Walmart

This week, JUST convened a virtual gathering of current and former corporate leaders to explore, in part, our Worker Financial Wellness Initiative.

While the discussion was under the Chatham House Rule, I can share some of the biggest takeaways from this highly impressive group, which are that CEOs must be courageous enough to take a short-term hit in order to create value for stakeholders in the long term, and that investing in the financial security and overall well-being of workers is perhaps the single most critical investment a company can make right now.

As you can read in my latest Forbes article, Walmart has seen both sides of the stakeholder vs shareholder debate over the last seven days, losing $25 billion off its market cap after a mixed earnings call. What made Wall Street especially upset was CEO Doug McMillon’s announcement of a $14 billion investment in operations – which included raises for 425,000 of its associates, from $13 to $19 per hour, depending on location and market. Costco, which followed suit yesterday by announcing it was lifting its hourly minimum wage to $16 per hour, saw similar short term stock declines.

Since becoming CEO in 2014, McMillon has been laser focused on keeping Walmart competitive with its rivals – notably Amazon, Target, Costco – in a rapidly changing retail landscape. Having the courage to invest in their workforce is a key part of this. When he raised wages for 1.2 million workers in 2016, the stock took a hit then too. It took two days to recover, and six months later was up 23%.

The key point is this: Building value for investors – and for all stakeholders – takes time, but the rewards for shareholders and society at large are much greater. CEOs need our support when they are punished in the short-term for their foresight.

Be well,

Martin

Aetna, UPS, Starbucks, UPS, and Whole Foods showcased as companies that offer health insurance to part-time employees.

150 CEOs, including those of BlackRock, Google, Goldman Sachs, and Intel, signed a letter urging Congress to pass President Biden’s $1.9 trillion coronavirus bill over Republican objections.

Costco will raise its starting wage to $16 an hour, officially paying higher than their competitors at Amazon, Best Buy, or Target.

Glassdoor launches a new product feature that reveals employee provided company ratings and salary reports broken out by specific demographic groups, specifically, salary data is broken out by gender identity and race/ethnicity.

JPMorgan Chase announces new investments as part of its $30 billion commitment to lift up Black and brown communities, including $350 million to support underserved small businesses, a $42.5 million to a “Entrepreneurs of Color Fund,” and new “lounges” serving entrepreneurs.

Nielsen announces that they will begin tracking diversity and inclusion on TV.

Walmart backed a McKinsey study – Race in the Workplace: The Black Experience – examining racial inequity in the private sector, particularly in higher-wage, higher-growth industries.

Throughout the coronavirus pandemic, companies faced new challenges in maintaining employee well-being. We teamed up with AARP to create a set of guides focused on three critical issues – paid sick leave, dependent care, and work from home – to help explain the current state of play, best practices, as well as benefits to employers and employees for implementing expanded programs. We hope they are a helpful resource.

A Corporate Guide to Dependent Care: By creating sustainable dependent care options for both eldercare and childcare, companies can greatly improve quality of life for their employees and their families and see significant savings and reduced turnover.

A Corporate Guide to Paid Sick Leave: By implementing paid sick leave policies, companies are not only protecting their workers’ health and financial security, but also the health of customers, communities, and their supply chain.

A Corporate Guide to Working From Home: By creating greater flexibility and better work-life balance, companies can reduce costs and turnover, and increase productivity and happiness.

JUST’s Yusuf George highlights nine Black women who are championing stakeholder capitalism across America’s largest companies, including Rosalind Brewer and Thasunda Brown Duckett, who will be the only two Black women CEOs of Fortune 500 companies.

The Reimagining Capitalism newsletter on LinkedIn featured a sit down with Martin exploring ideas for designing a more fair, inclusive, and sustainable capitalism. Explore other great interviews here.

Jennifer Tescher of the Financial Health Network invited JUST Board Member and National Urban League president Marc Morial onto her “Emerge Everywhere” podcast to discuss Economic Justice for All.

JUST Board member Arianna Huffington penned a byline in Thrive talking about new S.E.C. guidelines on human capital reporting, demonstrating a growing recognition of employee well-being as a key driver of business performance.

“Addressing stark disparities in income and wealth doesn’t just benefit Black families and marginalized populations. It benefits our neighborhoods and our entire economy. It is our collective responsibility to address this challenge and break down structural barriers to opportunity.”

“Thinking about employees shouldn’t be a function of human resources – it’s a competitive differentiator, and it’s needed now more than ever. …By advocating for internal safety measures, effective policy, and racial equity, companies can put purpose-driven leadership into practice to protect their workers and fuel an inclusive recovery.”

“I want to note this isn’t altruism. At Costco we know that paying employees good wages … makes sense for our business and constitutes a significant competitive advantage for us. It helps us in the long run by minimizing turnover and maximizing employee productivity.”

A Financial Times opinion piece explains why businesses should not be afraid of the calls to raise the minimum wage: “Almost all Americans, whether they live in Texas or California, admit that it is impossible to live on $7.25 an hour.”

In their State of Working America 2020 wages report the Economic Policy Institute shows that wages grew historically fast in the last year because the bottom fell out of the low-wage labor market: “Wages grew largely because more than 80% of the 9.6 million net jobs lost in 2020 were jobs held by wage earners in the bottom 25% of the wage distribution. The exit of 7.9 million low-wage workers from the workforce, coupled with the addition of 1.5 million jobs in the top half of the wage distribution, skewed average wages upward.”

The challenges of child care is getting the attention it deserves with an in-depth feature in The Lily explaining that a full economic recovery will only be possible if we invest heavily in our nation’s patchwork dependent care systems. Also a new report from the think tank Third Wayexplains that the costs of child care centers have gone up nearly 50% since the onset of the pandemic and that lack of child care is now the third-most cited reason for not working, behind layoffs and furloughs. CBS reports that the Marshall Plan for Moms is picking up steam in Washington.

Meanwhile, The New York Times believes that, no matter what, an economic boom lies at the end of the pandemic.

The Stagwell Group hosted a webinar featuring some of the most interesting findings from The Harris Poll’s survey work on CEO reputation. One of the most interesting insights? Ethical standards are the highest valued quality in a CEO.

This week, we look at Morningstar’s most recent analysis from Jackie Cook, diving into the C-suite Gender Pay Gap analysis that explores pay data of corporations’ named executive officers (NEOs).

Each year, we survey the American public to learn their views on business today, and we’ve learned that Americans consistently agree – year after year – that the top priority for companies should be their workers. And the public doesn’t necessarily distinguish between different types of workers – whether full-time, part-time, or contracted – showing that temporary, contract, and vendor (TVC) workers should be prioritized alongside a company’s permanent workforce.

Since 2018, JUST Capital has been working to better understand how companies think about their TVC workforces – and we’ve found that corporate leaders continue to grapple with key questions around these workers. Concretely: are TVC workforces a risk to be managed, or a potential asset that hasn’t been properly explored?

Over the last year, the impacts of COVID-19 have accelerated these questions – with companies asked to carefully consider how to support their contract workforces through the pandemic, and with the world of work writ-large on the cusp of transformation, as companies grapple with whether and how to reopen their workplaces and what a return to “normal” might look like for their employees. With TVC workers an increasingly urgent topic for corporate America, we recently sat down with Teresa Huston, Vice President and Deputy General Counsel at Microsoft, and Tauseef Rahman, Partner at Mercer, to explore their work on these issues.

At the start of the pandemic, #1 Most JUST company Microsoft committed to continue paying its contractor workers – many of whom work on-site at the company’s campus in Seattle – and the company continues to compensate these employees today. Huston explained Microsoft’s journey to this decision, which began long before the pandemic with a path that included a seminal lawsuit and now has led to Microsoft extending key benefits to its temporary employees. “We learned some pretty hard lessons from that case,” Huston shared – and in the years since, Microsoft has become a pioneer on these issues, requiring its vendors to offer paid sick leave and paid parental leave to their workers. With these foundations in place, Microsoft’s choice to continue paying its TVC workforce was a natural next step, and served once more as a model for how corporate leadership can and should support these employees.

Mercer – a consulting firm whose mission serves, in part, to help companies redefine the world of work – often explores the issues of TVC workforces in conversation with its clients. In March of 2020, Mercer learned that about ⅔ of companies say they employ contractors – but also found that the majority did not provide compensation during the pandemic. Rahman explained that the nature of contract work holds significant risk for TVC workers, particularly during more challenging times, but emphasized that this moment represents a significant opportunity to ask “Are there different ways to work for a company?”

Key takeaways are emerging from our conversations with companies – including Microsoft and Mercer – about how corporate leaders should consider their TVC workforces, as we continue to talk about building a more resilient economy in the future:

In recent years, more and more contract workers have become core to companies’ operations – sitting alongside their permanent counterparts as colleagues and taking part in work that is central to their company’s operation and mission. With Americans expecting companies to prioritize their workers, corporate leaders must consider how they support not just their employees, but the contract workers who share space with them and contribute considerably to their collaborative work. Huston emphasized that, while the unique legal and contractual considerations of contract workers can’t be ignored, corporate America needs to move away from the mindset that contractors are “a risk to be managed” and toward a more integrated understanding of how TVC workers contribute to the resiliency of their business, shape the experiences of the permanent workforce, and advance the company’s mission through their efforts.

Before we can truly consider what might need to change for America’s contract workforce, we need to understand the current state of play for these workers. Human capital disclosure – particularly around demographic issues – is becoming increasingly important across corporate America, but TVC workforces present unique challenges when it comes to disclosure and transparency. With many contract workers employed through vendors, Huston emphasized that there are different legal considerations at play – in regards to both the demographics of these workers and even what kinds of jobs they hold – when asking companies to share details on their contract workforce. Furthermore, Rahman shared that contract hiring and human capital issues might not even be centralized with HR departments, making it difficult to collect information about these workers and factor them into strategic workforce planning. In the coming years, a core question for corporate America must be around how we build a clear and consistent portrait of our nation’s – and each company’s – contract workers – so that we might better understand what is working and what is not.

Over the years, our research has shown that treating workers well not only benefits a company’s employees but its bottom line. Understanding, again, that contract and permanent employees are part of the same workforce, the unique challenges faced by TVC workers can negatively impact their own productivity as well as the productivity of their permanent colleagues – and the challenges of retention and retraining contract workers can significantly slow or hamper a company’s operations. Huston emphasized that, for Microsoft, “Making decisions to be responsible and aware has been good for our business,” a guiding principle that led them to set specific contract standards for their TVC workers – like paid sick leave and parental leave – that allow these employees to be more present and effective members of Microsoft’s overall workforce and to contribute more significantly to the company’s growth.

As we look ahead to the reopening of businesses across corporate America, the question of how contract workers are supported today can profoundly impact our eventual return to work. Most tangibly, there are key questions of occupational health and safety – if paid sick leave is not available to contract workers, the risks of outbreak are potentially greater, and the ways that contract and permanent employees share space can impact critical health concerns. But there are also important questions about operational resiliency – if an entire contract workforce has been laid off, corporate leaders face significant challenges to resuming normal operations and scaling back up, needing to rehire and retrain workers across many areas of their business. Finally, it’s critical for companies to recognize how decisions around their contract workforces can have tremendous impact on their communities. Huston shared that, for Microsoft, a major way that the company contributes to its community is by providing jobs to the people who live there. “We really are responsible for how our region emerges from this catastrophic event,” she emphasized – suggesting that support for contract workers shapes not only the future of our nation’s businesses, but the future of our nation’s communities.

Embedded within this question of how we rebuild following the pandemic is the consideration of what the future of work writ-large might look like. Rahman hypothesized that our “full-time-or-bust” mentality might become a thing of the past, as more employees core to companies’ operations are employed on a contract basis and we begin to more deeply question whether there are different ways to work for a company. And questions of flexibility and types of employment are relevant not just to lower-wage, lower-skill work, but must be central in how we think about all our nation’s workers. This moment represents an opportunity for companies to consider, coming out of the pandemic, what groundwork they might lay now to ensure that their full supply chain is resilient and connected to the operations and purpose of the broader company.

Corporate leaders are increasingly seen as societal leaders, responsible for what’s happening not only within their own organizations but within their communities and the world of work writ-large. It’s clear, and becoming clearer, that these issues are not limited to the on-demand economy or to lower-skilled workers, but to TVC employees across industries and the wage ladder who have become deeply integrated in their company’s core operations. In our ongoing conversations with C-suite leaders – focusing on issues like worker financial well-being and racial equity – we will continue to apply this lens of consideration, asking how a company’s TVC workforce must shape strategic decisions around these issues, as well as the future of work overall. There’s a real question about mindset-shift on this issue, where leaders must begin to ask and understand their contract workers. In the meantime, we will continue to contend with the fragmentation of America’s workforce, and the implications that fragmentation has for our nation’s businesses, the communities in which they operate, and the world of work overall.

Explore more of JUST Capital’s work on the TVC workforce here, and watch the full conversation with Microsoft and Mercer below:

Events over the last year have tested the country’s frayed social fabric like no other year in recent memory. Growing partisan polarization has been well-documented, and partisan antipathy has intensified to a point where 91% of Americans say that they see strong conflicts between Democrats and Republicans. Everything, from the COVID-19 pandemic to presidential approval ratings, shows widening gaps in attitudes between Americans of different political views. It seems that the only thing that the American public – across all ideological factions – can agree on is that Democrats and Republicans disagree on even basic facts.

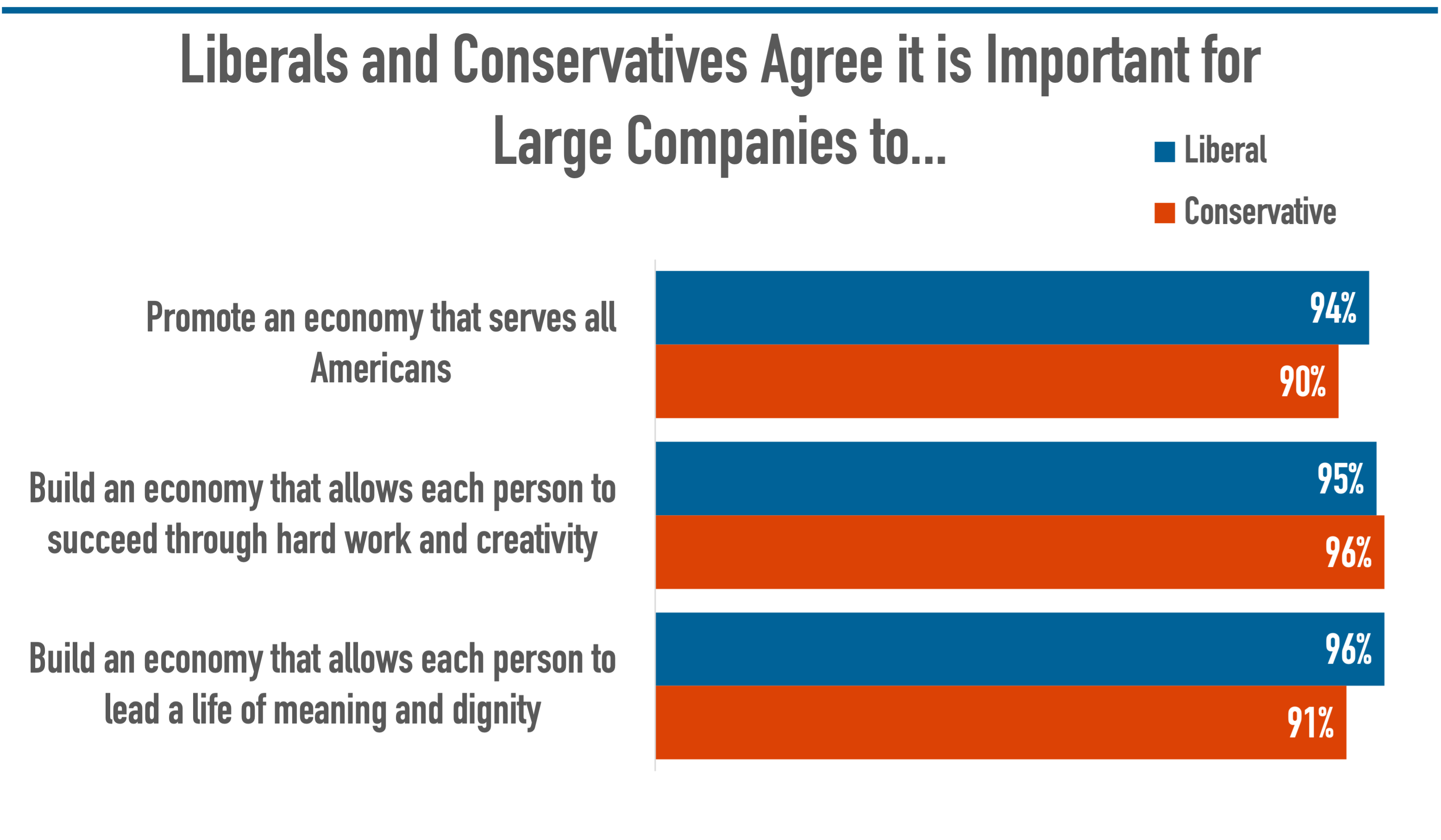

Our annual survey, however, has captured a common ground among liberal and conservative respondents when it comes to their views on stakeholder capitalism, with large majorities of each group agreeing that it’s important for companies to promote an economy that serves all Americans, as well as one that builds an economy that allows each person to succeed through hard work and creativity and to lead a life of meaning and dignity. And both groups largely agree that business can be a force for positive societal change (88% of liberals and 74% of conservatives).

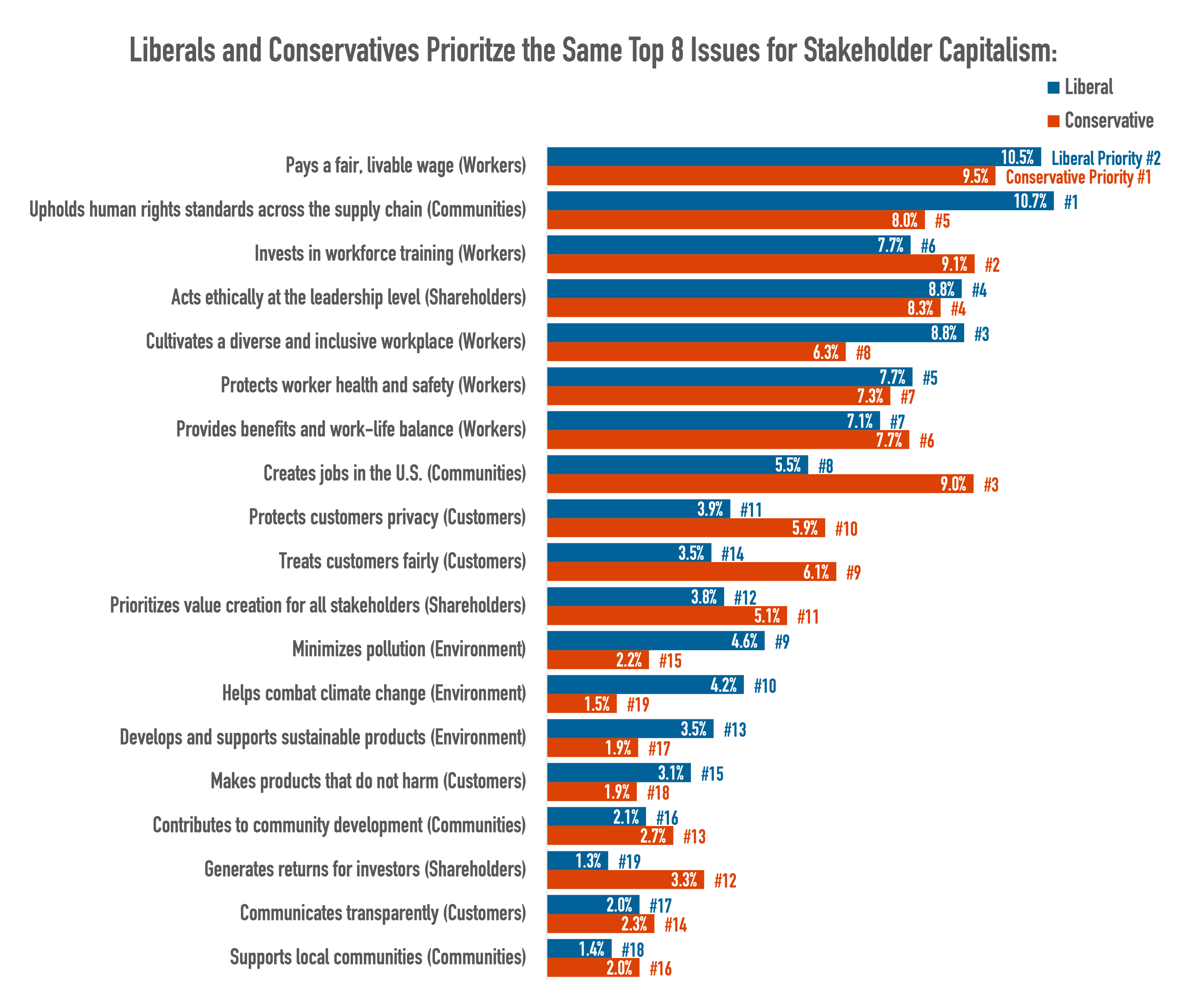

Across ideological divides, Americans also agree on what the top eight priorities for creating this vision of stakeholder capitalism should be – among them, paying a living wage, cultivating an inclusive workplace, and protecting workplace health and safety. This alignment signals that stakeholder capitalism may represent a broad-based solution for achieving a more equitable economy that all Americans, regardless of their ideological perspectives, can get behind – in particular, when it comes to how companies treat their workers.

Overall, Americans want to see companies pay a fair, livable wage to their workers – it is the top priority for conservatives and #2 for liberals (securing human rights across the supply chain is the top priority for liberals). Ethical leadership ranks #4 for both groups on the list of priorities. And among the top eight priorities overall, liberals put slightly more emphasis on issues of human rights and workplace diversity compared to conservatives, while conservatives put slightly more emphasis on job creation and workforce investment compared to liberals.

Further down the list of priorities, some predictable differences emerge. Liberals are more concerned about environmental issues compared to conservatives, such as limiting pollution (#9 for liberals and #15 for conservatives) and reducing carbon emissions (#10 for liberals and #19 for conservatives). Conservatives put a higher priority on generating profits (#12 for conservatives and #19 for liberals).

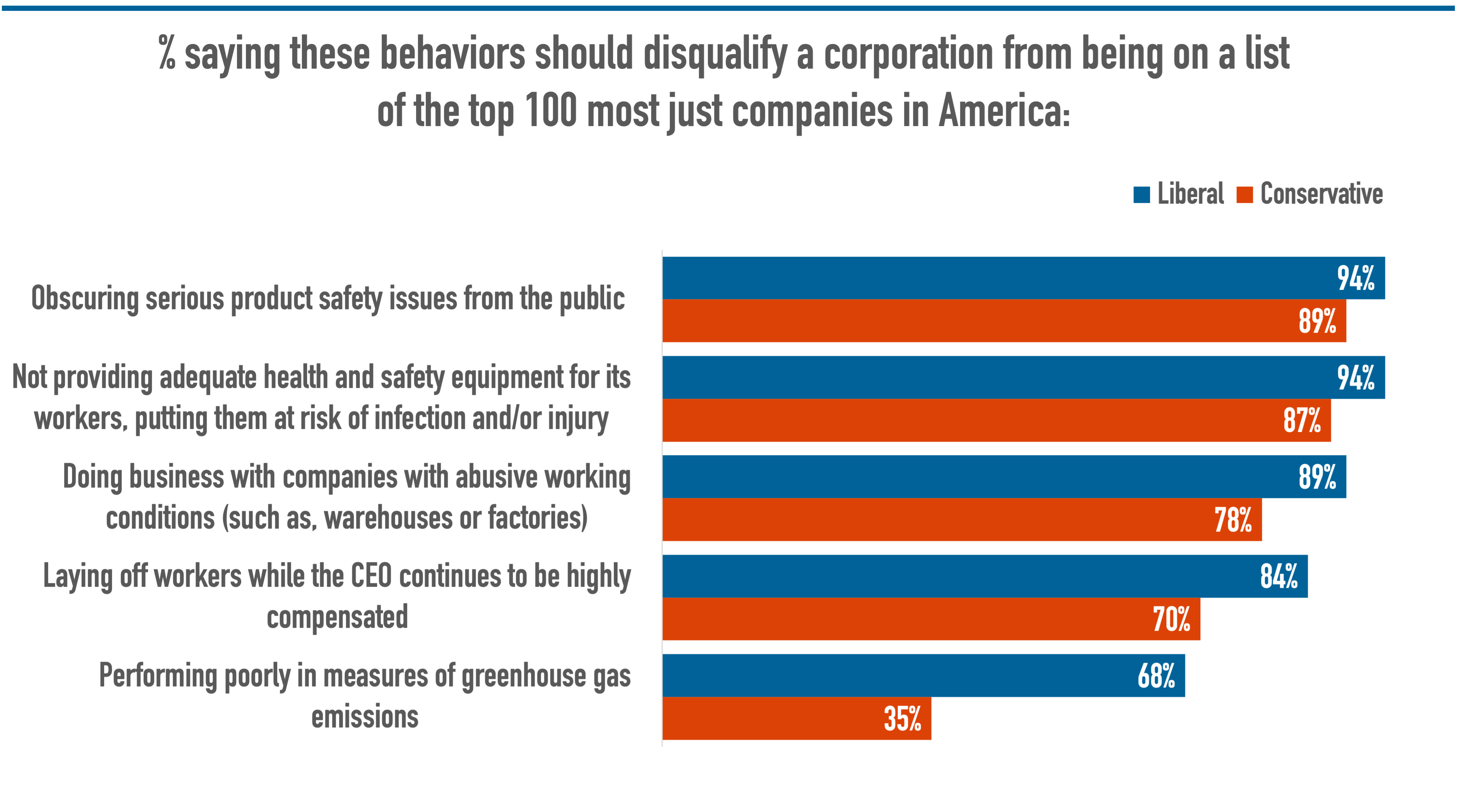

Liberals and conservatives also largely align on the business behaviors that they view as unjust. Large majorities of both groups believe it is unjust for corporations to hide product safety issues from the public, put workers at risk by not providing adequate health and safety measures, do business with companies that have abusive working conditions, and continue providing high pay to CEOs while laying off workers. The only issue that presented a split in opinion about unjust corporate behavior is greenhouse gas emissions – 68% of liberals believe corporations that produce more greenhouse gas emissions are unjust, compared to 35% of conservatives.

Despite the intense polarization that undeniably exists in our country today, a path toward unity seems to exist in how we approach stakeholder capitalism. Business leaders can do their part by putting forward a broader, more inclusive economic vision that allows all people to contribute and achieve their potential. And companies can take action by making the security and well-being of their workers their top priority – a move that truly bridges the ideological divide.

The debate raging this week in Congress around the $15 minimum wage – a Biden Administration “first 100 Day priority” – has put worker economic security back in the spotlight.

It’s a huge issue. Our own research shows that, incredibly, up to 50% of workers at Russell 1000 companies weren’t making enough to support a family of three, even with a partner working part-time. And that was before the coronavirus pandemic hit.

Amazon’s vocal support of a federal $15 min wage floor is, as Michelle puts it in a new piece, admirable. But if we’re looking at what Americans want, and what our biggest corporations can provide them, the bar has to be set higher.

“Paying a fair and livable wage” is the top issue Americans care about most when it comes to just business behavior, and that means paying more than minimum wage. It also means taking a wider view of worker financial health. The quality and availability of benefits; the capacity of workers to save for retirement or pay down student debt; worker financial education and literacy; upskilling and training; stock ownership and profit sharing; all of these things matter too.

More and more companies are starting to get it. This week saw GM announce that up to 44,000 eligible hourly UAW-represented employees could receive up to $9,000 in profit-sharing checks this year. The new CEO of Harley Davidson, Jochen Zeitz, a champion of corporate stakeholder performance (and former JUST Board member) announced the company would issue stock to 4,500 workers, including all of its hourly factory laborers, because when employees are engaged, respected, and have a stake in their work, the company benefits. Mastercard is building a major global initiative around financial inclusion.

The broader theme of investing in, listening to, and supporting workers is a bedrock of stakeholder capitalism. It’s good for business, and as our current Chart of the Week shows, it’s good for investors. It’s also why we’re so proud of the program we co-founded with PayPal, the Worker Financial Wellness Initiative, to guide companies on first evaluating, and then taking concrete steps to address, overall financial hardship among their employees. If you run a big company, and you want to get involved, I invite you to reach out.

Be well,

Martin

Citigroup is working with Black-owned investment firms for a $2.5 billion bond issuance.

As reported above, GM’s hourly workers are expected to receive $9,000 thanks to the company’s profit-sharing program.

Here are more details on Harley-Davidson issuing company stock to 4,500 employees, including all of its hourly factory workers.

Salesforce announced a new “Work From Anywhere” policy, offering employees three options for how they can work going forward: flex, fully remote, and office-based.

Tesla skips contributing to its 401(k) match for the 3rd year in a row, despite record stock price increases in 2020.

Wells Fargo makes equity investments in six Black-owned banks as part of a broader $50 million pledge to support minority-focused lenders.

12PM ET Today: Martin joins the NeuroLeadership Institute to discuss the companies that supported their workers, customers, and communities through the pandemic, and how increased scrutiny on diversity, equity, and inclusion disclosures is changing corporate America for the better. Sign up to listen here.

How can corporate America and the government work together to help all Americans? Martin spoke at a Bipartisan Policy Center event: “What’s Next for Stakeholder Capitalism in 2021.” Watch the replay here.

Our researchers Aleksandra Radeva and Molly Stutzman examine why corporate America needs a common standard for demographic disclosure.

The last couple of years have been scary for a lot of people. A good chunk of the population believes that capitalism is not working for them, that the system is rigged against them. There’s so much inequality that people are now in the streets. Business leaders are coming to a realization that this form of just staying with the status quo may not be sustainable for us as businesses. And I think that realization is creating this awareness that we have to lift up the bottom, we have to lift up the wages and working conditions of people for a better functioning society and economy.

– Zeynep Ton, President of the Good Jobs Institute, to JUST

“Predicting the future is hard. Nobody’s very good at it. For example, the Congressional Budget Office’s track record in its area of expertise – forecasting long term budget deficits – has been described in Forbes as “no better than throwing darts.” So when in its report on the Raise the Wage Act, the CBO chooses to model the employment effect of a $15 minimum wage by plugging in an elasticity value 10 times the consensus of experts in the field, it’s a safe bet that the CBO will once again be proven wrong. That said, regardless of its predictably implausible employment forecast, the CBO report actually makes a strong case for a $15 minimum wage. According to the CBO, 27 million workers would see their incomes rise. Nearly a million Americans would be lifted out of poverty. Even accounting for its predicted job losses, the aggregate pay of affected workers would increase by $333 billion. That’s a net gain for American workers and the American economy.”

– Nick Hanauer, Founder of Civic Ventures and Host of “Pitchfork Economics”

“The myth that sustainable investing results in lower returns is clearly just that. The Center for Sustainable Business’ new analysis of more than 1000 academic studies since 2015 finds that a very small percentage found a negative correlation – and in fact, 58% of corporate studies and 33% of investor-based studies found that ESG delivers superior returns. Managing for a low carbon transition appears to drive better performance for both corporates and investors, and sustainability appears to drive more innovation and better risk management, resulting in better financial performance, as well.”

– Tensie Whelan, Director of the NYU Stern Center for Sustainable Business, to JUST

Must-Reads of the Week

The New York Fed releases new research showing that lower-wage workers have borne much more of the brunt of job losses during the pandemic than higher-wage earners.

The Wall Street Journal highlights the latest CBO study saying that a $15 minimum wage would cut unemployment and reduce poverty. Goldman Sachs analysts estimate that about 30% of U.S. workers would benefit, and in some states like Mississippi, it might be as high as 40% of the state workforce.

The New York Times lifts up the plight of grocery store workers in a story focused on how many feel forgotten as the pandemic rages on, and Forbes reports on the food union’s push for hazard pay and more health and safety protections.

NBC reports that President Biden met with CEOs of JPMorgan Chase, Walmart, Gap, and Lowe’s to discuss equalizing the economic recovery and improving the wage gap.

Business Insider speaks with Ray Dalio on the fundamental changes capitalism needs to maketo address the inequities exposed through the crises of 2020.

CNBC shares a new analysis from the National Women’s Law Center, detailing how women’s labor force participation hit a 33-year low this January.

GreenBiz talks about how the “S” in ESG is finally having its moment, particularly around diversity and inclusion metrics, and Fortune adds more reasons why this sudden focus on social goals is not a passing fad for U.S. business. Meanwhile, Fast Company takes a deeper look into why so many corporate diversity reports are misleading.

Our latest Chart of the Week shows companies that don’t pay their workers well need to take up more debt (i.e. more risk) to have the same returns on equity as those that pay their workers well.

Following the death of George Floyd, Breonna Taylor, Ahmaud Arbery, and others – and the reckoning with racial injustice that followed – many of America’s largest companies responded by releasing public commitments to advancing racial equity. Companies across the board have pledged to boost their diversity, equity, and inclusion efforts by increasing the representation of Black, Indigenous, and People of Color (BIPOC) workers among their ranks, by instituting more equitable hiring, retention, and promotion policies, as well as other measures.

To hold companies accountable to these commitments, advocates from regulatory, research, and investor communities have asked companies to release their diversity data as a first step toward establishing a benchmark for improvement. But despite this consensus, there is currently very little guidance on what to disclose, resulting in inconsistent reporting of diversity data across corporate America. In seeking a more standardized method for disclosure, EEO-1 Reports – which provide a demographic breakdown of a company’s workforce by race and gender to the Equal Employment Opportunity Commission (EEOC) – could provide a helpful framework by which to make reporting on racial and ethnic diversity more consistent.

Last fall, the Securities and Exchange Commission (SEC) amended Item 101(c) under Regulation S-K, calling on employers to disclose human capital measures or objectives that a company deems material to its business, a step beyond the previous requirement to only disclose the number of employees. Even with this amendment, the new human capital reporting requirements make no mention of diversity data disclosure. In response, SEC Commissioner Allison Herren Lee outlined the importance of reporting on workforce demographics in her speech “Diversity Matters, Disclosure Works, and the SEC Can Do More,” noting that insufficient reporting requirements from the SEC has led to gaps and inconsistencies in disclosure. Lee and her colleague, Commissioner Caroline Crenshaw, spoke out against the SEC’s principles-based approach to human capital reporting and emphasized the need for a set of standardized requirements.

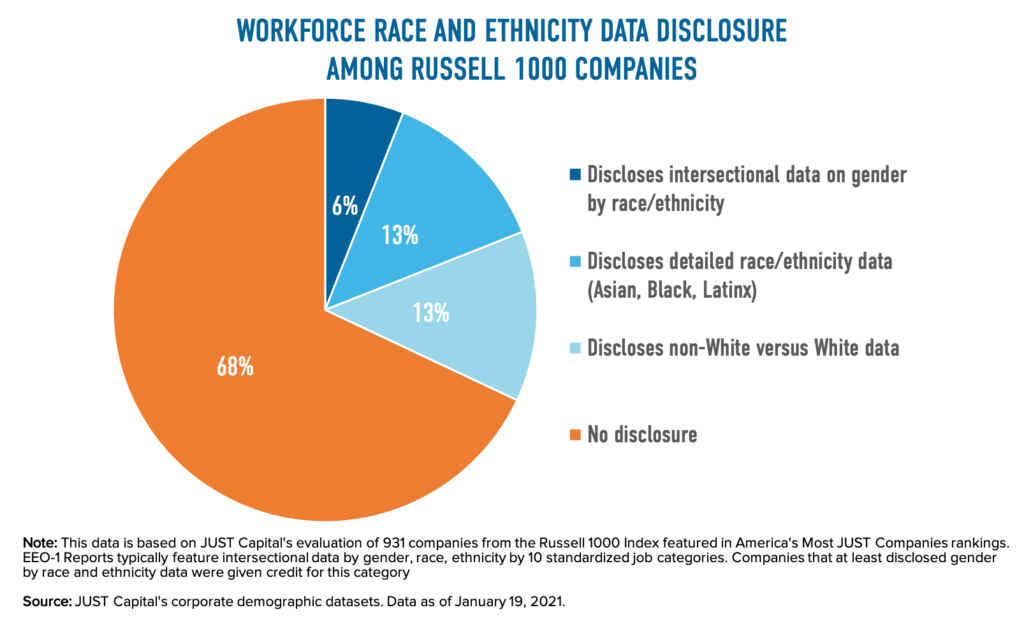

The lack of detailed and specific requirements leaves it to the discretion of companies themselves to determine what data is disclosed. Our own research has shown that, while 30% of companies disclose data on the racial and ethnic composition of their workforces, the detail of these disclosures is highly varied. For example, some companies disclose only on the number or share of Non-White workers, while some provide data on the number or share of Asian, Black, or Latinx groups, and others report highly intersectional data by gender, race, and ethnicity. When given the option, however, most companies deem diversity immaterial to their operations and do not share their diversity data. We have found that 70% of companies in the Russell 1000 do not have demographic data disclosure.

To address the lack of standardization and persistent gaps in reporting of race and ethnicity data, top firms in the investor community have advocated for companies to release their EEO-1 Reports. State Street was an early advocate for this framework, and most recently, BlackRock joined the ranks of investors asking companies to disclose the racial, ethnic and gender makeup of their employees.

The EEO-1 Report is currently viewed as a “gold standard” for disclosing workforce data on racial and ethnic diversity for several reasons. For one, it offers a detailed breakdown of each company’s workforce by gender, race, and ethnicity in the following categories: American Indian or Alaskan Native; Asian; Black or African American; Hispanic or Latino; Native Hawaiian or Other Pacific Islander; Two or more races; and White, as well as 10 standardized job categories that give a good sense of representation within a company not only as a whole, but also in senior and leadership positions.

In addition to the intersectionality of its reporting, it could be relatively easy for companies to adopt: companies are already required to maintain this data and report it to the EEOC. If the S-K included reporting on data found in EEO-1 Reports, it could alleviate the burden of having to prepare additional workforce demographic data. Doing so would also make it more possible to assess the current state of all companies’ diversity and benchmark their progress over time. The standardized reporting structure of the EEO-1 Report would also make it possible to compare some forms of diversity across companies and across industries.

It is important to note, though, that EEO-1 Reports do not capture all forms of diversity; notably, measures of diversity around non-binary gender identity, sexual orientation, disability, and veteran’s status, among other important demographic identifiers, are not covered by EEO-1 Reports. Nonetheless, given its intersectional reporting framework on gender, race, and ethnicity, the EEO-1 Report could serve as an important starting point toward more standardized and comprehensive demographic reporting.

Regulation S-K presents an opportunity not only to require increased reporting of demographic data but also for advocates from the regulatory, research, and investor communities to align on a clear, consistent, and comparable reporting framework. JUST Capital will continue to work with companies to release their EEO-1 Reports, acknowledging that, while this reporting framework is not perfect, it provides a practical and important option for companies to disclose diversity data in a standard format.

Nearly 10 months into the COVID-19 crisis in America, workers across the country continue to face unthinkable hardships. More than 26 million workers are unemployed, out of the labor force, or have reduced hours and pay as a result of the pandemic. Over 25 million people report that their household is food insecure and more than half of all adults identify having difficulty paying for household expenses. Workers who have remained on the job or recently returned face unimaginable health risks, often with little to no hazard pay.

At the same time, as we know from our COVID-19 Corporate Response Tracker, a number of companies have stepped up to help provide much needed support to their workers. From expanding paid sick leave plans and providing free PPE to establishing backup dependent care programs and hazard pay, some – though not nearly enough – of America’s largest companies have prioritized doing right by their workers. However, even fewer companies have taken steps to protect one particularly vulnerable segment of the workforce – temporary, vendor, and contract (TVC) workers.

Over the last three or more decades, businesses have increasingly relied upon the use of TVC workers to support the development of their products and services. Despite ensuring the successful day-to-day operations of offices and contributing to the core development of products, these workers have largely been left behind by companies, often being paid less and having access to fewer benefits. The COVID-19 crisis has exacerbated the precarious nature of these jobs, leaving many workers with little support when they needed it most. We explore a short overview of this often overlooked segment of the labor force below, and explore what steps companies in the Russell 1000 have taken to support this population, highlighting companies that are leading the way.

With the advent of the gig economy, the nature of contract work has gained increased attention from the media, policy makers, and the public. While workers at many of these companies are largely misclassified as independent contractors and the public is understandably questioning the nature of their employment, they are not representative of the broader temporary, vendor, and contract workforce. So, who are these workers?

TVC workers are individuals who contribute (directly or indirectly) to the development of a company’s products or services but are not the direct employees of that firm. For example: a company may contract with an agency to fill temporary fluctuations in workforce needs (e.g. during the holiday or summer season); a company may contract with a vendor to perform a specific service for the company either on-site (e.g. janitorial services) or off-site (e.g. payroll); and finally, a company may contract (directly or indirectly) with workers to meet specific business needs either on- or off-site (e.g. graphic designer). Collectively, this group of workers is referred to as the temporary, vendor, and contract (TVC) workforce.

Over the last few decades, companies have increasingly relied upon these forms of employment relationships. Dr. David Weil describes the phenomenon as the fissuring of the workplace. The days of co-workers under the same roof being employed by the same company seem to be behind us. Consider the last time you visited someone’s office. The security guard you passed on the way to the elevator, the receptionist at the front desk, the cleaning staff, and cafeteria workers are all likely employed by different entities despite all providing services and supporting the same parent company you visited.

Companies have traditionally argued that by focusing on their core competencies they could improve business outcomes. That is, by not having to directly manage janitorial staff, a technology company could better focus on developing new software, for example. Increasingly, though, companies have used TVC workers to fill roles that strike at the core competencies of the business. In short, companies are filling jobs up and down the wage and skill ladder with TVC workers rather than directly hiring employees.

A growing body of research has found that TVC employment relationships can have a significant negative impact on outcomes for workers. For example, one study that examined the rise in the use of contract workers in janitorial and security services found that there was as much as a 7% and 24% wage penalty for contract workers in these occupations, respectively. Similarly, news reports about contract workers at large technology firms, like Google, have highlighted significant disparities in pay and benefits, including paid time off, between similarly situated employees and contract workers.

Since COVID-19 hit the United States, JUST Capital has been tracking what companies have done to support their workers, customers, and communities. In the early weeks and months of the pandemic a number of companies announced new policies and benefits to support their employees and particularly frontline workers.

For example, when many businesses temporarily shut down, 52 companies (or nearly 6% of all Russell 1000 companies) announced that they would temporarily continue to pay their employees when the pandemic first began. After the CDC recommended a 14 day quarantine period for anyone who may have contracted COVID-19, 21% of companies announced new or expanded paid sick leave policies. And as schools and daycare centers shut down, 9% of companies offered new or expanded backup dependent care benefits.

While JUST Capital and others have celebrated companies for doing right by their workers during COVID-19, the complex nature of TVC employment relationships means that many of these workers have fallen through the cracks. Specifically, the scope of new corporate policies during the pandemic have almost exclusively covered employees, not TVC workers.

Across a number of issues, JUST Capital has found that only a handful of companies took specific steps to protect the TVC workers who support their businesses.

The COVID-19 crisis has underscored the precarious nature of the TVC workforce and the consequences of seemingly arbitrary division between policies for employees and TVC workers. In short, the lack of corporate action to protect TVC workers during the COVID-19 crisis is a function of a long-run trend in corporate America: increasingly companies have relied upon TVC workers to support their businesses but for legal or other reasons failed to take responsibility for the economic outcomes of these workers. But it need not be this way.

JUST Capital’s polling shows that only 25% of people think the current form of capitalism is working for society. Importantly, 89% of Americans think this is a moment for large companies to “hit reset” and change how they are treating their stakeholders. As more companies begin answering the public’s call for change and focus on improving outcomes for their workers, they should take a close look at their contracting practices too and ask whether the treatment and outcomes of these workers align with their mission and values.

Over the next several months, Americans are expected to have access to a COVID-19 vaccine. For the first time, the end of the pandemic seems like it is within our reach. However, even after vaccines are distributed, workers and businesses across the country will continue to struggle to recover from the economic hardships of 2020. Temporary, vendor, and contract workers are no exception. In fact, as businesses reopen and rehire workers, some experts predict an increase in the prevalence of TVC employment relationships. This means that many workers may return to jobs that are less secure than those they held prior to the COVID-19 crisis. At the same time, though, we are seeing meaningful steps taken by some businesses to raise wages for low-wage and historically marginalized employees. The trajectory of the experience of employees and TVC workers should not continue to diverge.

As more companies embrace stakeholder capitalism and strive to create greater value for their workers – they should consider what they are doing for all of their workers, including the temporary, vendor, and contract workers who ensure the success of their operations and products.