On Wednesday, a relatively new activist investor firm owning 0.02% of ExxonMobil stock gathered enough support to win at least two seats on the oil and gas giant’s board. The shockwaves of this outcome, which would have been unthinkable a few years ago, will reverberate throughout every boardroom in America and may even change the course of shareholder activism itself.

The firm, Engine No. 1, and its campaign are emblematic of a generational shift in American capitalism. When it nominated board members to push the company on its climate and clean energy strategy, it did so on the basis of shareholder value creation, not politics or some sense of “social good.”’ The institutional and retail investors who voted in their favor did so because they were persuaded by the business imperative put forth by the campaign. (Disclosure: Engine No. 1executive Jennifer Grancio and ExxonMobil board member Ursula Burns are both JUST advisors.)

Likewise, the 61% of Chevron investors who voted on Wednesday in favor of cutting Scope 3 emissions (emissions from the use of the company’s products) believed this was in shareholders’ best interests.

The same can be said of matters relating to diversity, equity, and inclusion (DEI). As JUST’s managing director of corporate engagement, Yusuf George, explained on CNBC this week while discussing our latest pay equity analysis, this is not about politics. It’s about the right of every worker to be respected, valued, and given a fair shot. That’s the American way. That’s what good business looks like.

Clearly, many shareholders agree. Bloomberg reported there were a record 37 DEI-related proposals this proxy season, with an average 43% of support as of a week ago, up from 21% last year. Strong majorities of shareholders voted for the release of annual diversity reports at IBM(94%), DuPont (84%), Union Pacific (81%), and American Express (60%). Why? Because companies that do better on DEI are more competitive, do better in the market and make more money for shareholders.

This notion that investing in stakeholders is somehow anathema to serving shareholders is a dangerous fallacy. Investing in workers, building strong and diverse teams, supporting local communities, creating good jobs, reducing environmental impacts, doing right by your customers, and yes, running a company with ethics and integrity – this is how shareholder value gets created. It’s how American companies can compete and win on the world stage. And it’s what millions of Americans want.

Be well,

Martin Whittaker

P.S. In honor of our veterans on Memorial Day, we produced this special piece of research. Please check it out.

Amazon is instituting a plan to reduce worker injuries by 50%.

GM is now supporting unionization at its new battery factories for its electric fleet.

Ford boosts investments on electric vehicles and commits to spend $30 billion.

Shell has been ordered by a Dutch court to cut its carbon emissions.

Under Armour is raising its starting wages to $15 an hour in the U.S.

As part of our ongoing work tracking how companies are following through on their DEI commitments, we shine a light this week on pay equity analysis. 85% of Americans overall and 91% of Black American respondents believe it is important for companies to conduct annual pay analyses, yet only 31 of America’s largest employers disclosed conducting an analysis by race or ethnicity and only 14 disclose the gaps. Yusuf joined Andrew Ross Sorkin on CNBC Squawk Box to discuss the details.

Our Corporate Racial Equity Tracker was featured in the Anti-Racism Daily newsletter, and our recent survey work was highlighted in this Financial Times feature marking the anniversary of George Floyd’s death.

Martin appeared in the Financial Health Network’s Emerge Everywhere podcast and Columbia Business School’s Capital for Good podcast to discuss the rise of ESG and stakeholder capitalism.

“Context matters. People are not merely financial engines. We are still in the middle of a pandemic even though we are seeing significant improvements. Nearly every facet of people’s work and nonwork lives has been upended.”

“I don’t think you can, in this age, have a dichotomy of what you say outside and what you say inside. That’s not sustainable. Any company that’s doing this is doomed.”

“This is a landmark moment for Exxon and for the industry. How the industry chooses to respond to this clear signal will determine which companies thrive through the coming transition and which wither.”

Lots of new research on inequality. McKinsey reports on “Unequal America” through a new opportunity survey that spotlights Americans’ views on economic opportunity, the obstacles they face, and the path ahead to create a more inclusive economy. Morning Consult and Axios’Inequality Index inched up as stimulus checks’ impact winds down. Researchers at the University of Chicago chart the stagnation of average earnings and income inequality since the 1970s in a series of interactives.

Quartz looks at new apps that enable retail investors to vote against things like increased CEO pay during proxy season. The Financial Times reports that this year has broken the record for the most CEO pay increases rejected by shareholders.

Fast Company features a new Glassdoor report that shows LGBTQ employees rate their companies much lower than their non-LGBTQ counterparts, especially workers at Walmart, Wells Fargo, and Amazon.

Forbes chronicles corporate attempts to prevent burnout by adding more vacation days to employees’ calendars. The problem? Most aren’t actually using them. CNBC also reports on how companies are trying to support their workers’ mental health.

For Memorial Day, we took a closer look at veteran hiring practices, and saw that companies that disclose specific veteran hiring policies outperform those that don’t. Learn more here.

(Dean Mouhtaropoulos/Getty Images)

The campaign by activist investors Engine No. 1 and CalSTRs to push ExxonMobil to embrace a clean energy future is one we have been tracking closely. The oil major is coming off one of its worst years ever, and announced during its Monday earnings call that it would be building a $3 billion low carbon solutions business over the next five years.

Yet CalSTRs called the announcement “minor” and “inadequate,” rejected a new director proposal, and said the energy giant’s $22 billion loss “demonstrates the continued erosion of shareholder value and that incremental changes are not enough to restore investor confidenceand position the company for the global energy transition.”

Why is this so important? Because it illustrates perfectly what our friend George Serafeim of Harvard Business School recently wrote about, namely, that “investors are becoming sophisticated enough to tell the difference between greenwashing and value creation.”

With ESG investing growing at such a breathtaking pace, this issue is only going to get bigger. Morningstar reported that global sustainable fund assets climbed 29% in Q4 to $1.65 trillion, with net flows to U.S. ESG funds setting a new record of $51 billion in 2020, more than double the total for 2019 and nearly 10 times more than in 2018. (Most of these funds outperformed their benchmarks during the pandemic.)

Just yesterday, Moody’s forecasted that global issuance of sustainable bonds would also hit a new record of $650 billion this year, up more than three-fold from last year and representing 8-10% of total global bonds issued in 2021.

Even the SPAC (special-purpose acquisition company) market is getting in on the act. We found that roughly 45 sustainability-oriented SPACs launched over the past year, ranging in size from $100-400 million, with several now having a market cap above $1 billion.

All of this money, and all the money that flows after it, is eventually going to ask the question, what impact did we have? Are we actually moving the needle on underlying societal challenges, and how do we know whether ESG performance is actually being delivered?

Demonstrating real authenticity of social and environmental impact is finally becoming the basis on which ESG investment products compete.

Be well,

Martin Whittaker

Amazon warehouse workers in Alabama will decide next week if they want to be the company’s first U.S. employees to unionize. Amazon goes on the offensive in response.

Darden Restaurants announced it will offer paid sick leave for employees to receive the COVID-19 vaccine.

Google will pay $2.6 million over claims that the firm’s hiring processes have been biased against women and Asians.

Mastercard pledges to reach a goal of net-zero emissions by 2050 – in its own operations and in its suppliers’.

Martin Whittaker joined JUST board member Alan Fleischmann on SiriusXM to talk Leadership Matters – everything from how companies have supported their workers through COVID-19, to the growing expectations Americans have for corporate America, and more. Listen here.

Martin joined JUST Board Member Dan Ariely to discuss BeWorks’ 2021 Choice Architecture Report – exploring the ways companies can use behavioral science to improve their culture.

Yusuf George joined Judy Samuelson, Founder and Executive Director of the Aspen Institute Business and Society Program, for a conversation on how intangibles, such as reputation and trust, are beginning to have a greater impact on business value – particularly in these tumultuous times.

(Paul Morigi/Getty Images)

“A level playing field will help us all. What do I mean by that? If all businesses have to abide by the moral and capitalist backbone of fairness, of employer and employee strength, of commercial strength – then we would not be faced with making these short-term choices of increasing our earnings on the backs of our employees…on the backs of our sustainability efforts.”

Ursula Burns, Former Xerox Corporation Chair & CEO, in the Rockefeller Foundation’s event “A Framework for Inclusive Capitalism”

“I think more of us are saying it’s now time to cut the bullshit and get serious about attacking these difficult and interrelated problems before it’s too late. …And that’s the context in which I see an increasing resolve in the world of sustainable finance to invest in solutions and to very strongly encourage companies to take the long view, valuing stakeholders and positioning for a just transition to a net zero economy by mid-century. It’s what we all want, and perhaps to the surprise of those not well-versed in the world of finance, this sector is clearly going to play a major role.”

Jon Hale, Global Head of Sustainability Research at Morningstar, to JUST

“The growth has been phenomenal. …. [F]rom the $110 trillion assets that are being professionally managed, we are seeing 40 percent of global financial assets with an ESG consideration. And that will only increase.”

Anne Finucane, Vice Chair of Bank of America, to the Financial Times

In the history of the Fortune 500 there have been only 19 Black CEOs out of 1,800. Fortune profiles them all here. Walgreens names Starbucks executive Rosalind Brewer as the company’s next CEO, increasing the list to 19. But Ken Frazier of Merck and Roger Ferguson Jr. have both announced retirements, leaving Brewer, Marvin Ellison at Lowe’s, and René Jones at M&T Bank as the only three Black CEOs currently leading Fortune 500 companies.

In honor of Black History Month, Business Insider shares a collection of essays and articles from Black writers for readers looking to further educate themselves about Black history and America’s history of racism.

EPI releases a new fact sheet showing how the Raise the Wage Act would benefit U.S. workers and their families. Of the 32 million beneficiaries: 31% would be African American, 26% Latino, and 59% women – many of whom have attended college (43%) and have children (28%).

Despite raising the threshold for inclusion in the 2021 Gender Equality Index, Bloombergannounced that a record number of companies disclosed data on gender equity and inclusion in their workforces, as well as improvements in the quality of disclosure.

Forbes’ Senior Contributor Jack Kelly predicts that the future of work is being able to work anywhere you want while receiving the same pay, rather than the pay cuts many firms are imposing now.

Our latest ESG Chart of the Week takes a look at how industry leaders are at the forefront of the movement to disclose EEO-1 diversity data.

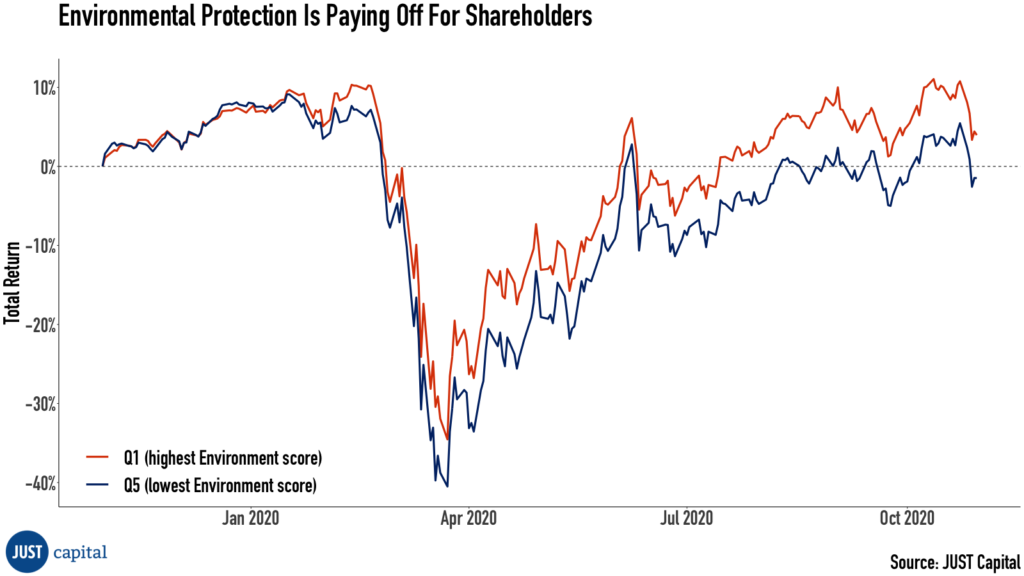

In our last Chart of the Week, we argued that companies increasingly face the prospect of needing to incorporate carbon emissions and emission reductions when engaging in internal cost-benefit analysis for new projects. As we’ve shown before, companies with lower carbon emission intensity outperform their peers in the stock market. This week, we look at the broader picture and find that companies with overall lower environmental impacts also outperform their peers:

For this analysis, we divide the companies we ranked this year into quintiles by their scores in our Environment stakeholder relative to their industry peers. We find that the top quintile (Q1) had returns of 3.96% over the trailing year to October 31st, while the bottom quintile had negative returns of -1.47%. This is in line with our previous results and once again demonstrates the win-win of just business behavior when it comes to environmental protection.

In addition to this fundamental insight, with the incoming Biden administration, we expect increasing political and regulatory pressure for companies to reduce their impact on the environment. In turn, this results in an increasing divergence in company performance between those that are prepared and those that are not. What this means is that now is the time for companies to act and to prepare – both for the sake of their shareholders and for the sake of the environment.

If you are interested in supporting our mission, we are happy to discuss data needs, index licensing, and other ways we can partner. Please reach out to our Director of Business Development, Charlie Mahoney, at cmahoney@justcapital.com to discuss how we can create a more JUST economy together.

If you have questions concerning the underlying analysis, please reach out to our Senior Manager for Quantitative Research, Steffen Bixby, PhD, at sbixby@justcapital.com.

Last month, the Department of Labor released a proposal that would effectively keep all ESG (environmental, social, and governance) investing out of ERISA retirement plans.

“As Private employer-sponsored retirement plans are not vehicles for furthering social goals or policy objectives that are not in the financial interest of the plan,” Labor Secretary Eugene Scalia wrote, and called out ESG funds specifically.

We disagree with the way ESG is characterized in the proposal and think that implementing it would crush significant momentum for assessing companies based on the value they add to all stakeholders, including shareholders. It’s why we submitted the following comment to the DOL. Thursday is the final day the public can weigh in.

We are writing in response to the Department of Labor’s proposed rule, “Financial Factors in Selecting Plan Investments” (RIN 1210-AB95) (the “Proposal”).

JUST Capital is a nonprofit with a mission to build an economy that works for all Americans by helping companies improve how they serve all their stakeholders – workers, customers, communities, the environment, and shareholders. Uniquely, JUST Capital engages the American public to determine what matters most to them when it comes to just business behavior. We then define metrics that map to those issues and track and analyze the companies in the Russell 1000. The analysis helps companies benchmark and improve stakeholder performance, and incentivizes a “race to the top” through our high-profile Rankings with Forbes, as well as investment products like Goldman Sachs’ JUST ETF, which tracks our JUST U.S. Large Cap Diversified Index (JULCD), and has $137 million AUM.

The Department makes claims about the growth and role of “ESG” investing and its appropriateness in the context of ERISA plans, and then proposes to put ERISA sponsors in the fiduciary box with a rigid understanding of the relationship between “financial” and “nonpecuniary” factors. We respectfully request that the Proposal be withdrawn.

Thoughtful long-term allocators of capital are committed to considering the corporation’s role in meeting its obligations to other stakeholders, such as the Business Roundtable’s statement of August 2019, and moving beyond Milton Friedman’s iron-clad view that shareholders are the only stakeholder that deserves consideration, which the proposed rule the Department seeks to codify. Over the past six years, we have also surveyed over 100,000 Americans on this matter, and there is overwhelming and widespread support for stakeholder and ESG considerations in business and financial decision making.

We believe the proposed rule will ultimately result in lower risk-adjusted returns for ERISA plan holders, the same American people the rule is intended to protect. Research supports that long-term, risk-adjusted shareholder value is maximized when companies have good governance and managerial leadership aligned around maintaining a productive, safe workforce to serve customer needs in the context of the health of the social and physical environment in which they operate.

The Department states, “There is no consensus about what constitutes a genuine ESG investment, and ESG rating systems are often vague and inconsistent, despite featuring prominently in marketing efforts.” We submit that the investment community is coalescing around a definition of “ESG” that means, broadly, analyzing a company’s environmental, social, and governance characteristics, and incorporating those externalities into company valuations as part of a broadly diversified investment portfolio.

Ever since Graham and Dodd defined the field with their seminal Security Analysis text, financial analysts have gone beyond a company’s financial statements, which can only ever be backwards-looking, to investigating the company’s product offerings, its managerial quality, its social and economic environment, its relationships with suppliers and workers, and a host of other potential cues about its likely future prospects. Additionally, as companies have shifted from fixed to intangible assets, understanding how businesses are managing their human capital and market relationships with customers and suppliers takes on even more salience, and traditional accounting has failed to keep up with this shift. Taking this additional information into account gives analysts the capacity to build that forward-looking view.

And financial analysts since Graham and Dodd have been estimating – and disagreeing about – company valuations ever since. Those disagreements are what “make the market” as new information is impounded into security prices.

Thus, “ESG” is part of traditional company valuation analysis and has been for decades. These considerations have been with us since the dawn of modern financial analysis, and in this regard deserve no special consideration from the Department.

We also acknowledge the Department’s interest in preserving the fiduciary duty of sponsors to provide plan participants with “financial, rather than ‘nonpecuniary’ benefits.” In this regard, the evidence is mounting that companies that perform better on management of “ESG” issues certainly do not underperform their peers, and may even outperform them.

Our extensive public polling has identified with great specificity what the American public thinks the priorities of U.S. companies ought to be. We find that since we began this work, the companies that are most aligned with the priorities of the American people actually outperform the broader market.

Our experience is not unique. The evidence from years of experience suggests that investors in equity investment funds with “ESG” or “sustainable” goals do not need to sacrifice risk-adjusted returns. The notion that investors cannot maintain financial prudence while considering non-financial measures of performance is simply a false choice.

Given the evidence that “ESG” funds offer risk-adjusted performance in line with their peers, we believe they pass the “all things being equal” test and are entirely consistent with fiduciary duty as part of a well-diversified QDIA offering. As with consideration of any investment in this context, care must be given to the quality of the investment manager, the fund’s stated investment strategy and holdings, their investment process, and expected returns net of fees.

The American people are the ultimate beneficiaries of American companies, through their ownership in ERISA-sponsored plans, other retirement plans and ownership vehicles, and the final taxation and regulatory power of the U.S. Government. Americans can express their will as voters, but their capacity to effect change at corporations, even as the beneficial owners in an ERISA-sponsored plan, is limited given the proxy voting process.

Our polling tells us what the American people want from corporations: They want them to build loyal, stable, continually-learning workforces and pay them fairly; establish good relationships with the communities where they operate; provide safe, honest products and services to their customers, and leave the physical environment in which they operate in the same condition or better for their being in it.

Denying ERISA plan participants access to investment vehicles that incorporate “ESG” considerations would be closing off access to important non-financial information that affects company, and investment, valuations. It could leave sophisticated investors the fruits of deeper analysis, while relegating ERISA participants to the crumbs of underperformance. The evidence is strong and growing that “ESG” considerations are critical factors in evaluating long-term company performance and future prospects. Incorporating those and all relevant factors in a thoughtful valuation process is the core of achieving superior risk-adjusted returns, and fiduciary duty demands that we deliver the highest available risk-adjusted returns to the American people in their ERISA-sponsored plans.

Thank you for considering these comments.

Last month, the Department of Labor (DOL) proposed a new investment duties rule that would essentially keep ESG funds out of retirement accounts and kill ESG momentum if enacted. Everything I’ve seen throughout my career shows that such a move would hurt investors. The comment period closes this Thursday.

While the DOL states “the rule is intended to provide clear regulatory guideposts for plan fiduciaries in light of recent trends involving environmental, social and governance (ESG) investing,” the context they provide shows a lack of understanding of ESG. This will affect everyday American’s access to modern day investment strategies, which take into account the way businesses treat stakeholders. With the update, the DOL seeks to clarify requirements for plan fiduciaries, stating that ERISA plan fiduciaries cannot invest in ESG vehicles when they “understand an underlying investment strategy of the vehicle is to subordinate return or increase risk for the purpose of non-financial objectives.”

The crux of the problem with the proposed rule is that it rests on the outdated belief that ESG funds subordinate financial objectives to environmental, social or governance objectives, and will therefore underperform. In fact, just the opposite is true. JUST Capital launched the JUST US Large Cap Diversified Index (JULCD) on November 30, 2016, the index underpins the Goldman Sachs JUST U.S. Large Cap Equity ETF (JUST ETF), which launched in 2018. At 2Q 2020 the JULCD represented 447 of the top companies in the Russell 1000, by industry, according to our rankings. The Index provides broad exposure to companies that do right by their stakeholders: workers, customers, communities, the environment, and shareholders. Since inception through 2Q 2020, the index returned 13.73%, outperforming both the Russell 1000 and the S&P 500, which returned 12.43% and 12.53% over the same period.

External studies have also shown that ESG funds generally outperform conventional peers. An April Morningstar report by Jon Hale, PhD, CFA found that from 2014 through 2019, sustainable funds showed strong performance in both up and down markets relative to conventional peers. Per Hale, “when markets were flat (2015) or down (2018), the returns of 57% and 63% of sustainable funds placed in the top half of their categories. When markets were up in 2016, 2017, and 2019, the returns of 55%, 54%, and 65% of sustainable funds placed in the top half of their categories.”

Our work at JUST Capital over the last six years centers on elevating the voice of the public to align their priorities for just business behaviors with corporate action. Coupled with that, we seek to highlight the relationship between the financial outperformance of just companies and how well they serve all stakeholders – the results show a clear connection between the two, debunking the myth that ESG investments are doomed to underperform.

Amidst the COVID-19 pandemic, JUST Capital has doubled efforts to look under the hood to evaluate how companies are treating their stakeholders during the crisis and highlight the outperformance of just companies. What we’ve found is that companies with strong corporate governance lead the market in a downturn. We did this analysis on Russell 1000 companies by looking at the data points related to corporate governance within the JUST Capital rankings model.

In this exercise, we noted that top quintile companies have significantly outperformed the market in the past year by 3.0% relative to the fifth quintile performance during the past year. With regard to social issues, we found in particular that companies that have prioritized their workers during the pandemic have continued to outperform. Looking at the performance of each quintile year-to-date as of 5/31, we see the top quintile (Q1) outperforming by 6.26% relative to the bottom quintile.

Earlier in my career, I worked as an ETF product manager for private wealth clients. A critical part of my role was evaluating the holdings, investment strategies, and performance of ETFs and determining whether they were acceptable offerings for our clients. This meant I needed to take the time to carefully evaluate the funds. What was driving performance? Did the holdings match the fund’s stated investment objective? How did the fund compare with peers in its asset class?

That experience leaves me confident that the DOL proposal would do a disservice to all investors, but particularly millennials, who are overwhelmingly inclined towards making ESG investments and whose 401 (k) plans represent a large portion of their savings. In the most recent “Better Money Habits® Millennial Report” Bank of America found that “of millennials with savings, three-quarters are saving for retirement.” And a recent Morgan Stanley report found enthusiasm for sustainable investing at an all-time high, with 52% of the general population and 67% of millennials taking part in at least one sustainable investing activity, such as investing in companies or funds that target specific environmental or social outcomes. The report goes on to state that “investors want products that match their interests; 84% want the ability to tailor their investments to their impact goals, 90% among millennials.”

To be clear, the work we do at JUST is in complete harmony with the stated mission of the DOL, which is “to foster, promote, and develop the welfare of the wage earners, job seekers, and retirees of the United States; improve working conditions; advance opportunities for profitable employment; and assure work-related benefits and rights.” With institutional investors increasingly investing in ESG leaders and moving away from ESG-risky companies, our concern is that the general public will be left owning companies in their 401 (k) plans that face high downside risks as a result of poor environmental, social, and governance performance.

Adding hurdles such as documentation requirements for fiduciaries choosing between “truly economically ‘indistinguishable’ investments” could work to disincentivize plan sponsors from adding ESG investment options, which many end investors are interested in, and eventually make 401(k) plans a haven for companies rated as ESG laggards.

We hope to see more firms add their voice to the discussion so that investors can choose from best in class companies in their retirement plans, companies who look after their stakeholders, ensuring a better future for all.

This week, we’re turning to the Environment stakeholder, which – despite heightened focus from business and investment leaders at the start of this year that’s also confirmed by our polling – has taken a backseat to the urgencies of pandemic, economic recession, and racial reckoning. But climate change remains a critical issue that needs our nation’s attention, and intersects distinctly with both the impacts of pandemic and systemic racism.

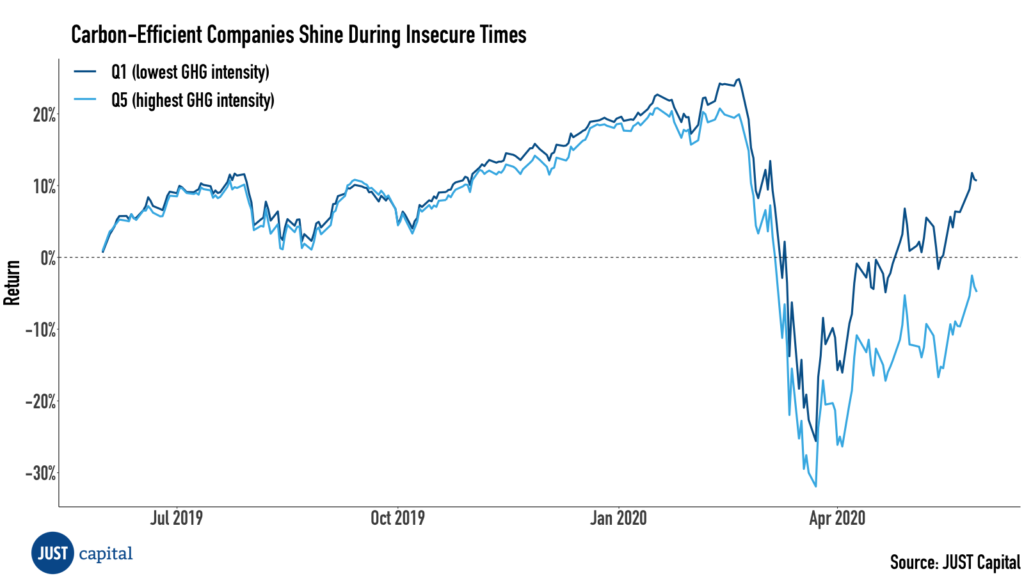

Climate change must remain part of the conversation. Earlier this week, First Street Foundation published critical new analysis showing flood risk data for more than 142 million homes and properties across the U.S., and found that over 10% of these properties face substantial risk of flooding, and even more should sea levels continue to rise as a result of climate change. While this demonstrates the potential costs of climate change, companies might be reluctant to reduce their carbon emissions, citing the costs of doing so. In our latest Chart of the Week, we show that a lower carbon footprint can actually be beneficial for a company’s bottom line.

To run this analysis, we looked at the GHG intensity – the amount of GHG emissions per dollar of revenue – of our ranked companies relative to their respective industries. When comparing the performance of the top quintile to the bottom quintile we find an outperformance of 15.5% over the last year. While the top quintile saw a 10.7.% return, the bottom quintile is down by 4.8%.

The result is a classic win-win: Companies emitting fewer greenhouse gases gain more in value. One possible explanation for this might be that a reduction in greenhouse gas emissions comes with lower energy costs. There is also the avoidance of stranded assets and potential regulatory costs like a carbon tax.

What this means is that climate change does not have to be a collective action problem. There is direct value for companies in mitigating climate change by reducing their greenhouse gas emissions, irrespective of the actions of their competitors. Reduced societal costs, such as limiting flooding, are the result.

In previous Charts of the Week, we looked at aspects of corporate governance and social responsibility and how both improve the bottom line for companies and investors. In light of these results, we maintain our strong belief that there is sufficient evidence for ESG factors being material to the investing process as a risk management tool. That’s why the proposed rule of the Department of Labor on the use of ESG vehicles in ERISA plans seems outdated already and nothing more than a form of appeasement to people insisting on the idea of shareholder primacy.

At JUST, we’re going to continue analyzing the ways companies are prioritizing stakeholder capitalism, and our research has shown that the E, the S, and the G all have their role to play in fostering long-term business health.

If you are interested in supporting our mission, we are happy to discuss data needs, index licensing, and other ways we can partner. Please reach out to our Director of Business Development, Charlie Mahoney, at cmahoney@justcapital.com to discuss how we can create a more JUST economy together.

If you have questions concerning the underlying analysis, please reach out to our Senior Manager for Quantitative Research, Steffen Bixby, PhD, at sbixby@justcapital.com.