Alex Heath, Edelman’s U.S. Head of Social Impact & Sustainability, had a conversation with one of his firm’s clients recently that captured what CEOs and their leadership teams are struggling with across the country. And while he couldn’t share specific details of that discussion due to client privacy, its basics are familiar with anyone who has been even casually following business news for the past couple years.

This client personally cared about a social issue affecting the United States, and had to decide if they would speak to it on behalf of the company. After all, Edelman’s Trust Barometer found this year that business was the only trusted institution around the world, and as both Edelman and JUST Capital have found in their polling, majorities expect CEOs to respond to such issues writ large.

But, as the client explained to Heath, they ultimately decided to say nothing. “One, the company didn’t have a big reason to take a stand on it,” Heath told us. “And two, their workforce is politically polarized. It’s about 50-50. And so they knew that if they took a stance on this, which wasn’t totally material to their business, they would then alienate half of their employee base, perhaps. That’s not worth it.” The client did, however, decide to continue sharing data and updates on its sustainable supply chain initiatives because while they recognized the polarity of climate politics, sustainability was crucial to their company’s success, and they wanted their stakeholders to understand this.

For Heath, this was a healthy and wise approach to dealing with a term that’s been popular with the Davos set the past few months – ”greenhushing.” Related to its cousin “greenwashing,” which has long referred to the practice of using the guise of sustainability and “going green” as a marketing ploy and not actual policy affecting the practitioner’s business, it refers to the approach of staying mum publicly when it comes to any sustainability initiatives for fear of being labeled “woke” on the right and disingenuous on the left.

Regardless of whether “greenhushing” as a term is fleeting or here to stay, it refers to a problem that’s been front of mind for Heath because of how often it’s come up lately. A report from the climate NGO South Pole last fall found that among 1,200 global companies, “one in four businesses do not plan to talk about their science-aligned climate targets.” And, as Heath explained, in the same way that greenwashing came to casually be used to represent companies using deceptive practices for social issues in addition to environmental ones, greenhushing has applied to anything executives believe may be tied to the attack on what has been painted with a broad brush as ESG (environmental, social, governance).

Heath told JUST that he and Edelman are trying to prevent companies from giving into the temptation to drop all positioning that became the norm over the past few years, while also recognizing that this moment is the perfect time to bring focus to messaging that, in many instances, probably became too far-reaching for many companies. The most effective path, he said, is somewhere in the middle. “I think greenhushing can force a course correction in the space.”

He offered an alternative approach that he’s based on his many conversations with Edelman’s clients across American corporations.

Listen to your stakeholders and act accordingly

JUST identifies five stakeholders – workers, customers, communities, the environment, and shareholders. And while we ask the public how they prioritize them, we recognize that the stakeholder model (which Edelman aligns itself with, along with the Business Roundtable coalition of CEOs) means that all are linked; when, for example, a company is investing in its workforce or expanding sustainability policies, they should be in service to all other stakeholders, including investors.

Heath recognized that seeing where stakeholders stand on any given issue is difficult, and he also acknowledged the nuance that, for large public corporations especially, politicians are also stakeholders. For example, 17 states now have “anti-ESG” laws enacted or being considered, barring investments in companies they have deemed working for progressive political ideals at the cost of profits, and as we have seen repeatedly, this can lead to financial and PR disasters for companies like, famously, Disney in Florida. And that’s just the U.S.

But Heath also pointed out that in the same way JUST has found many stakeholder issues to be very popular among Americans, majorities around the world are reaching the same conclusions. “People are expecting business to take on climate, economic inequality, skills training, etc. That may be different in North Dakota versus Texas versus France versus Bangladesh – but broadly,” he said. “Not everyone can do everything, but everyone must do something – what’s right for you.”

Share why your actions are creating value – and stay focused on those issues

In 2020, a year marked by both the worst days of the COVID pandemic and the most passionate days of a racial equity movement, companies began scrambling to embed themselves in the zeitgeist, with mixed results.

“The last few years, companies saw that people wanted companies to act more on impact,” Heath said. “And so they jumped into these opportunities to communicate and engage audiences on impact without doing the hard work to build internally the policies, programs, and partnerships that they needed to actually stand up that impact. They wanted to rush to communication without actually building the work.”

In other words, customers and other stakeholders can see right through what boils down to marketing detached from either progress on the issue, or a policy that is wildly unrelated to a company’s purpose. And that’s how companies can alienate stakeholders regardless of their political ideology.

So actual work to purpose is critical before any posturing. But if you take the greenhushing route (again, using this in the casual application for environmental and social issues alike), “nobody will know about it, and you’ll lose out on trust. If you communicate without the action, then you’re rightfully at risk of being called out for greenwashing. And so the challenge is to a place where business is communicating commensurate with the action.”

Regularly and transparently communicate updates on progress

Heath guides his clients through the stakeholders model when guiding them. “What is good for their people? What is good for their supply chain? And how does that build multi-stakeholder value? And as you do that, rather than screaming from the mountaintops, ‘We are an ESG leader,’ it’s more about – and I think you’re starting to see this – it’s let’s talk about where we’re good, where we’re making progress, and be transparent about that work.”

He told us about another recent client discussion, in which this business leader explained the challenges their organization was facing around a project. The progress wasn’t ideal, and they were telling Heath that their business probably wasn’t going to release an update on where the project stands. That’s not the feedback Heath wants to hear!

“It’s about progress and not perfection,” he said. Edelman is especially focused on its corporate trust-building work, and has found that transparency – even around failures and setbacks – is better than ignoring problems for building trust among stakeholders. And there’s an added brand positioning benefit that comes with it.

“That requires a little bit more openness, and some companies are not willing to share their learnings or their failures, but others can learn from it,” Heath said. “You move forward and you move the space forward. You have a chance to actually lead.”

If your company wold like to learn more about how to put JUST Capital’s polling and corporate stakeholder performance insights into action, visit our company resources page.

This was a big year for JUST Capital when it comes to how we show up in the world and the impact we drive – arguably our biggest yet.

Two fundamental developments spurred that growth. As the United States began to mostly move on from COVID-19 pandemic restrictions, inflation simultaneously rose to a 40-year peak, the labor market remained tight, and companies had to determine new ways to recruit and retain talent. We also saw – with the combined forces of a war that upended energy markets, a midterm election, and a Securities and Exchange Commission with an ambitious agenda – ESG (environmental, social, governance) investing and the related stakeholder capitalism movement rise into mainstream political culture wars.

Both of these issues are, of course, incredibly complex, but we remained centered on the polling of the American public that defines our work. Our top articles, collected below, include the analysis, reports, Rankings, and interviews that positioned JUST Capital as the champion of pragmatic and popular business leadership.

1. JUST Capital and CNBC Release the 2022 Rankings of America’s Most JUST Companies

We kicked off the year with our biggest Rankings launch yet, with our new media partner CNBC. Alphabet took the No. 1 spot this year.

2. The 2022 Corporate Racial Equity Tracker

We checked in on how America’s largest companies are doing when it comes to their racial equity commitments of the past two years, with a more robust version of the Tracker we launched last year.

3. The Top Five Companies Leading on Paid Parental Leave in 2022

As the COVID recovery progressed, we took a look at the companies that offered a wide array of parental benefits, including six months of paid leave for two parents.

4. JUST Capital’s 2022 Workforce Equity and Mobility Ranking

With support from the Annie E. Casey Foundation, we identified the companies that are offering their employees not just good wages, but access to opportunities for growth in an inclusive way.

5. America’s Top 10 Companies for Environmental Performance in 2022

This year’s ESG debate was largely driven by the question of whether companies should be mandated to disclose environmental policy information, and to what degree. Regardless of how that plays out, these companies are already showing what’s possible.

6. How Companies Are Responding to Russia’s Invasion of Ukraine

When Russia invaded Ukraine in February, it threw the world’s political dynamics and economies into a frenzy. We quickly began tracking how the largest U.S. companies, many with business ties to Russia, responded.

7. The 2022 Top 100 U.S. Companies Supporting Healthy Families and Communities

With support from the Robert Wood Johnson Foundation, we ranked the companies that are having positive impacts on the communities in which they operate.

8. Just Over Half of the Largest U.S. Companies Share Workforce Diversity Data as Calls for Transparency from Investors and Regulators Grow

The SEC indicated last year that it would consider mandating enhanced reporting of human capital metrics as the largest institutional investors increasingly call for that information. We took a look at the state of play.

9. America’s 32 Industry Leaders for Environmental Performance in 2022

In honor of Earth Day, we showcased the companies leading their industries in transparent and ambitious climate policies and sustainable business practices.

10. Bank of America’s Head of Diversity & Inclusion Explains How Its Hiring and Retention Practices Prioritize Equity and Upward Mobility for Workers

Bank of America scored well on our 2022 Workforce Equity and Mobility Ranking (link above), and to discuss the policies behind that performance, we reached out to Cynthia Bowman, the bank’s head of DEI.

11. SURVEY ANALYSIS: Americans Want to See Greater Transparency on ESG Issues and View Federal Requirements as a Key Lever for Increasing Disclosure

At this point, a broad interpretation of what ESG means is now solidly part of America’s culture wars, but in February we found that large majorities of Americans support more transparency around how companies are impacting society, and even support federal reporting guidelines.

12. The 5 JUST 100 Companies Leading on Gender Board Diversity

Companies prioritizing gender equality do so at all levels of the organization, and we found that the average representation of women on Russell 1000 boards rose from 23.8% to 28.2% between 2019-2021. These are the JUST 100 corporations that stood out.

13. JPMorgan Chase’s Head of Corporate Responsibility Breaks Down 4 Lessons From Overseeing the Firm’s $2.5 Trillion Sustainability Initiative

We spoke with JPM’s Demetrios Marantis, who was put in charge of the bank’s highly ambitious $2.5 trillion sustainability initiative, and whose team has brought transparent updates on it into the firm’s annual ESG report.

14. In 2022, These 3 Companies Are Leading the Way for Women in the Workplace

As part of our partnership with CNBC, we determined the companies that excel on the women’s issues our polling found Americans value most, including access to childcare, equal pay, and paid family leave.

15. State Street Global Advisors’ CEO and Head of Asset Stewardship Talk Proxy Season, the State of Energy Amid Ukraine War, and the Future of ESG

State Street, as one of the Big Three institutional investors, holds significant influence over the fate of ESG investing, and we discussed SSGA’s “Value, not values” philosophy with then-CEO Cyrus Taraporevala and Benjamin Colton.

Each year, JUST Capital asks the American public about its views on the current state of business in the country, and which corporate issues matter most to them. This year, of a representative sample of over 3,000, 68% agreed with “Our current form of capitalism is not working for the average American,” up a full 10% from last year.

With that statistic in mind, along with the increasingly heated debate over ESG (environmental, social, governance) investing and stakeholder capitalism, our co-founder and chairman, Paul Tudor Jones, convened earlier this month a gathering of business leaders held at the Norton Museum of Art in West Palm Beach, Florida.

For the morning’s panel, Jones moderated a discussion with Alex Gorsky, former CEO and current chair of Johnson & Johnson, Andrea Jung, JUST board member and Grameen America CEO, and Thomas Peterffy, founder, former CEO, and current chair of Interactive Brokers. Gorsky sits on the boards of Apple, IBM, JPMorgan Chase, and New York Presbyterian Hospital, and Jung sits on the boards of Apple, Unilever, Rockefeller Capital Management, and Wayfair. Each brought a unique perspective: Gorsky helped lead the development of the Business Roundtable’s statement on the purpose of a corporation in 2019, shifting the CEO group’s stance away from shareholder primacy to an embrace of the stakeholder approach; Jung is dedicated to providing women entrepreneurs with capital and is especially concerned with matters of diversity, equity, and inclusion (DEI); and Peterffy, an ardent champion of free markets, filled the role of stakeholder capitalism skeptic.

But despite some disagreements over rhetoric, all endorsed the idea that a business’ stakeholders are inextricably linked. They also agreed that capitalism today in the United States was not serving regular people as much as it could be, and that the private sector played the primary role in addressing this. “How capitalism responds in this new period is going to be very important,” Gorsky said.

We’ve collected some key moments from the discussion below.

CEOs have a set of stakeholder obligations

Jones brought up the polling on Americans’ views on capitalism, noting that he feared the welcoming of socialism in the country, which he believes will weaken it. He added, however, that he still appreciates the intensifying debate as a means of encouraging progress. Gorsky responded by pointing to the common rebuttal to the stakeholder champions, who are often painted as focused on progressive policy goals disconnected from business. “I think the concept of obligations and responsibilities to shareholders is really important to balance that conversation,” he said.

Peterffy, who teased his fellow panelists by saying that the concept of stakeholder capitalism was “fake,” indirectly endorsed it. “Of course we have to take care of people, otherwise the company doesn’t get better,” he said, and then explained that if they don’t take care of their employees, then they will deliver worse service and products to their customers, and that in turn will hurt their shareholders. Peterffy may not be a fan of the stakeholder rhetoric, but he was echoing one of the theory’s pioneers, Ed Freeman. As Freeman explained to us last year, “Even if all you care about is making money for shareholders, how are you going to do it? You’re going to have great products and services for customers, suppliers who want to make you better, employees who want to be engaged in the company, and communities who want you or at least allow you to operate.”

The panel also brought up the way CEOs are increasingly expected to speak out on current events. In our 2022 Views on Business Survey, we found that a majority of respondents agreed that “CEOs of large companies do have a responsibility to take a stand on important societal issues” – but that was split 81% liberal, 75% moderate, and 44% conservative. “When I became the CEO of a public company at Avon in 1999, the environment was so different,” Jung said. But now, “the concept of a leader staying silent – and yes, it is extremely complicated – is impossible.”

Jung explained that as CEOs navigate this challenge, they need to determine which position is best aligned with a company’s purpose, thus serving its stakeholders.

Implementing ESG should be a careful balance of short- and long-term goals and actions

Peterffy’s son William started Interactive Broker’s ESG branch in 2019 and still chairs its ESG committee. And while Peterffy said he does not worry too much about endorsing or rejecting specific ESG metrics, he understands the appeal of ESG investing and believes “the environmental situation is a serious problem” and that investors and CEOs alike should be factoring in climate risk into their decisions.

Gorsky said that when considering these metrics, companies need to avoid ambitious goals set far into the future, which can be placating in the present but not proper North Stars. “Sometimes you’ve seen businesses confuse aspirational goals with realistic commitments that can be hit,” he said. He also made clear that he is wary of regulators creating “one size fits all” ESG metrics, given the sheer amount of variety across America’s public companies.

“It’s this balance, too, of short-term and long-term,” Jung said, noting that it wouldn’t require government legislation for a company to assess whether it is offering equal pay for the same job regardless of demographics and respond accordingly.

Workers are central

Jones brought up that JUST’s polling shows the public continually prioritizes worker issues, and that this year’s top issue across gender, race, age, and even political ideology is yet again that a company “Pays a fair, living wage.”

Jung endorsed the goal of the Worker Financial Wellness Initiative, which JUST cofounded with PayPal, the Good Jobs Institute, and Financial Health Network in 2020, saying that companies should undertake an assessment of whether their lowest paid workers are making a wage that allows them to provide for their families without struggling.

Peterffy took a broader stance, highlighting the word that kept coming up, “demand.” As he put it, “If they demand it, we’ll do it. I mean, we have to do everything to stay alive.”

“Look, I think COVID was a big wakeup call for businesses in this area,” Gorsky said, referring to the way the pandemic, along with the tight labor market in its recovery, shifted the power dynamic between labor and management. “Every board that we’re sitting on,” he said, referencing his fellow panelists, “has seen extraordinary pressure on wages.” Even during this challenging moment of inflation, with uncertainty of whether or not a recession is on the horizon, “you’re not going to be competitive unless you’re responding” to what both prospective and current workers are seeking.

You can watch the full panel discussion here:

JUST Capital’s polling of the American public and current policy debates continue to emphasize the importance of inflation and worker wages. We recently featured new data analysis showing low disclosure among the Russell 1000 companies on minimum wage rates and public minimum wage increase announcements resulting in real wage gains, and we also wrote a Fortune editorial dispelling the wage-price spiral myth and making the case that companies can unlock business value by regularly raising employee wages to match inflation.

This week, the Bureau of Labor Statistics reported that the headline CPI in November increased 7.1% year over year, and the core CPI – excluding food and energy – increased 6%. These were both lower than the figures for October and suggest that inflation is cooling, though price pressures remain throughout the economy. In turn, the Federal Reserve slowed the rate of increase in the federal funds rate to 0.5%, down from 0.75% in previous meetings.

Another highlight from this week is that even though real wages grew from October to November, they still declined year over year – they fell 1.9%, on average, despite nominal wage growth. However, some in the media continue to imply that workers’ nominal wage increases are the main driver of inflation and need to be reduced to lower inflation. This is despite empirical research from the International Monetary Fund showing that nominal wages can continue to increase while inflation declines, allowing real wages to eventually grow, and Federal Reserve Bank of San Francisco President Mary Daly saying last month there is no evidence of a wage-price spiral. In addition, household debt has reached multi-year highs, and the personal savings rate has dropped precipitously to its lowest since 2005.

Only time will tell if the Federal Reserve is able to achieve a “soft landing” or if it will push the economy into a recession. It is worth emphasizing, however, that even though inflation will likely decline further in 2023, it will remain above the Fed’s 2% target, which will continue to negatively impact family budgets if real wages continue to decline.

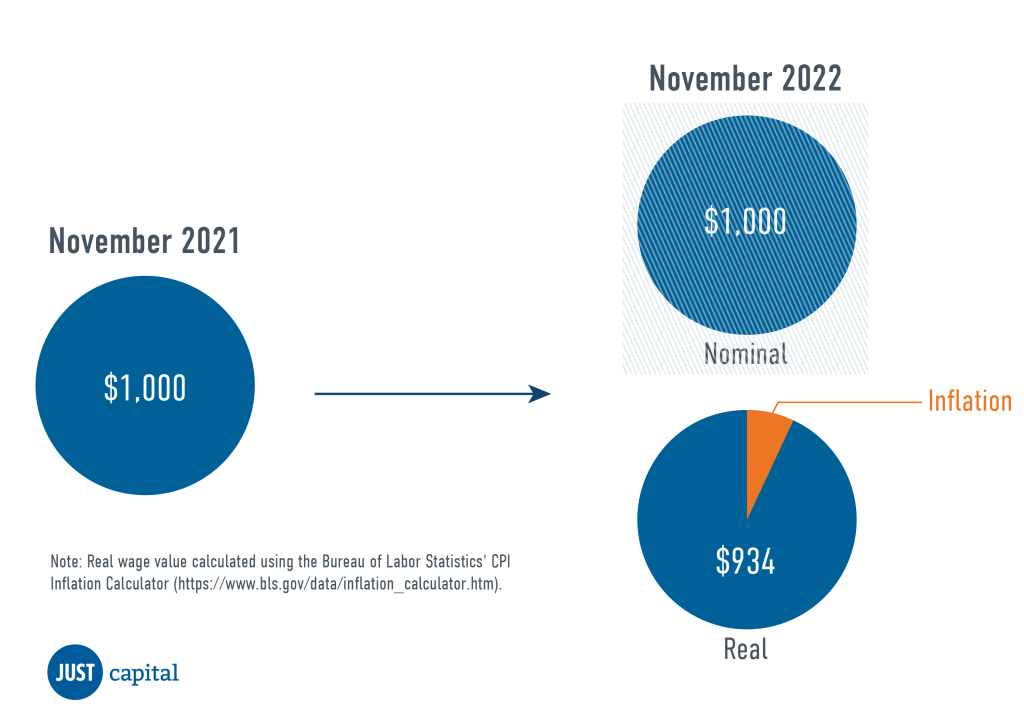

Within this context, to help investors, companies, and workers understand the relationship between inflation and wages, we are presenting three charts to concisely show how inflation reduces the purchasing power of wages and causes pay cuts for workers over time.

1. Inflation Reduces Purchasing Power

Imagine the following scenario. You have $1,000 in cash in November 2021. You don’t spend it, so you still have $1,000 in cash in November 2022. But because annual inflation was 7.1%, that money is really worth $934 in November 2021 dollars. $1,000 is the nominal value, and $934 is the real, and the real value is what matters for workers and companies.

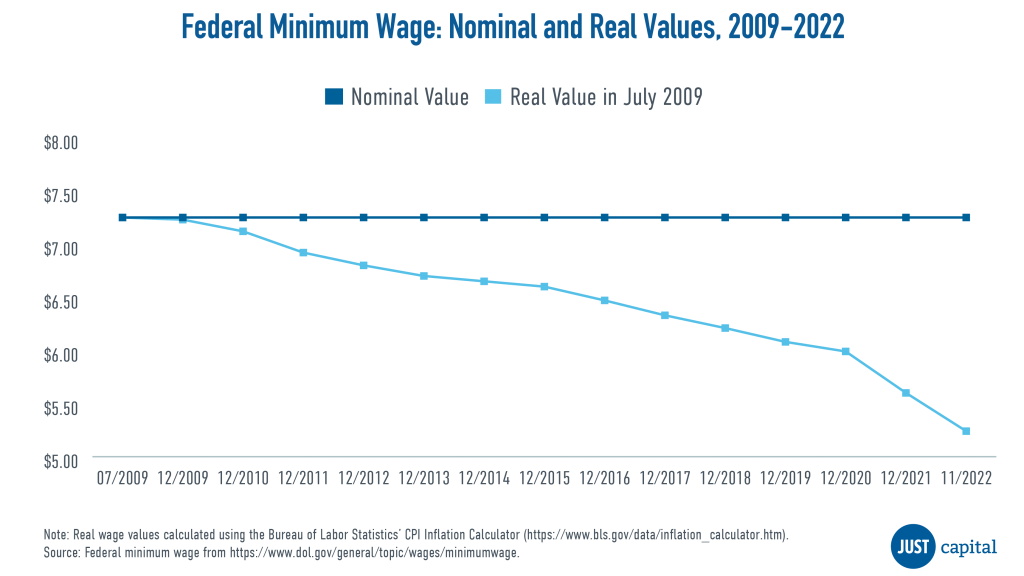

2. Without Wage Increases, Inflation Causes Pay Cuts for Workers

We can see how inflation affects wages by looking at nominal and real values over time. When wages are not increased, their real value, or purchasing power, declines. Because the federal minimum wage has not been raised since July 2009, when it was set at $7.25 per hour, its real value has dropped, and in November 2022 it had a purchasing power of $5.24 in July 2009 dollars. This means that a worker earning the federal minimum wage has effectively received a 28% pay cut over the past 13 years due to inflation.

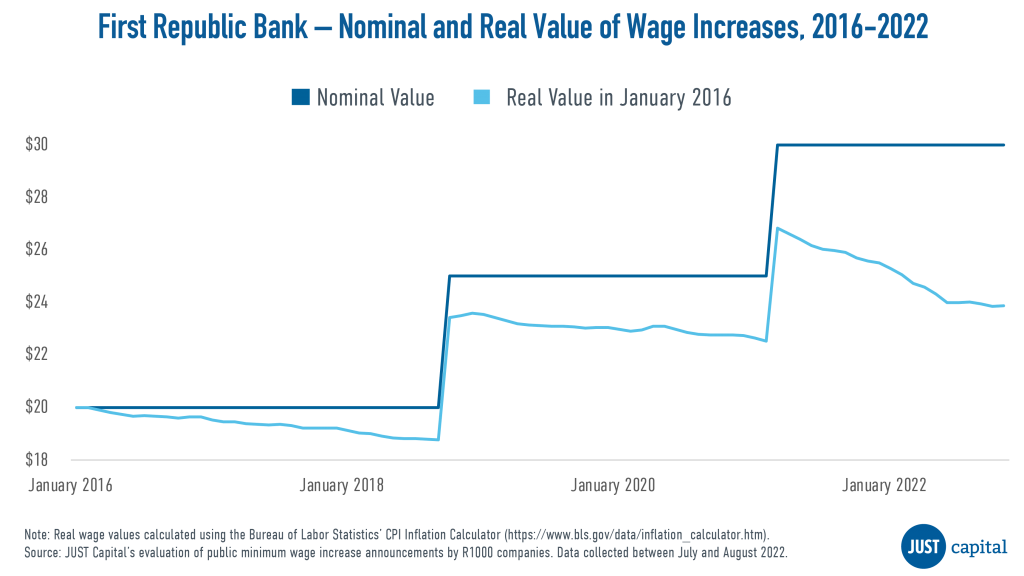

3. Even With Wage Increases, Inflation Causes Pay Cuts for Workers in the Period Between Each Increase

Even when wages are adjusted upwards by wage increases, inflation causes the real value of wages to decline in the periods between wage increases. First Republic Bank offers the highest publicly announced minimum wage rate among the R1000 companies at $30 per hour, and it has granted three wage increases since January 2016. But as can be seen, inflation causes a pay cut for workers in the periods between each increase, and the real value of wages is one of peaks and valleys due to inflation. In addition, that pay cut is amplified when the inflation rate is higher (i.e., compare the steepness of the curve from March 2021 to November 2022 compared to the previous two periods between wage increases when inflation was lower).

These charts show how inflation reduces the real value of wages over time. This hurts American workers, who effectively receive pay cuts, as well as American companies, which potentially face lower employee satisfaction, retention, and productivity. Regardless of how successful the Federal Reserve will be in achieving a “soft landing” in 2023, businesses can unlock value by understanding this relationship between inflation and wages and regularly raising employee wages to match inflation, benefitting workers, companies, and the U.S. economy at large.

As the ESG debate heats up among lawmakers, JUST Capital is showing how our data and research prove that “when companies manage their stakeholder relationships well, shareholders also benefit.” That’s how our Managing Director and Head of Investor Strategies, Cambria Allen-Ratzlaff, put it in her opening statement on Thursday in front of the U.S. House Committee on Financial Services Subcommittee on Investor Protection, Entrepreneurship, and Capital Markets.

The topic of the hearing was “E, S, G, and W: Examining Private Sector Disclosure of Workforce Management, Investment, and Diversity Data,” with the question of potential ESG and human capital disclosure standards via the Securities and Exchange Commission (SEC) the focus. Rep. Brad Sherman, D-Calif., led Democrats on the committee calling for a robust set of standards, and Rep. Bill Huizenga, R-Mich., led Republicans arguing that such standards would be SEC overreach.

Representing JUST Capital, Allen-Ratzlaff highlighted the data that shows that it remains quite difficult to capture the human capital metrics that Americans across all demographics, as well as major investors, are calling for, and in her capacity as Co-Chair of the Human Capital Metrics Coalition, she recommended four disclosures that would benefit shareholders. Using JUST’s research, Allen-Ratzlaff avoided the argument over what’s “woke” politicking by regulation rather than votes, and instead pointed to current challenges in gathering the data the public and investors alike are asking for.

Below, you’ll find a recording of the full hearing along with text of Allen-Ratzlaff’s opening statement. At the House subcommittee’s website, you can read and download JUST’s full written testimony, filled with intricate details supporting our position.

Testimony of Cambria Allen-Ratzlaff

Managing Director and Head of Investor Strategies, JUST Capital

Co-Chair, Human Capital Management Coalition

Chairman Sherman, Ranking Member Huizenga, and Members of the Subcommittee:

Good afternoon. My name is Cambria Allen-Ratzlaff, and I am pleased to appear before you today representing JUST Capital where I am Managing Director and Head of Investor Strategies. I also Co-Chair the Human Capital Management Coalition, a group of 37 large investors representing over $8 trillion in assets.

I have brief prepared remarks and respectfully request that the full text of my oral and written statements be entered into the public record.

JUST Capital is an independent, nonprofit research organization dedicated to measuring how America’s largest public companies create competitive value for their shareholders while serving their workers, customers, communities, and the environment. Our view is that when companies manage their stakeholder relationships well, shareholders also benefit.

Every year, we survey the American public to identify the business issues that matter most to them. We then use publicly available data to quantify performance of the Russell 1000 against those priorities. The vast majority of this data is hand-collected by our research team, taking 10,000 to 15,000 hours on average. Once we have reviewed the data and assessed company performance, we build our annual Rankings. We also leverage the data we collect to understand how performance translates into investment returns.

As researchers, our work goes where the voice of the American public takes us.

Since 2015, we’ve engaged more than 160,000 Americans representative of the U.S. adult population. And we have found that Americans are remarkably united in what they want companies to prioritize: workers, wages, and jobs. This holds across every single demographic group.

Paying a fair and living wage is the most important priority across all groups, followed by creating jobs at home. Americans are also primarily concerned about health and safety, and workforce mobility and training. So much so that collectively, worker issues make up 44% of our assessment model.

Our thesis is that companies that are better at managing their stakeholder relationships tend to generate more returns for their investors. We have consistently observed this to be true:

As U.S. public companies are born from, and an integral part of, American society, it is perhaps unsurprising that what is good for workers is good for investors. Our reporting system, however, has been slow to adapt.

Consider this: The only line-item data U.S. public companies are required to disclose on their workforce is headcount. This reporting standard was set in 1973, when over 80% of the S&P 500’s market cap was property, plant, and equipment. Fast forward 50 years to today, and 90% of the S&P 500 is based on intangible assets. It’s human capital – the collective knowledge, skills, and experiences of the workforce – powering economic growth.

But as our financial reporting standards have lagged, this also means that up to 90% of company value may not be reflected in companies’ disclosed financials. And investors have taken note.

Speaking on behalf of the Human Capital Management Coalition, the Coalition has urged financial and accounting standard-setters to improve access to workforce data through a balanced approach, where principles-based disclosures are anchored by four foundational, decision-useful disclosures that apply to all companies. They are: (1) the number of full time, part-time and contingent or contracted labor directly involved in firm operations; (2) labor costs; (3) turnover; and (4) workforce diversity data sufficient to understand the company’s efforts to access and develop new sources of talent, as well as how effective these efforts are.

Without this information, investors are flying blind, unable to understand how well a company manages its workforce, and how it impacts a company’s overall business, risks and prospects, to most efficiently direct their financial capital to its highest-value use.

Today, even attempting to get this information is excessively time-consuming. When JUST Capital assessed workforce disclosure at the 100 largest U.S. employers, it took a team of two skilled data scientists over 130 hours to collect data on a discreet number of human capital metrics – or find the data completely unavailable.

If a sophisticated research organization like JUST Capital, or large, global institutions with billions of dollars in capital are unable to access decision-useful, comparable, consistent, and reliable workforce data, small retail investors are at even more of a disadvantage. And, according to JUST Capital’s polling, 85% of Americans across political affiliations agree that companies should disclose more about their business practices and impact on society.

Companies meeting the needs and expectations of the American public have proven them to be value-relevant through their performance. Simply put, companies that are best at harnessing the awesome power of their workforces are also best-positioned to generate long-term value for shareholders.

Thank you, and I look forward to your questions.

Inflation, a potential recession on the horizon, the lingering effects of a pandemic, a war with global impact, and bitterly divisive politics – it can be easy to be pessimistic about the direction of the United States. But Steve Case won’t indulge that.

For the past eight years, the AOL cofounder and founding CEO of the venture capital firm Revolution has been touring the United States in a big, bright bus, for the “Rise of the Rest” initiative, which shares its name with Case’s new book. The book is an exploration of his vision for an America boosted by startup economies tied to their communities – namely the ones not in Silicon Valley, New York City, or Boston, where 75% of venture capital in the U.S. goes. And it’s an expression of optimism that can feel exceedingly rare these days, but is one complementary to what we’ve found at JUST.

In the same way that we have found through our polling research that Americans across all the demographics we track agree that worker issues, especially providing a living wage, should be the number-one priority of American businesses, Case is driven by the idea that people across the country ultimately want the chance at a fulfilling career regardless of where they live. And, he says, we’re at the beginning of an era in technology that can help make this happen. Case believes that AOL represented the First Wave of the internet, followed by social media marking the Second Wave, and now we’re at the forefront of the Third Wave, where “internet of things” becomes the internet of everything and opens up transformative opportunities across all industries.

So far, Case and his team have been to 43 cities across the country and made 200 investments through two $150 million funds. They made eight bus tours before COVID forced them to temporarily go virtual, leading to one virtual tour focused on Black founders and another connecting talent from the coasts to opportunities at startups beyond the three primary hubs.

The new book is the next step in introducing his mission to a wider audience. We recently spoke with Case about what he wants to accomplish with it, and explored the overlap of Rise of the Rest with JUST’s own work.

The following transcript has been edited for length and clarity.

How has your perspective on Rise of the Rest – the fund, the tour, the idea – evolved over time?

We’ve seen steady progress each year in terms of interest in these cities, new companies starting and scaling, big exits that get attention, people shifting where they’re living, and people starting to think about investing in other places.

It was steady progress and then COVID has been a tipping point on multiple levels. For some people it was a moment to take a step back and rethink how and where you want to live, and how and where you want to work.

We stressed even when we got started that one of the things we needed to do was shift the talent discussion from being about bemoaning a “brain drain” of people leaving to celebrating a boomerang of people returning. So the pandemic has been helpful on that front.

It’s also been helpful on the venture investing side. Investors who were intrigued with some of what’s happening in rising cities but not necessarily intrigued enough to jump on a plane could now jump on Zoom and then talk to people in those cities. That led to a lot of pitch meetings on Zoom.

On the policy side of things, at the state and local level, a lot more governors and mayors are focusing on startups, and at the federal level, there’s been legislation passed like the Inflation Reduction Act and the CHIPS and Science Act, which includes authorization for investment in regional hubs.

A few weeks ago President Biden was in Columbus talking about regional entrepreneurship at the Intel plant. And then Treasury Secretary Yellen was talking about the idea of leveling the playing field and creating more opportunity for more people and places. So they’re mostly in sync with the arguments we’ve been making.

I’d say that it went from steady progress to an acceleration, which I think bodes well for the next chapter.

It sounds like there was, maybe this is the wrong phrase for it, but a silver lining of the pandemic.

It was such a terrible pandemic and I’d hate to say, “But oh, isn’t this great!” But yes, it was a silver lining, if you are looking for something positive in a difficult two-and-a-half years.

You included in the book some numbers that appear to be backing the Rise of the Rest thesis, in terms of where the money is starting to flow.

You’re referencing the Beyond Silicon Valley report we did with Pitchbook. There’s one data point particularly that was of surprise even to me, which is that in the last decade there have been 1,400 new regional venture firms outside of San Francisco, New York, and Boston. So basically you’ve got our Rise of the Rest footprint.

That’s super interesting and super encouraging because we’ve long said that the entrepreneurs in most parts of the country need more access to that initial capital as a seed stage, and having capital available locally is really important.

Business and community are inextricably linked

With a lot of the companies you highlight from the Rise of the Rest portfolio, it seems like these startups are baking in purpose-driven values and stakeholder issues JUST tracks for corporations. Are you seeing that?

A lot of these Rise of the Rest entrepreneurs are passionate about fixing or addressing some problem in society and opt to do that through the prism of starting a company. That leads to companies like AppHarvest in Kentucky with sustainable agriculture or TemperPack in Richmond, Virginia with sustainable packaging, and I could give you a couple of dozen others.

They are also quite intentional about how their companies also can lift up their community. For example, Jonathan Webb of AppHarvest was deliberately focusing on this and had a strategic reason to do it. Eastern Kentucky, outside of Lexington, is within a 24-hour drive of 70% of the U.S. population. But Jonathan also had a desire to create jobs and bring opportunity to coal country Appalachia, which for several decades had been struggling. So there was that broader societal impact.

On the DEI side, many of these cities are diverse, and we have been intentional about diversity for building our own team and backing entrepreneurs. Right now the Rise of the Rest portfolio, which is about 200 companies, is 41-42% female founders or founders of color, which is still not what it should be, but a lot better than you see in most venture firms.

The corporate and startup worlds of are often linked in ecosystems. One of the examples that you point to is Atlanta, where you have corporations like Delta, Home Depot, and UPS actively engaging their communities, including entrepreneurs there. Why should corporate leaders be paying attention to Rise of the Rest, regardless of where they are in the country?

Because their own success could be accentuated by focusing on Rise of the Rest. If they’re staying close to entrepreneurs who are doing innovative, disruptive things, they’re more likely to see the future as opposed to being overwhelmed by it, and might, if they’re agile, actually be able to partner with or, in some cases, acquire some of these companies to strengthen their competitive position.

Second, every company is ultimately about its people, and part of what JUST has done is highlight that and the benefits of investing and properly rewarding people. How do you attract great people who want to work at your company? Part of that is attracting people that want to live in your community.

Personally I remember my own experience in Cincinnati, where my first job out of college was at Procter & Gamble. At the time there were a few big companies there, but there were really no startups. The downtown area was occupied nine-to-five, was basically dead on evenings and weekends, and there wasn’t a real vibrancy to it. Some of the big companies eventually noticed that, too, and they got together and funded some programs like Cintrifuse, the Hatchery, and others to basically create a more fertile environment for startups. That paid off, and the city is now more interesting to live and work in. It makes it easier for those big companies to attract and keep the people they want to take their companies to the next level.

What Dan Gilbert’s done in Detroit comes to mind.

That’s obviously a great example. I’ll be there on Monday. He helped get the Forbes 30 Under 30 Summit to Detroit, and that’s exact thing we’re talking about. Dan made an effort to get more young people to understand what Detroit is now, with the idea that some people visiting for a conference would see it and some of them would end up deciding to move to Detroit. That’s happened. So it’s an example of this idea of trying to use your position as a corporate leader to have a broader impact in the community.

A mission to unite behind

You’ve got access to a lot of politicians and big influential players across the political spectrum. You’ve been all over the country, talked to people from every corner of America. Given your perspective and optimism, what are you seeing that could better unite the country when it’s so divided?

Well, part of the reason why I wrote the book is I think it’s an optimistic story of an America that’s not something that most people are aware of. There are a lot of things that are negative with inflation, Ukraine, the pandemic, all kind of things. But there’s a more positive, inspirational story that’s not just about certain people or certain places. I felt there’s a reason to be more hopeful, but we have to continue to build on some of the initial foundational efforts over the last decade.

I start and end the book with the idea that it’s not our God-given right as a country to remain the most innovative, entrepreneurial nation in the world. We can’t be complacent about that. We’ve got to lean into the future and I don’t think we can do that successfully if we’re only putting our eggs in a few baskets like Silicon Valley, New York, and Boston. We need to have a more diversified and decentralized approach to innovation.

But my hope is that this book will lead everybody in America to maybe feel a little bit better about our country’s potential future.

So this is based on the idea of economic opportunity for Americans regardless of where they are in the country, whether they want to create something or even just work within their own community with a good paying job?

Yes, one of the big problems is the opportunity gap where some people in some places are doing really well, and a lot of people in a lot of places are struggling and feeling left behind because they have been.

So the idea is that fertile startup ecosystems in more places brings more capital, which creates more jobs, which drives more economic growth, and which will then create more opportunity and more reasons for people to be more optimistic about the future. I think it’s critical that we do that if we are going to have a country that continues to lead the world. Now is the time to get it done.

I think it’s safe to say, then, that you’re bullish in America.

I believe in America! I believe in America, as long as we’re celebrating the next generation of entrepreneurs, how we’re doing it everywhere, not just in a few places.