Jennifer Tescher, Financial Health Network founder and CEO. (Financial Health Network)

As politicians and business owners and leaders across America debate how much the government and companies can afford to pay in wages and which benefits encourage or discourage work, what is always central, whether explicitly or not, is the idea of Americans’ financial health.

That is, what does it take for people to make enough money to live, and are their benefits designed to actually be useful?

Jennifer Tescher, CEO of the Financial Health Network, is dedicated to helping institutions develop a holistic understanding of what it takes for Americans to lead lives where money is working for them, which in turn strengthens the communities they live in and the businesses they work for.

Tescher founded FHN in 2004 after first spending time as a journalist in the early days of data-driven journalism and then entering banking. In a recent interview, she told JUST Capital that with journalism, she was “in it for the issues, not the writing,” and when she ended up working for a bank, which she hadn’t initially planned for, she “came to appreciate the power of the private sector to achieve scale.” FHN became a way, then, the bring together her love of data and passion for finding ways business could help people live more fulfilling lives.

It’s why JUST and PayPal brought FHN on as a partner to our Worker Financial Wellness Initiative, a coalition built around the idea that when corporations commit to understanding the financial health of their workforce, particularly their lowest paid workers, they will be able to know how the benefits they’re providing are being used and whether their wages are livable. Along with our fellow partner the Good Jobs Institute and anchor member Chobani, we are asking companies to commit assessing the financial health of their lowest paid workers as an important first step toward building more resilient companies that benefit all stakeholders over the long term.

Before the pandemic hit last year, JUST Capital estimated that roughly half of the workers at Russell 1000 companies, about 10 million, weren’t making enough to support a family of three, even with a partner working full time. And as we discussed with Tescher, the past year’s pandemic and reckoning with racial injustice has made the project feel even more urgent.

Our conversation explored the interwoven business and moral cases for companies first understanding and then enhancing the financial health of their workforce, what companies can expect after joining our initiative, the value of PayPal’s example, and how leaders can best communicate their journey to workers and the public.

The following interview had been edited for length and clarity.

JUST Capital: What’s your elevator pitch to a CEO for joining the Worker Financial Wellness Initiative?

Jennifer Tescher: Your employees are one of your biggest expenses, they’re one of the most important inputs into a successful business, and the financial health of your workers is getting in the way of their performance. And, moreover, you’re not even sure whether the money you’re spending to support them with benefits, etc., is actually helping improve their financial lives or not.

What gets measured gets managed. And so starting to understand better the financial lives of your employees is going to help you be more strategic about how to effectively support them in a way that is good for them and good for your business.

JUST: What have your conversations with corporate executives been like recently? What are they looking for?

Tescher: Our history has been in financial services and we’ve expanded into broader workplaces over the last couple of years. What’s interesting and different about those two things is employers get it already. They already get that there is a challenge, particularly in the midst of the pandemic. If they weren’t thinking about the broader lives of their employees, they certainly had to in the face of the pandemic. “Are we going to make everyone work from home? Does everyone actually have a home?” And I’ve talked to executives where call center employees, a couple of them were homeless. That’s not going to work. And they had to address that.

I also think that right now financial wellness is very trendy in the workplace. There’s not a single RFP [request for proposal] that goes out from a company to vendors that doesn’t have on the checklist something around financial wellness, but most employers don’t fully understand what that means. In the vendor community, whether that’s plan sponsors, voluntary benefits providers, healthcare providers, they don’t really fully understand it either, particularly around retirement. Most of those folks are still thinking well, yeah, I have to provide advice about how to invest your retirement savings and provide a retirement calculator, but financial wellness is so much broader than that. And if people aren’t able to deal with their own day-to-day systems and needs, it’s a lot harder to plan for retirement and use those benefits effectively.

We’ve been working on both sides of the table, with employers who are being inundated with new tech startups and with their existing incumbent providers, all pushing new product, new platforms, new tools – it’s dizzying. They don’t know how to make sense of it. And on the other side of the house, we’ve been working with a whole range of different solutions providers to say your offerings need to be more holistic. They need to be more employee-centric. And they need to be based in the reality of people’s actual financial lives. Those are the conversations we tend to have with HR folks. I think HR folks in general know that their workforces are challenged and want to know what to do about it. And I think a lot of workforces, particularly the more progressive employers that are most drawn immediately to the initiative, in many cases they’ve already done a pay equity audit, or maybe they’re thinking about benefits a little bit but that’s as far as they’ve gotten.

The other thing I would say is in this moment of racial reckoning there’s a tremendous focus on racial equity in the workplace and the place that most often starts is around pay, but it’s so much bigger than that. If we don’t start to uncover the inequities in benefits usage, or in benefits plan design, or even understand the differential circumstances that people are facing, we really won’t close the gap.

The last thing I’ll say is a number of companies that we engage with believe that they have relatively well-paid, relatively white collar, middle-class and above employees – but they all have call centers. And I can tell you that one of the single biggest pain points for companies like that are their call centers employees. The other place where people have a pain point and may not even realize it is with all of the contractors they do business with, whether it’s their cleaning contractors, their security contractors – we haven’t even really begun to talk about what’s the responsibility that employers have for the people who are working for them through a contract company.

JUST: You mentioned how some companies you’ll work with have already done something like an audit, and further work might be appealing to them. What about companies where leaders would be much more focused upfront on how they will only want to do what will make more money for their business?

Tescher: We’ve got some research that really looks at the costs to the business of having a financially challenged workforce, and they’re pretty steep. The other thing that we know is what workers say they want out of a workforce and we know what’s actually happening – there’s a significant gap. Increasingly the quality of the job and the support that people get is is a big differentiator for talent. I often say you have to put your own oxygen mask on first. If you’re not treating your employees well on this front, it’s going to be hard for them to go and treat their customers well.

So, as an example, 78% of employees with high financial stress say it distracts them at work sometimes, often, or very often, and six in 10 workers would be more likely to stay at a job that offered financial wellness benefits.

So there’s a reduction in turnover. There’s a reduction in absenteeism.

I’ll give you some more top line findings. Currently less than one third of employees report having access to any given financial guidance benefit, even though a majority of employees express interest in these benefits. Emergency savings benefits from employers are still rare, with only 23% of employees indicating that they currently have access to an employer match for emergency savings. Yet that is the most in demand benefit of any that we polled on. Debt-related benefits are of interest to employees across the income spectrum. Even high income employees want support for managing their debt, but less than 20% of employees say that they have any access to that.

Then we also surveyed HR executives. A majority of employers consider themselves aware of the financial health challenges of their employees and are taking action to address those challenges. Employers are maintaining or increasing their investment in financial health benefits as a result of COVID, and think it’s a good time to be doing this.

Employer awareness of employee financial health challenges is largely based on limited metrics, contributing to this gap between employee needs and solutions. And so that gets back to this idea that they know there’s a problem. They know that they need to do more, but they don’t actually have the right information because most of the time, all they have is basic information about engagement, usage of benefits, or plan engagement. They don’t actually have anything that talks about outcomes.

JUST: If you work with a company to actually find this information, collecting it in the best way possible, what level of transparency do you then encourage in terms of what is shared with their workforce?

Tescher: We have an eight question survey, and employers can embed it in their existing engagement surveys. Lots of employers are regularly surveying their employees. If it’s going to be something that’s unique or separate, it will be particularly important to explain why they’re asking, and that it’s going to be used in an aggregated fashion, that they’re not looking at any individual employee but that it is about enabling them to make sure that they’re providing the things that workers need.

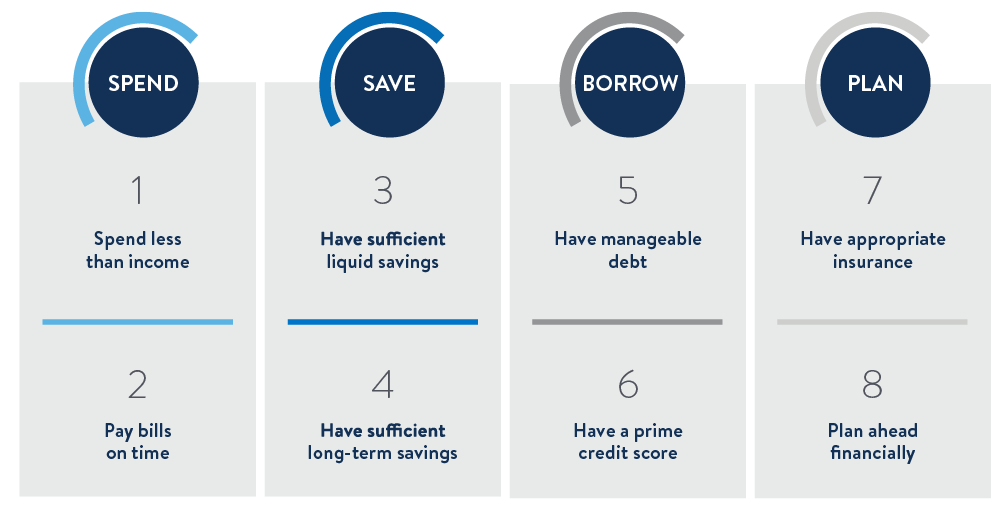

Eight indicators of financial health form the basis of the survey. (Financial Health Network)

We’ve built this platform that enables this end to end measurement, and there is a worker facing piece of it that tells them based on these eight questions, here’s how we think your financial health is, and here are some things you might want to think about, so that they at least get some benefit immediately.

But it’s also beneficial for companies to do this without sort of creeping out their employees. PayPal is a really great example of how to do it. You have to then show directly what action you’re actually taking. You ask questions because you’re committed to doing something. I think that’s really important.

JUST: There are plenty of situations where maybe a company’s already done an audit and they’ve communicated some degree of findings with employees, but they don’t want to go anywhere near releasing it to the public. What do you encourage there?

Tescher: Measuring the pay equity gap, whether it’s around gender or race or other characteristics, that’s been something that’s been encouraged for quite some number of years now, and there is increasing pressure for companies to be transparent about that publicly with their shareholders, and with all their stakeholders. This idea of a broader understanding of the financial health of of one’s workforce is newer, and there aren’t really even sufficient benchmarks. We have benchmarks about financial health nationally and regionally, but we don’t yet have enough benchmarks about what that looks like at a particular company, in different kinds of industries, or across peers – that’s where we’d like to go over time. As there’s more data available for benchmarking, then there’s an opportunity to start thinking about how and when to share that publicly, to create accountability.

Right now, there’s plenty of work that companies can do internally. PayPal CEO Dan Schulman has been terrific in speaking publicly about his experience, but remember he didn’t survey his employees, realize the situation, and then make an announcement. He went and took action, and he saw progress. Then he said, let me as a leader show you my whole process so that I can encourage the rest of you. Is there an opportunity to create opportunities to celebrate those companies who seem to be moving the needle most effectively on the financial health of their workforce? Absolutely. We’re still early days, though. So I think just getting companies to measure, and then to think about what it means and where they can do better is an important first step.

JUST: So OK, you have the information and then you’re ready to take action. That could require a significant investment made in the short term for long-term value creation. That could entail CEOs making these arguments for investments to their boards, and then communicating decisions to their investors, that look, this is going to be a big cost upfront, but this is something we have to do. How have you seen this play out?

Tescher: I don’t tend to see a lot of board pushback. Companies make decisions to invest all the time, it’s a question of where. We’re in an environment right now where these issues are top of mind. And certainly boards need to be prepared for the typical stock market response to an employee wage increase, which tends to take the stock down. But we’ve also seen that those tend to be short-lived negatives and they tend to bounce back pretty quickly, assuming the fundamentals are there. So from that perspective, yes, companies need to prepare themselves. But generally right now they’re getting lauded everywhere else for taking those kinds of actions. From a reputational perspective, if nothing else, it’s an incredibly positive thing to be doing right now.

And listen, companies need to create a roadmap for how they’re going to invest. They don’t have to do it all at one time, and many of them aren’t going to be able to afford to do it all at one time. That’s really important.

Increasingly, CEOs understand that they are responsible to numerous stakeholders and that the majority of their stakeholders are happy when they’re taking action to beef up their most important input into their products and services.

There is also an element of moral leadership here. You were asking like what’s a powerful way to make the case. Stories matter. And forget about investors for a minute. For the board to understand what it looks like for a call center employee, doing the math to show what that equates to in a year, laying out their various expenses, that’s really powerful. And I would like to think that most of us still have some humanity, some empathy in us. When you really understand what people’s lives are like, what their real financial lives are like, you can’t unsee that.

The government has a super important role to play in that, too. But employers definitely have a role to play.

JUST: Back to the Worker Financial Wellness Initiative specifically, if you’re speaking with a CEO or CHRO who’s interested, what else should they know before they sign on?

Tescher: They have to be committed to measuring on an ongoing basis and holding themselves accountable for the results. It’s great to take that first step of trying to really understand the lives of your employees. It’s another to then use that data to take action and then to measure again to see if it made a difference.

Can they hold themselves accountable for everything in their employees’ lives? Absolutely not. But it’s really important to set appropriate metrics that are within the control of the business and then make sure that you’re making progress over time. It’s what CEOs do in every other part of their business. Why should the way they manage their employees and the expense of their employees be any different?

JUST: So it’s really understanding that this is a long-term change. This is a way a new way of understanding your workforce. This isn’t just a one and done type of thing.

Tescher: That’s exactly right.