(Christopher Furlong/Getty Images)

As the first week of COP26 draws to a close, it’s becoming clear how much the conversation has shifted to incorporate the financial and corporate worlds.

Former Bank of England chief Mark Carney announced that his Glasgow Alliance for Net Zerohas as much as $130 trillion committed to hitting net zero carbon emissions by 2050. The group comprises “more than 450 banks, insurers, and asset managers across 45 countries” and includes top JUST performers Bank of America, BlackRock, and Citi. Janet Yellen, the first U.S. Treasury Secretary to attend COP, said that the private sector needs to play a bigger role, and sent a clear message: climate change is an economic issue, and the costs of insufficient action far outweigh the investments needed for an energy transition, for both governments and business alike. “Private capital is essential to our success,” she said, adding that as the U.S. government, investors, and corporations make progress, job creation will be paramount.

As I mentioned last week, corporate climate policy standards are seen as being critical to achieving these broader goals. A new piece from JUST’s Laura Thornton shows why even though companies like COP sponsors Microsoft and Salesforce can make impressive climate-related commitments, proprietary terminology and reporting makes it impossible for investors and other stakeholders to fully compare where they stand in relation to each other.

This is gradually changing. Building on last week’s net zero standard announcement from SBTi, the International Sustainability Standards Board launched yesterday and said it is consolidating existing major frameworks (VRF, SASB, the IIRC and the CDSB) into a single reporting body to serve regulators and investors around the world.

Building confidence in corporate reporting – not just on climate, but on all stakeholder performance issues – is critical. The market can only begin to reward (and punish) companies for their actions when the results are both seen and also believed.

Be well,

Martin

Apple adds 100 more suppliers committed to using clean energy, helping it get closer to a carbon-neutral supply chain by 2030.

Citigroup announces a $1 billion social finance bond to advance social initiatives globally.

Colgate-Palmolive announces a EUR 500 million 8-year sustainability bond to support its 2025 sustainability and social impact strategy.

Facebook plans to shut down its facial recognition system and delete the face scan data of more than one billion users.

McDonald’s workers strike in 10 cities to combat workplace sexual harassment.

Starbucks plans to boost wages to at least $15 an hour – up from $12 currently – for all partners by the summer of 2022, aiming for an average of $17 with rates ranging between $15 to $23.

Walmart increases educational opportunities for Black Americans by adding three HBCUs to its 100% tuition-paid college offering, alongside investing several million in education grants.

Zillow shuts down its home buying business and lays off 25%, or about 2,000, of its employees.

It’s clear more companies are investing in diversity, equity, and inclusion (DEI) programs, but how are they doing? Our latest polling looks at where employer and worker perspectives align and diverge on motivations, communications, goals, progres, and more. Some topline stats: While 90% of workers and employers believe their organizations are taking DEI seriously, only 49% of workers think their company has established clearly defined DEI goals. Explore the insights here.

Ahead of the COP26 UN Climate Summit, we spoke with HP CEO Enrique Lores for our latest Quarterly JUST Call, covering the company’s outstanding work on climate action and digital equity, and how its sustainability initiatives have generated more than $1 billion in revenue for two years straight. Read the takeaways and watch the replay here.

And, as the conversation at COP26 focuses on standardization in climate targets, JUST’s Laura Thornton explains why the language companies use with these goals can be misleading to employees, customers, shareholders, policymakers, and other key stakeholders – ultimately lessening corporate accountability.

Zachary Conway, CEO of Seeds (which utilizes JUST data to deliver impact insights to advisors and the clients), spoke with Adrian Grenier on the importance of impact investing, and where the winds are headed for the ESG market.

(Patagonia)

“At Patagonia, we don’t use the word ‘sustainable.’ Why? Because we recognize we are part of the problem. Previously, we set ourselves the target of carbon neutrality by 2025. But purchasing offsets to get us there doesn’t erase the footprint we create and won’t save us in the long run. We must first put the weight of our business behind drastically cutting emissions across the full length of our supply chain.”

“We are seeing more hydrocarbons moving away from public entities to private entities. If we’re serious about this . . . we have to ask all of society to move forward or we’re lying to ourselves, we will not get to a net zero.”

“There’s no comparable feat that mankind has ever achieved to what we need to do for climate change…green cement costs twice as much, green aviation fuel costs twice as much. Through innovation, the rich countries have to bring that down so dramatically. [We have to do that] so that we can turn to India and say, OK, yes, you’re still building basic shelter for your citizens. And we can’t tell you to do that at half the rate because you’re buying expensive cement.”

With COP26 in full swing this week, here additional stories you may have missed:

The Financial Times looks at the consistent problem with companies struggling to set and understand net zero goals for themselves and their industries thanks to a lack of common standards. To help, SBTi launched the first net zero global corporate standard last week.

Insider releases its second annual list of DEI Trailblazers, highlighting 16 diversity executives who have helped to change corporate culture. Read the whole list and delve deeper into our conversation earlier this year with JPMorgan’s trailblazer, Brian Lamb.

This chart comes from our latest DEI survey analysis, and points to one of the most interesting splits – near equal amounts of workers think their company is “going above and beyond on DEI efforts” and that “there is more work to be done.” Explore this another key insights and takeaways for corporate leaders looking to deepen their work.

JUST Capital is thrilled to share that Dr. Jason Wingard, President of Temple University and Founding Partner and Chairman of The Education Board, Inc., has joined our Board of Directors. Dr. Wingard joins us on the heels of a major board expansion we began in June – at which time we invited six new members onto our Board – and brings with him extensive expertise in the areas of organizational strategy, leadership development, and the future of work.

In addition to his role as President of Temple University, Dr. Wingard also holds a dual appointment as Professor of Policy, Organization, and Leadership and Professor of Human Resource Management – and prior to his time at Temple, served on the faculty of Columbia University, the Wharton School at University of Pennsylvania, and the Stanford Educational Leadership Institute at Stanford University. Outside of academia, Dr. Wingard also served as Managing Director and Chief Learning Officer at Goldman Sachs, developing strategy for and implementing leadership development solutions for the firm’s partners, global workforce, and clients.

Dr. Wingard’s experience comes to us at a crucial moment, as we deepen our focus on human capital disclosure (bolstered by the SEC’s increasing prioritization of these issues), provide guidance to C-suite leaders on how to advance racial equity, and work to make workers’ financial well-being a C-suite priority, shaping an equitable and inclusive recovery from the COVID-19 pandemic.

“Jason is an incredible leader, who will bring a unique blend of experience, expertise, and insight to the JUST board. We are beyond thrilled to welcome him to the organization,” shared JUST Capital CEO, Martin Whittaker.

“We’re thrilled to welcome Jason to our Board. His commitment to JUST’s mission of creating an economy that works for all and his expertise in leadership will be of great value to the organization in this period of growth and opportunity,” Laurel Britton, who chairs the Board’s Nominating and Governance Committee, said.

(Klaus Vedfelt – Getty Images)

In a new survey of 500 business leaders and 1,000 other members of the U.S. public, PwC found that in their roles as consumers and employees, respondents trust business more now than before the pandemic. And consumers, employees, and leaders agreed that the most important elements of trust right now are, in descending order: protecting data and cybersecurity, treating employees well, ethical business practices, and admitting to mistakes.

The report’s authors also noted that 88% of executives reported higher-than-normal turnover in recent weeks, which they tied to an increased demand for flexible work benefits and career growth opportunities, both of which have become much more attractive or necessary over the past year and a half.

As I discussed with Deepak Chopra during our incredible event yesterday honoring him as JUST’s first Chairman Emeritus, the future of the private sector’s role in our economy will be defined by whether businesses can truly create value for all their stakeholders. We look at a specific example of this in a new JUST article this week, examining how companies like Chipotle, Bank of America, and Hilton have developed recruiting and career development strategies for “opportunity youth,” 16-24 year olds disconnected from school and work. It’s one of many instances of companies linking their business goals with investment across stakeholders – in this case, filling entry-level positions while investing in communities where these companies operate.

As the trust premium grows, and with future ESG regulation looking more and more likely, the need to walk the talk and quantify this value creation process in a meaningful, transparent, and standardized way becomes evermore important. It’s why we are participating in the G7’s Impact Taskforce on the subject, and why we applaud efforts like Engine No. 1’s robust Total Value Framework, which also launched this week.

HP CEO Enrique Lores is one of those leaders at the forefront of this new era of business leadership, and I encourage you to sign up if you haven’t already for my discussion with him next week.

Be well,

Martin Whittaker

Amazon increases its starting wages to $18 an hour as it pushes to hire an additional 125,000 warehouse workers.

Cisco commits to net-zero greenhouse gas emissions by 2040.

HP, HPE, Intel, and Microsoft launch the HBCU Technology Conference to expand access to tech careers for students of color.

P&G aims to reach net-zero emissions across the company – and more importantly, its supply chain – by 2040.

Pepsi sets new goals to achieve net-zero emissions by 2040, become net water positive by 2030, cut virgin plastic by 50%, and more.

Verizon prices out its third $1 billion green bond, making the company one of the largest renewable energy buyers in the U.S.

Walmart issues its first green bond at $2 billion toward green investments in renewable energy, high performance buildings, sustainable transport, zero waste, water stewardship, and habitat restoration.

JUST Events

SEPTEMBER 21: Quarterly JUST Call with HP CEO Enrique Lores

Join us for the latest installment of the Quarterly JUST Call (QJC) with HP CEO Enrique Lores. HP is a JUST 100 company that under Lores’ leadership, has created value for shareholders while excelling on climate action, diversity and inclusion, and digital equity. JUST CEO Martin Whittaker will explore each of these areas with Lores, and, since it is timed with Climate Week, pay special attention to HP’s latest environmental sustainability efforts. Sign up for the Quarterly JUST Call here.

SEPTEMBER 21: Corporate Climate Commitments: Lessons from Goal Setting & its Intersection with the American Public: Recent news has highlighted the need for urgent action on climate, and about two in three Americans now believe corporations have a growing role to play in combating climate change. Join our Research team during Climate Week for a panel discussion about net-zero and science-based climate commitments at America’s largest corporations. Register to watch here.

What’s Happening at JUST

Worker Financial Wellness Initiative participants Chipotle, PayPal, and Prudential Financial joined the Aspen Institute to discuss how they’ve invested in their workers’ financial security. The Wall Street Journal’s Lauren Weber moderated the discussion, which highlighted how this work has impacted the companies’ bottom lines and what employers currently struggling to hire might take away from their efforts. Our Worker Financial Wellness Initiative was also featured by LinkedIn News, alongside posts from Martin, PayPal, and more.

We highlighted key ways everyday investors can make better ESG decisions, with the help of firms and financial advisors, following Lorraine Wilson’s conversation with Morningstar Global Head of Sustainability Research Jon Hale and Seeds’ Founder and CEO Zach Conway. Watch the conversation here.

(Chipotle)

“We see that the labor pool, and who knew this would happen even after the pandemic, that there’s a finite group of workers out there in the world. And so how can we go from always churning people to actually being in the business of creating talent for the future? So when we had big things like debt-free degrees as well as access to mental health benefits, when we wanted to introduce that, of course I would tell everybody ‘Make sure you have the business case.’ But, at the end of the day, if it’s aligned with the purpose of the company…it may get easy buy-in.”

“We believe this will make this process fair and respectful for every partner in Buffalo. It will ensure that all of you are afforded the voting rights, and the voice that you deserve in this process.”

“Paid family leave is something that our nonprofit partners are advocating for, making the child tax credit more permanent. Philanthropy is not just on the side of things, but it’s right in-line with how we do our business because it’s trying to change some of the structural issues…to get to the point where it’s not just about our own employees and customers.”

The Conference Board releases a comprehensive new report on CEO Pay at the Russell 3000 and S&P 500 showing how soaring stock prices bolstered pay in the last year. The EconomicPolicy Institute shares its latest analysis finding that CEO pay has skyrocketed 1,322% since 1978 and that CEOs were paid 351 times as much as a typical worker in 2020.

Engine No. 1 continues to make waves: Reuters reports on the group’s new Total Value Framework for investing that aims to tie company valuations to climate and societal impact.

The Washington Post reports that Harvard will officially divest entirely from fossil fuels, and explores what this means for a new wave of climate activism. The Verge reports that Jeff Bezos’ Earth Fund has pledged an additional $150 million to climate justice groups.

The Wall Street Journal deepens its investigation into failings at Facebook, including a look into the company’s own research into teen mental health issues as well as how misinformation, toxicity, and violent content increased after changes to its algorithm.

Refinitiv releases its annual Diversity & Inclusion Top 100, with Gap earning the top spot.

CNBC launches Equity and Opportunity, a new global brand that focuses on individuals and organizations leading the way on matters of diversity, equity, and inclusion.

This week’s chart comes from our latest polling report, showing how the pandemic has affected parents and caregivers, with 82% of respondents hearing of others, or personally experiencing, increased childcare costs throughout the last year and a half.

Ariel Investments co-CEO and President Mellody Hobson speaks at the Fortune Most Powerful Women Summit. (Paul Morigi/Getty Images)

Diversity, equity, and inclusion (DEI) has become an urgent item on the agendas of C-suites and boardrooms across corporate America over the past year. And, while there’s no shortage of commitments and interest from companies, data captured in our Corporate Racial Equity Tracker shows transparency and disclosure of progress against these pledges hasn’t kept pace.

But in light of the past year, demand from all stakeholders for companies to enhance their DEI commitment and boost transparency has continued to grow. Last week, Jean Case, CEO of Case Impact Network, and Mellody Hobson, co-CEO and President of Ariel Investments, joined JUST Chief Strategy Officer Alison Omens and CEO Martin Whittaker to discuss how companies should be meeting this moment, and adjusting their DEI strategies to deliver an inclusive recovery from the worst days of the pandemic.

Whittaker pointed out the gap between the “good stories” we tend to see from companies around DEI and actual results, and asked Hobson what she thinks the roadblocks companies that haven’t been as transparent are facing. To her, it comes down to two reasons – both rooted in fear. The first being fear of legal liability – which would be more of a threat when there is lack of specificity or transparency – and the second being fear of vulnerability.

She stressed how ingrained the idea of vulnerability as weakness is in our society and that, for CEOs and other corporate leaders, it ultimately leads to not sharing updates on DEI efforts until goals are met – if they are actually met. “We have this, this invincibility or this perfection that then makes someone very, very reticent to admit that they can’t do something or pull it off or that they’ve failed at something,” Hobson said.

These are challenges that have been historically embedded in corporate culture but, she explained, companies can overcome them by using their failures as motivation, and shifting ownership of DEI work to those in positions of power. To Hobson, these steps can both help them get comfortable with admitting where they’re starting from and, ultimately, reach their DEI targets.

A board director at JPMorgan Chase, Hobson shared how CEO Jamie Dimon used the company’s historical failure to promote Black employees through its ranks as motivation for change. Shortly after joining the board, she recalled that Dimon was upfront about how unhappy he was with the bank’s numbers around advancement for Black employees. Hobson noted being taken back at first, as she wasn’t used to hearing executives admit to something not being good enough. Dimon pointed to the numbers, which were poor at the time, and called on the whole company to make raising them an imperative.

With that, Hobson said, it took on the same level of urgency as the success of the rest of the business. Accepting and acknowledging this failure gave JPMorgan the added incentive to take action. And while the company knew “it wasn’t going to happen in 10 minutes,” the willingness to admit the problem made it a goal as important as any other high-level business outcome – and one it couldn’t claim to have met without the data to back it up, she emphasized.

In addition to embracing failure as a means of motivation to reach DEI targets, Hobson wants companies to think about who’s taking ownership of this work. It’s clear that this is no longer a nice-to-have for any business, Hobson said, and yet we’re still seeing it siloed and not clearly tied to business outcomes. She sees this as a matter of who’s tasked with this work.

Women and people of color are often carrying the brunt of DEI efforts while being underrepresented in senior leadership positions. She pointed to the success of the 30% Club in the United Kingdom, which relied upon men in the country’s C-suite advocating for women to fill empty board seats, as one way to shifting the ownership of this work can pay off, especially when it is made a priority worth competing over.

But, Hobson said, those in leadership positions should think about the skills they need to carry DEI work forward. She brought up reverse mentorship as an example of how executives could tweak a potential pre-existing DEI initiative to help better prepare leadership to engage in these efforts. She’s seen growth in corporate leaders “talking about how they want to mentor women or they want to mentor minorities,” but she wants them to take it a step further.

“You need as much mentoring around these issues of gender and race as they may need around business skills,” Hobson said. “That, again, is inclusion. It’s participatory. It’s a two-way street.”

Catch up on last week’s full conversation below to hear more from Hobson and Case on what companies should be considering at this crucial point for action on racial and gender equity.

Over a year into the nation’s reckoning with racial injustice, corporate America is experiencing a reckoning of its own. Companies that rushed to make pledges to advance racial equity last summer are now seeing their commitment put to the test. There’s concern that momentum is fleeting and “diversity fatigue” is setting in.

At the same time, Americans want to see more – with 83% of Black Americans and 64% of Americans overall believing that corporate America has more work to do to achieve racial equity. The private sector is taking steps in the right direction. Disclosure of EEO-1 and other workforce and board data is trending upward. Shareholders are increasingly holding companies to account. But Ariel Investments co-CEO and President and Starbucks Chair, Mellody Hobson, doesn’t want companies patting themselves on the back for “stepping over such low bars” yet.

“We can’t feel like this is tremendous progress because suddenly there are three Black women that have risen to some ranks in corporate America,” she said, referring to Roz Brewer and Thasunda Brown Duckett joining Ursula Burns as the only Black women to have run Fortune 500 companies. “Tremendous breakthrough on the one hand. On the other hand, definitely not good enough.”

We’re seeing this stalling of progress unfold in real-time with women and workers of color being left out of the beginnings of an economic recovery. Hobson and Jean Case, CEO of Case Impact Network and Chairman of the National Geographic Society, sat down with JUST CEO Martin Whittaker and Chief Strategy Officer Alison Omens to discuss how companies can address this through changing their approach to diversity, equity, and inclusion (DEI).

Watch the full conversation below and explore our key takeaways.

There’s no shortage of research making the business case for DEI. For Case and Hobson, it’s time companies leaned into this argument and treated DEI as a business outcome. Case pointed to the fact that the firms that are the C-suite’s go-tos for consulting are the ones putting out this research and yet, companies aren’t capitalizing on its economic value. Diversity is not philanthropy, Hobson said, and made the point that, when companies look at it through a more metric and outcome-oriented lens it will ultimately lead to greater transparency. “We need that same intentionality. We need the same kind of incentives. And we need that same level of accountability when it comes to race and gender.”

A board director at JPMorgan Chase, Hobson shared how CEO Jamie Dimon was upfront about the bank’s poor numbers around advancement for Black employees and committed to bringing them up. With that, it took on the same level of urgency as the success of the business. Both Hobson and Case want to see companies operating with that outcomes-driven mindset, following examples like that of Merck’s detailed DEI reporting to go beyond intention to act on racial and gender equity. “People want credit for intent as opposed to outcomes. That is problematic,” Hobson said.

When companies treat DEI as a business outcome, Case and Hobson stressed it’s easier for it to be treated as a core value. “The board is the boss,” Hobson said. And, once the board sees DEI as key to the company’s success, the impact of this work will last beyond the tenure of one CEO. At Ariel Investments, that’s manifested in an approach Hobson refers to as the “Three Ps”: People, Purchasing, and Philanthropy. She raised how McDonald’s has built long-standing relationships with Black, brown and women-owned businesses through its purchasing practices, proving “the power of process over personality.”

Case touched upon how important institutionalizing DEI is as the pandemic continues to put added strain on working parents. With employers looking to re-open offices, she wants to see policies designed to meet working parents where they are – like Merck’s Re-Invent Program, built to help professionals reenter the workforce after two or more years. While the burden over the last year has fallen more heavily on mothers, Case thinks the key to de-stigmatizing working as a parent is both for men to be more vocal and for them to be seen as parents.

“It’s on all of us, and I’m particularly talking to the men, who are leaders and executives to make it clear that they too are parents and to be a little transparent about what all parents need and that it’s not exclusively a working moms issue,” she said.

Hobson sees the need for those in leadership to champion all DEI work – a burden that too often falls to those these programs are designed to help. But she first wants corporate leaders to acknowledge the very real difference in the “‘line” used to measure performance for workers from marginalized groups. “It moves all the time for Black people, brown people, people with different sexual orientations, women,” she said. She shared that, more than once, while in meetings with her co-CEO and JUST Board Member, John Rogers, she’s had people not look her in the eye.

Hobson wants executives to see this, and also use the power and privilege they have to take on this work. She brought up the success of the 30% Club in the United Kingdom, surpassing its target of securing at least 30% of seats on FTSE 350 boards for women in less than a decade. Helena Morrissey, the campaign’s founder, told Hobson it came down to her approaching influential businessmen in the U.K. and tasking them with adding women to the boards they sat on, and had sway over. Ultimately, Hobson sees this as key to avoiding diversity fatigue and the burden women and workers of color feel having to shoulder this work.

As the pressure for companies to follow through on their DEI commitments intensifies, Hobson made the simple, but important point: “Don’t say it if you don’t mean it.” To her, everyone is an activist – employees especially. Companies should expect to be held accountable by their stakeholders, and plan accordingly. Case brought up the rise in shareholder activism on DEI that no company can afford to ignore. CEOs are going to have to pay attention when board members are being voted out, she said.

Case also stressed that startups should be taking this work seriously. While the numbers around venture funding are dire, she said, seeing listing requirements from Nasdaq and Goldman Sachs sends a clear signal to “companies who dream of IPO-ing, what they have to get together before they IPO.”

Whether companies are at day one or have made headway, Hobson wants them to keep one question in mind: Who’s not at the table? She urged leaders, white men in particular, to think about what it feels like, as a woman or a person of color, to walk into a room and be surrounded by only white or male colleagues.

“I am asking people every time they walk into a room to put that lens on so then they can see what is missing in the room,” Hobson said. “And to the extent that people are walking into rooms and see that, I think that we can start changing this conversation and really elevating this idea of what diversity and real inclusion look like.”

The relationship between corporate America and Washington D.C. has always been a topic of debate in the U.S. – and in recent years, we’ve seen the conversation center around issues from adjusting tax rates to working together in the fight against COVID-19. A recent Forbes piece on corporate lobbying points to the old adage – “If you are not at the table, you’re on the menu” – impressing the important role companies can play in influencing legislation on economic and social issues, something the American public also confirmed in our latest survey. Survey research continues to confirm that Americans are increasingly looking to CEOs to be societal leaders, and they trust business more and more to address the big issues, from inequality to climate change.

Yet the question between companies’ leadership overall, and their engagement with government and government-adjacent organizations, remains blurry. Trade associations, also known as industry associations, are an integral part of the corporate lobbying conversation. A trade association is an organization founded and funded by businesses, typically grouped by industry, for the purpose of collaboration, lobbying, education, and advertising, as well as to promote the group’s views to government entities. Trade associations are uniquely positioned to exert political influence with in-depth policy knowledge, political connections, and the influence of a large corporate membership. We know that companies rely heavily on trade associations to advance their priorities, and yet trade associations can advance issues that may be antithetical to their stated stakeholder-capitalism priorities.

Funded mostly by corporate membership fees and non-deductible contributions from their members, trade associations can use this funding for general lobbying-related expenses. Companies also have the ability to pay the trade association in the form of a non-deductible contribution to direct a lobby campaign in their interest. The strength of trade associations should not be underestimated, as their support for or opposition to policy issues is closely followed.

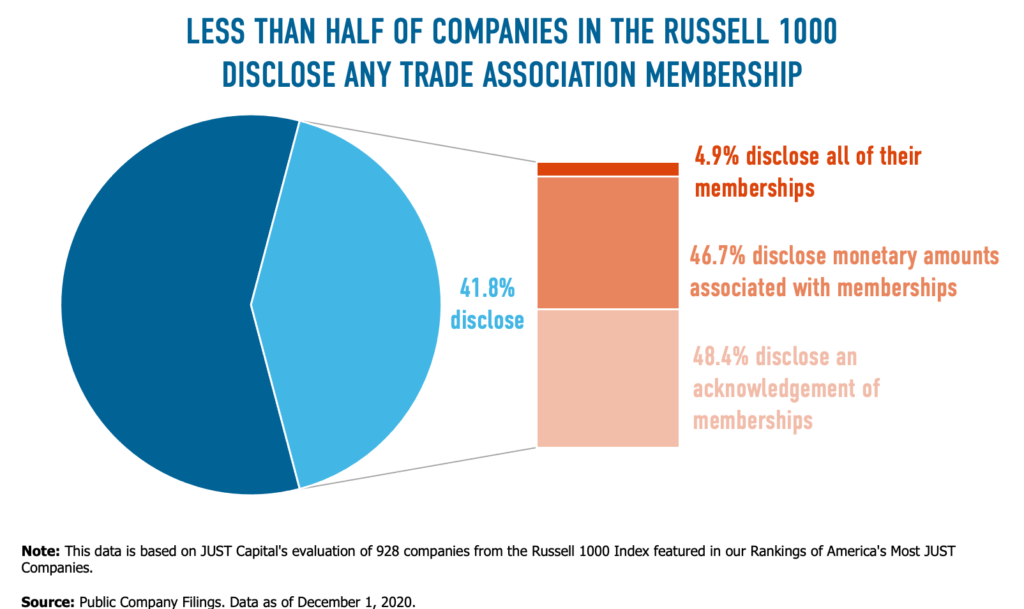

Currently, there is no mandate for companies to disclose their trade association memberships, or for the trade associations to disclose their members, so JUST Capital decided to look at the state of disclosure, as transparency on this issue provides stakeholders with another tool to understand if companies are following through on or possibly undermining their ESG commitments through the trade associations’ approach.

When looking at the 928 publicly traded companies from our 2021 Rankings, we find that 58.3% do not disclose any of their trade association memberships. Of the 41.7% of companies that do disclose trade association memberships, the vast majority provide general disclosures – an acknowledgement of their memberships – but not necessarily an exhaustive list with specific details. Only 46.7% of the companies that disclose these general memberships also make mention of their monetary contributions and just 4.9% explicitly state that they’ve disclosed a full – rather than selected – list of trade association affiliations, in addition to their monetary disclosure.

Controlling for industry and revenue, we find that all three levels of disclosure mentioned above correlate strongly with a higher level of performance in JUST Capital’s annual Rankings across each of the five stakeholder groups – workers, customers, communities, shareholders, and the environment. Accordingly, companies that score higher in JUST Capital’s overall Rankings tend to disclose more than their peers.

When collecting this data, we found that these disclosures are often tucked inside governance documents on investor sites or on a hard-to-find public policy/engagement webpage, making the disclosures generally less accessible. The ways that these disclosures are ultimately displayed also varied greatly. For example, Intel has a separate section in their Corporate Responsibility Report Builder with the option to download a list of the company’s political contributions, trade association memberships, and associated membership dues. Aggregating this disclosure along with Intel’s other ESG disclosures shows its commitment to transparency on this as an ESG-related issue. BlackRock’s disclosure specifically notes that these memberships are periodically reviewed to ensure they align with BlackRock’s views on material public policy issues. A robust monetary disclosure from Tractor Supply breaks out what portion of monetary contributions went to lobbying.

As stakeholders continue to expect greater transparency, this is an area that companies may want to review to better understand their approach to government relations alongside their overall approach to supporting their stakeholders. Companies can ensure alignment with their membership to these organizations and all of their viewpoints before contributing to them. In addition, the American public and investors will want to know whether companies are taking one step forward or two steps back through their trade association memberships, or if they are walking the walk in every aspect possible.

The data and analysis in this piece were collected and run in December 2020.