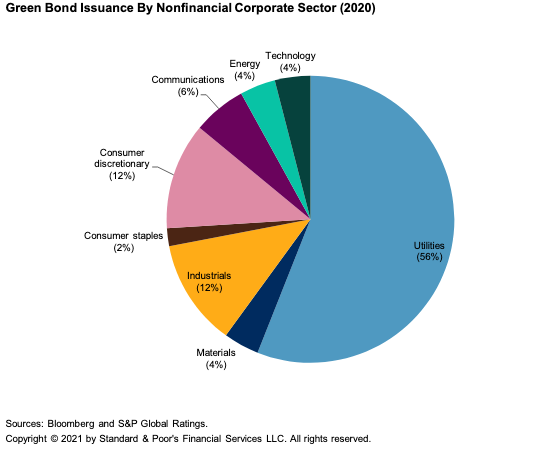

Green bonds continue to raise record levels of financing, but are largely limited to companies that have various capital expenditures connected to environmental projects or initiatives and fall into the utilities sector. As the chart below shows, these companies issued bonds raising 56% of the total green bond dollars invested in 2020. However, a newer form of raising capital, the sustainability-linked bond, opens up the possibility for companies at the beginning of their sustainability journeys or that fall into “hard-to-abate” (meaning most challenging to decarbonize) sectors to raise debt in a similar fashion while advancing their own ESG initiatives.

A sustainability-linked bond (SLB) is a new form of green financing in which companies issue a debt instrument with the intent of raising financing tied to achieving a predefined KPI (key performance indicator) or set of KPIs over the duration of the bond maturity. What is unique, however, about SLBs is that they open up the sustainable debt field to all companies, regardless of sector or resources and can be used for general purpose – not explicitly for environmental expenditures.

For example, if an issuer is looking to raise debt to achieve a large-scale reduction in carbon emissions, they can issue an SLB linked to a predetermined KPI over the maturity of the bond at a discounted coupon rate (or cost) that will ratchet up or down depending on whether or not they have reached the set target. This enables an issuer to achieve a cheaper cost of debt or “greenium” from investors in exchange for following through on the KPI targets. We’re also seeing companies use the sustainability-linked KPI framework around broader ESG commitments – not just environmental targets. Earlier this year, the Carlyle Group linked a $4.6 billion credit facility to KPIs to increasing board diversity.

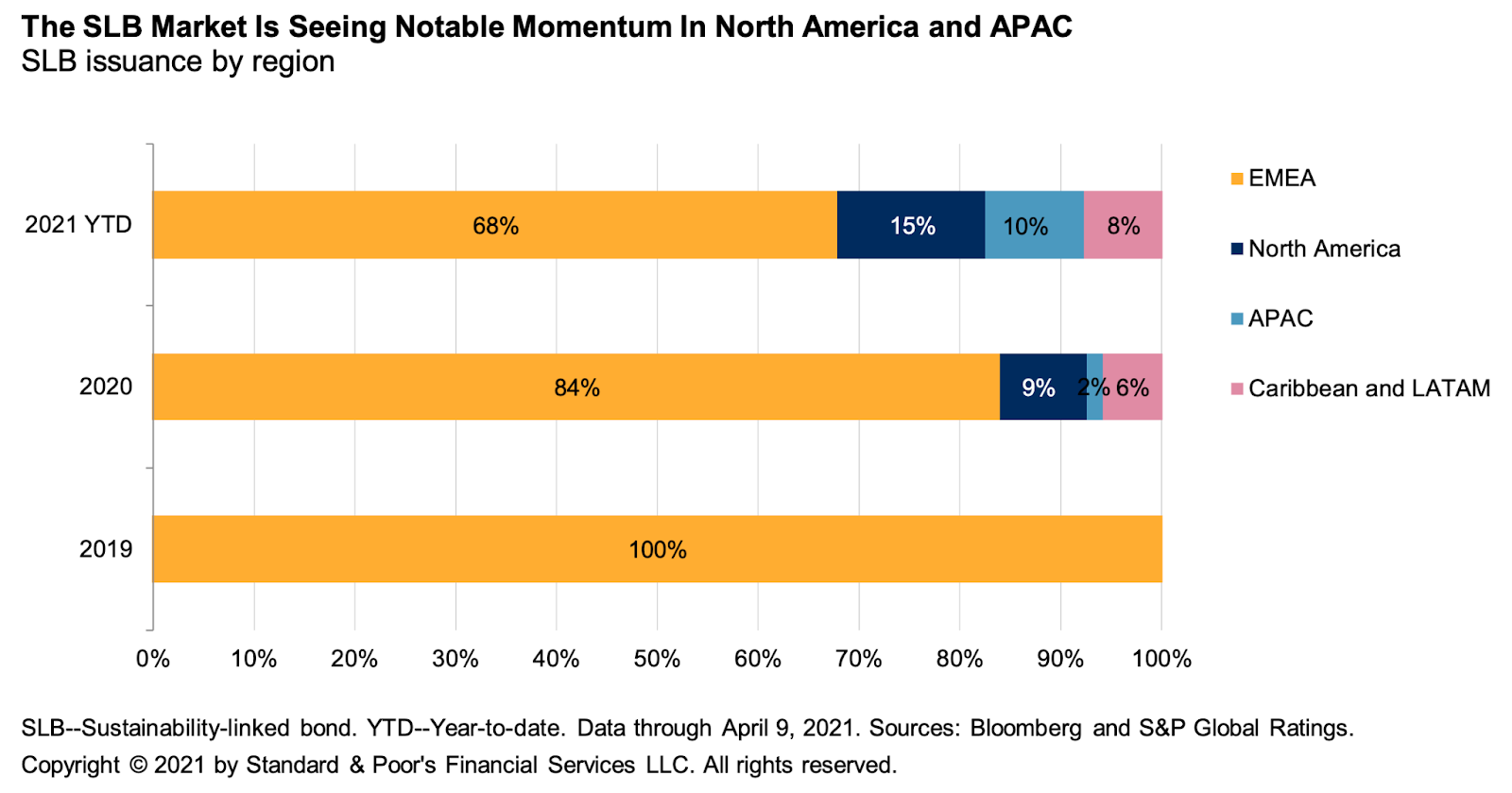

Looking to the charts from S&P below, we see a steady rise occurring in the SLB market over the past 2.5 years with North America moving from 0% of the global market to 15% so far in 2021. “2021 will be the year of sustainability-linked bonds.” Marilyn Ceci, global head of ESG debt capital markets at JPMorgan, said in a recent Bloomberg article. “It’s going to be the fastest-growing sustainable instrument that we have if we extrapolate what we’ve seen already.”

SLBs remain a nascent asset class, but are rising significantly with 13 launched YTD in 2021. As issuers continue to iterate, SLBs represent a win-win opportunity. The ability to leverage SLB financing not just for environmental and governance initiatives, but for social initiatives is a unique and important way for organizations to quantify and transparently progress upon their commitments to social issues.

The opportunity to tie goals and KPIs to debt in a meaningful way empowers organizations to follow through on their commitments to diversity, equity, and inclusion (DEI), workforce financial health, and more. As JUST Capital tracks how they’re taking action against DEI commitments in our Corporate Racial Equity Tracker, SLBs present a massive opportunity for companies to tie their targets to debt financing to achieve a lower cost of capital and publicly follow through on their pledges.

Ultimately, with all of the talk of greenwashing and only 29% of the 444 companies in the S&P 500 in 2020 hiring external assurance to verify their CSR reports, SLBs are a differentiated way to prove organizational commitment in a quantifiable way while being incentivized by investors to do so. The social metrics we track – board diversity, workforce demographics, and pay equity among others – are all industry-agnostic metrics upon which all companies can improve, regardless of size. As organizations grapple with their journey toward becoming a truly stakeholder-driven company, being rewarded with cheaper financing for doing so makes following through on these commitments a win-win opportunity they shouldn’t pass up.

1: BloombergNEF defines their sustainable debt universe as “consisting of green bonds, green loans, social bonds, and sustainability bonds that follow the use-of-proceeds requirements set by the International Capital Market Association (ICMA) and Loan Market Association (LMA), as well as all sustainability-linked bonds and loans that follow the guidelines set by the ICMA and the LMA.”

If you are interested in supporting our mission, we are happy to discuss data needs, index licensing, and other ways we can partner. Please reach out to our Director of Business Development, Charlie Mahoney, at cmahoney@justcapital.com to discuss how we can create a more JUST economy together.