Happy Friday. This is Alison Omens, JUST Capital’s Chief Strategy Officer, filling in for Martin as he takes a much-deserved break.

One notable change since 2020 is how many worker-related issues now end up in the headlines. This week is no different, from the United Auto Workers strike, actor and writers’ strike, quiet quitting (did you see this week’s Fortune headline on grumpy stayers?), to the both practical and philosophical debate over workplace flexibility and return to office mandates. Zoom caught our eye this week for their return-to-office mandate (and AI privacy gaffe).

With the future of work so up in the air, there’s a real opportunity for businesses to capture significant value from investing in their workers. I was recently looking up a Gallup number I hear so frequently at business leadership and jobs conferences. You know which one I mean. Only 32% of workers are engaged at work, which costs the economy $8.8 trillion a year, and according to one estimate, costs businesses about a third of a worker’s annual salary. Here’s a number I hadn’t heard – Gallup also estimates that best-practice organizations (who focus on engagement, transparency, management) see 72% engagement – a 40 point differential!

The co-founder of Slack’s Future Forum wrote in Charter this week that our old way of thinking about effective work (which is driving the return-to-work debate), including metrics of employee productivity – from hours logged to even revenue-per-employee – isn’t cutting it anymore. It’s blunt-object management that’s not focused on outcomes. On another hot topic, some experts including JUST’s former board member Sharon Block, see worker activism, including union activism, as a sign of employee engagement (see her recent piece in Harvard Business Review for details).

I’d like to pose a question for all business leaders to consider: Instead of seeing worker issues as a risk to be managed – what might it look like to consider their workforce as a tool to drive lasting competitive advantage? And engagement of any kind as a sign of that success?

Now, no one is saying operating like this is easy. Managers have to be trained and ready to create workplaces that don’t just function but thrive.

But make no mistake: Regardless of industry, workers are asking more of their employers in a way that hasn’t been seen in a long time. People’s expectations are higher. At JUST Capital, our research shows that worker issues consistently rank the highest among all business priorities. And our data shows that companies that rank highest in terms of worker issues consistently outperform the Russell 1000. Listening to workers and prioritizing their career success benefits shareholders. There’s ample research supporting this.

If this resonates with you, I encourage you to explore JUST Capital’s framework, specifically the Worker Financial Wellness Initiative, where we work with CEOs, HR leaders, and other executives to help businesses understand the financial health of their workforce.

Have a great weekend,

Alison

Fortune’s Alan Murray spotlights our new research report in CEO Daily discussing four companies leading on women representation across workforce, board, and suppliers – Citigroup, Accenture, General Mills, and The Hartford. Check out the full analysis here.

JUST Capital sits down with Syndio CEO Maria Colacurcio for an informative conversation on pay equity policies amid growing political pressure against diversity, how AI will impact HR, and more.

PolicyLink, FSG, and JUST Capital have teamed up to develop corporate standards that will provide companies with the actionable guidance they need to deepen their commitment to racial and economic equity. To stay up to date on the latest news and ways to get involved, sign up for the new Corporate Racial Equity Alliance newsletter and read the latest issue here.

JUST Advisor Paul Rissman pens an editorial for As You Sow’s new Investing ESG website titled “House Hearings to Deny Climate Risk Heat Up Even as World Burns.”

(Syndio)

“I think a lot of folks started immediately presuming that the Supreme Court’s recent ruling would cause a big rollback in diversity practices … But in the wake of salary transparency laws, and a competitive talent market, which continues even amidst all the news of layoffs, we’re seeing a lot of companies doubling down on [pay equity]. I think part of that is because folks realize there’s no going back to the old way. This generation of employees expects companies to pay equitably.”

Zoom announces new terms of service that alarm customers as they have allowed the business to use images, sound, and other content from meetings hosted on the platform to train its AI algorithm. The company’s CEO apologized, but it hasn’t quelled the outcry.

Sidley publishes an article breaking down how boards of directors should approach AI and understand the strategies, risks, and potential compliance issues involved with the new technology.

Disney will commission an AI task force aimed at reducing inefficiencies across the media and entertainment giant. Reuters has the story.

OpenAI launches a media grant in collaboration with NYU’s Arthur L. Carter Journalism Institute, which will fund a journalism ethics initiative focused on how to cover the 2024 election in light of disinformation and polarization, as well as explore the best way to diversify newsrooms and cover marginalized communities.

When the man that wrote the book on “Woke Inc.” says the frame is “in his rearview mirror,” perhaps political tides are turning. The New York Times shares Republican voters are less in favor of a candidate whose top priority is battling “wokeness” versus one who is focused on law and order issues. Politico reports on Ron DeSantis’ failure to reach striking distance of the GOP nomination as he doubles down on his “anti-woke” strategy and Alan Murray writing for Fortune thinks Vivek Ramaswamy might have overestimated how much voters care about “woke CEOs.”

The Conference Board releases insights on how companies can position themselves to weather the current ESG backlash and use it as a chance to solidify their stance on stakeholder issues.

S&P Global halts numbered ESG ratings, reverting to text-only analysis for investors. Meanwhile, competitor Moody’s will continue to rate ESG criteria on a one to five scale.

In the wake of a new $30 billion union deal, job searches for open positions at UPS have spiked. Starting wages for part-time workers increased to $21 an hour and other accommodations were all included in the agreement.

Fortune’s CHRO Daily Newsletter shares a new poll that found 51% of for-profit and nonprofit firms believe retaining talent is a top operational priority.

CNBC highlights Amazon’s partnership with Maven Clinic, the first female-focused health startup valued over $1 billion. The agreement will provide reproductive health services for 1 million employees.

Bloomberg writes about the state of share buybacks as companies put profits back into their businesses rather than offering it up to investors. Net repurchases plunged 36% from a year ago among S&P 500 firms that announced financial results.

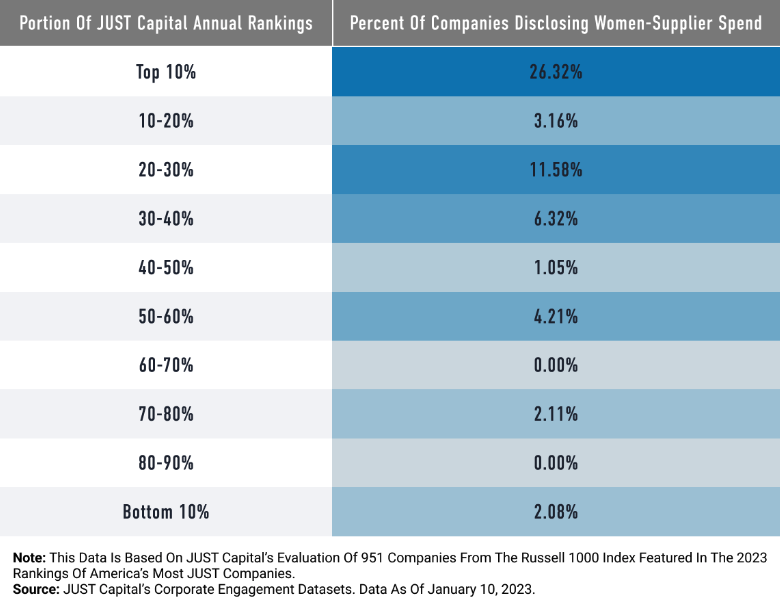

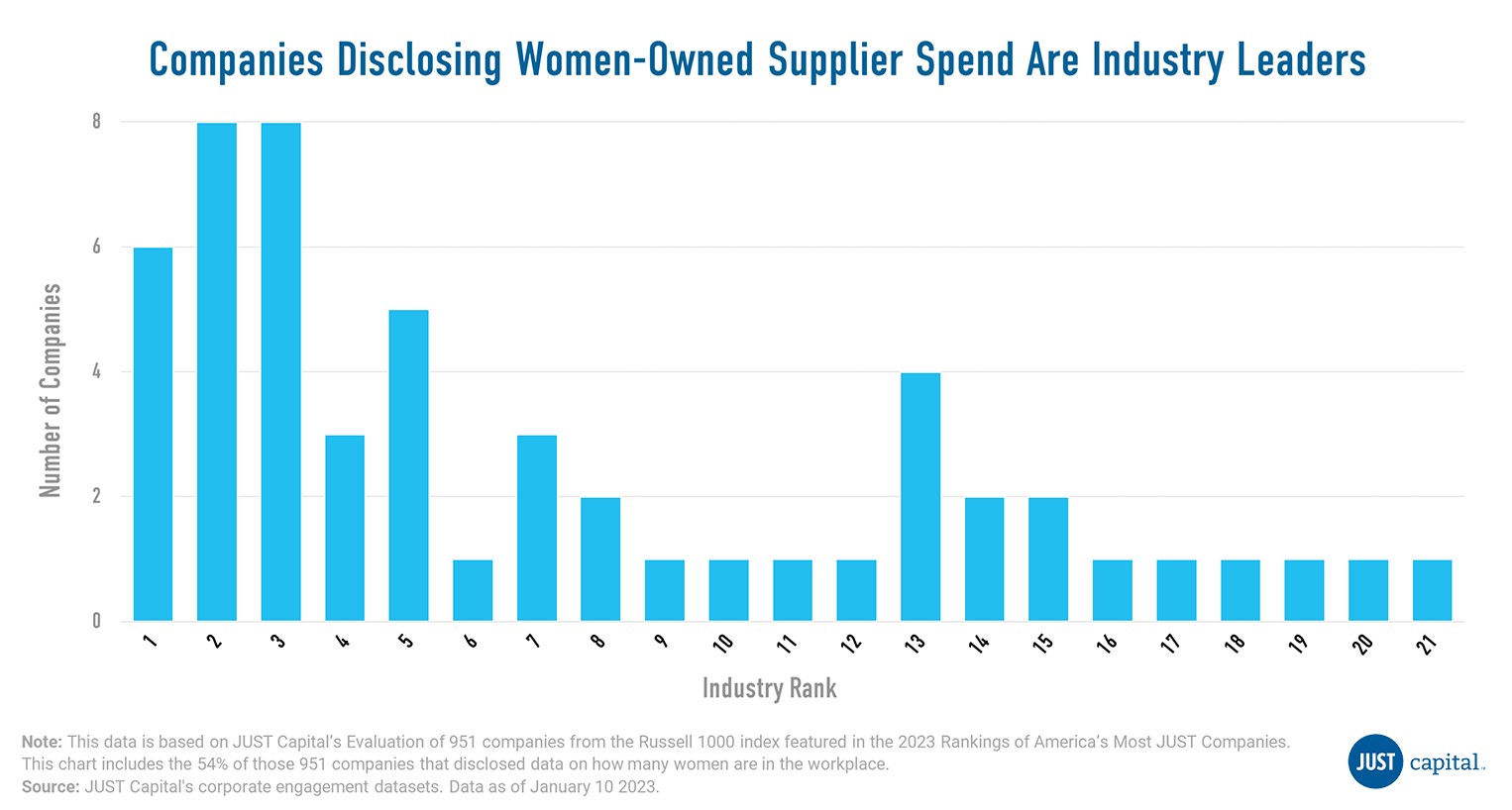

In conjunction with our recent article on gender diversity, we’re highlighting data that shows how more just companies are leading the way with disclosing how much they spend with diverse suppliers. Out of the 54 companies that disclosed spend on women-owned supplier businesses, companies in the top decile were also most likely to have disclosed, and 53% of all companies who disclosed their spend on women-owned suppliers were represented in the top 20% of JUST Capital’s Rankings.

This report was co-authored by Rachael Doubledee and Daniel Krasner.

Today, when it comes to disclosing comprehensive data around gender when it comes to workers, board members, and suppliers, the results are varied. Of the 951 Russell 1000 companies that JUST Capital analyzed and ranked in 2023, approximately 79% disclosed data on how many women are in the workplace, 99% reported having at least one woman on their board, but only 5.6% disclosed spending on women-owned businesses

In combing through different company data and policy disclosures, JUST Capital identified four companies leading the pack in terms of publishing data around women in their workforces, on their boards, and with women-owned businesses in their supply chains – Citigroup, Accenture, General Mills, and The Hartford. These leaders are also innovating on programs to increase those numbers. Each had women representation in their workforce at or near 50%, had above 40% women representation on their boards, and disclosed how much they spend with women-owned suppliers.

During the pandemic, women were more vulnerable to layoffs than men, were more likely to work in industries that suffered (hospitality, service sector), and were more likely to exit the workforce to care for their families.

But economic data shows a promising turning point. Women’s current labor force participation — that is, the percentage of women working or looking for work — is around 57.4% as of July 2023, almost back to the February 2020 number, 57.9%, per February government data.

Building a more resilient economy means building inclusion across industries for women, and makes the economy stronger and better able to weather future crises. According to JUST Capital polling, most Americans believe that women leaving the labor force is bad for the economy (66%), and bad for women’s equality (59%). JUST’s recent work on promoting inclusion in the workplace has also focused on the policies and practices that companies can and should implement including supporting paid family leave and equal pay.

In a 2022 analysis, JUST found that the share of companies publicly disclosing workforce demographic data by race, ethnicity, and gender by standardized job categories in their EEO-1 Report – the gold standard for workforce demographic disclosure – or similar intersectional data has more than tripled between 2021 and 2022, from 11% to 34%. Companies with 100 or more employees are already legally required to submit these reports to the U.S. Equal Opportunity Commission and Department of Labor, meaning that the data has already been collected, but not all companies make it publicly available. For example, 79% of the Russell 1000 disclose women’s representation within their workforce, but 21% do not. In a companion analysis exploring the business and investor case for increased disclosure, we found that the companies that disclose EEO-1 or similar intersectional data outperform those that don’t by 7.9% over the trailing one-year period ending in 2022.

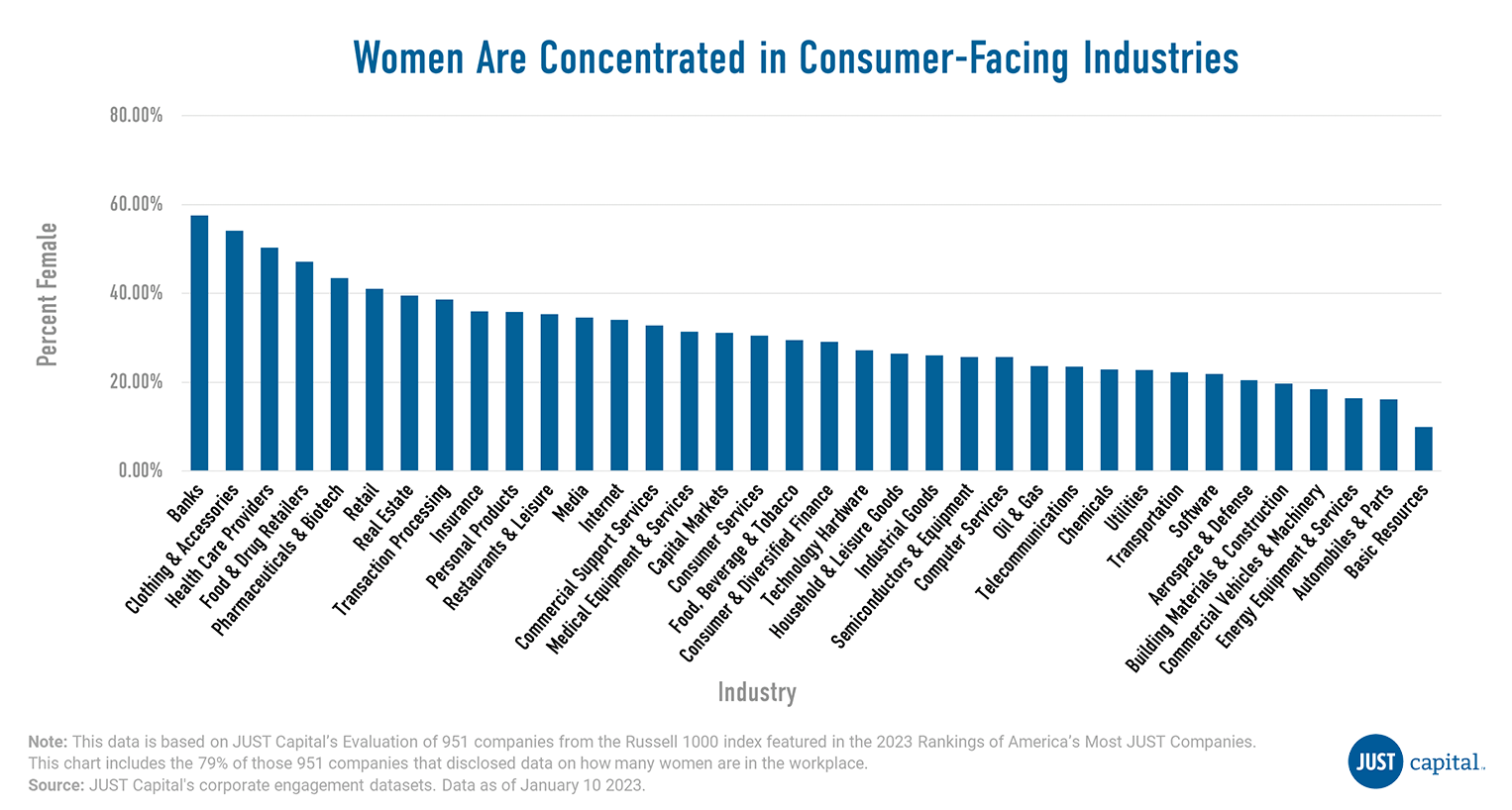

Women have historically turned to customer-facing industries with more flexible hourly roles like accommodation, retail, and food services to meet the dual demands of work and caregiving. These industries were some of the most vulnerable to pandemic job losses. Our own analysis of companies in the Russell 1000 that disclosed workforce data demonstrated higher female representation persists in industries like clothing and accessories, and lower representation remains in industries related to energy and technology.

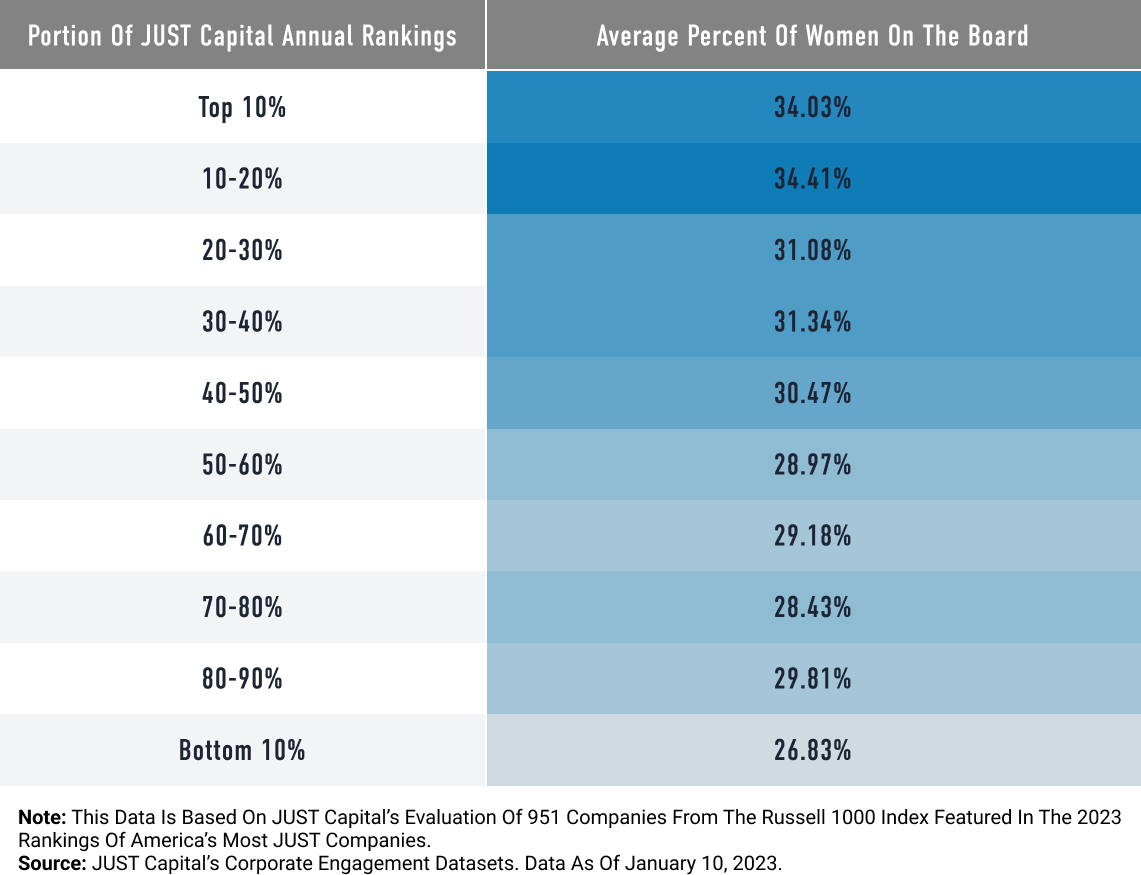

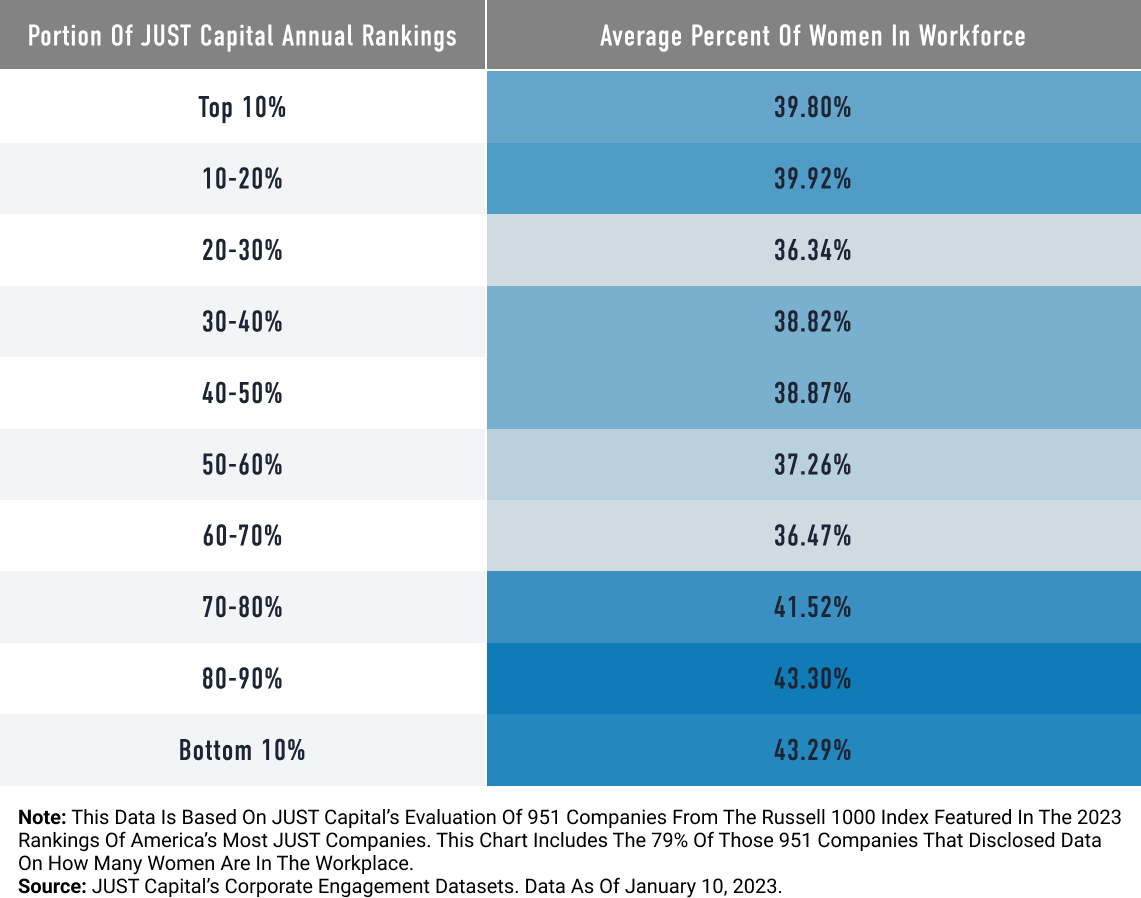

Company data within each decile shows that higher representation is taking place at the top of our rankings in board diversity. On average, the higher one’s rank, the higher one’s percent women on boards. Out of the 54 companies that disclosed spend on women-owned supplier businesses, companies in the top decile were also most likely to have disclosed, and 53% of all companies who disclosed their spend on women-owned suppliers were represented in the top 20% of JUST Capital’s rankings.

For the workforce, trends aren’t as clear. Women’s average representation varies slightly between 36.47% and 43.3% throughout the rankings. At first thought, industry could be a driver for further analysis; for example, if industries with higher representation of women in the workforce are ranking lower, that could explain the slight variation. But upon evaluation of where companies aren’t disclosing, a likely driver is that the slightly higher percentages at the bottom of the ranking are due to companies not disclosing their workforce.

In the top 10%, only 1 company does not disclose its representation of women in the workforce, while at the bottom 10%, 42 companies do not disclose, contributing to the seemingly higher representation of women in the bottom 10% of the rankings. With less companies disclosing, there are less inputs when averaging. This is why no matter the level of female representation in the workforce, it is imperative companies disclose the demographics of their workforce for us to fully understand the breadth of women’s representation in Russell 1000 companies.

The four leaders in our analysis all had women representation in their workforce at or near 50%, had above 40% women representation on their boards, and disclosed spending with women-owned suppliers. Here are additional details on how they are advancing more comprehensive policies and practices:

As part of its Global Diversity Strategy, Citigroup has made bold strides in addressing women representation through hiring, promoting from within, and retention strategies with 53% women representation. As part of the 30% Club, Citigroup has outperformed many of its peers in the banking industry, and discloses 50% women board representation.

Citigroup stands out from peers in its supplier practices, including increasing supplier capacity, supplier-business mentorship, and supplier engagement, many of which are women-specific initiatives. In 2021, Citigroup spent $172M with Tier 1 Women-Owned Suppliers. In 2020, Citi set a goal to increase spending with certified diverse suppliers to $1 billion annually.

Accenture provides detailed disclosure of women representation across its operations and at varied levels within the organization. With women representing 50% of the board of directors, and 47% of their workforce, Accenture stands out as the only company in its industry with Board parity by gender.

Accenture leverages its supply chain to support its efforts to achieve gender parity. In FY21, it spent $95,194 with women-owned suppliers – about 18% of its total diverse supplier spending. Accenture is also invested in supplier success, and it outlines global efforts to engage and support women suppliers.

General Mills discloses high women board representation for its industry at 45%, and clearly discloses 50% workforce representation for women. It also provides a disaggregated view of women’s representation at multiple levels of seniority (Officer, Director, Manager, etc.) throughout the company.

It has disclosed spending of $122.9M on women-owned suppliers and has set time bound targets and goals to increase diverse supplier spending. Importantly, General Mills is focused on increasing certification for diverse suppliers through funding and consulting support. This process can be laborious and expensive and is important in consideration of problems with access to capital often faced by women and minority-owned businesses.

The Hartford clearly discloses board women representation at 40%, a standout in the insurance industry. Workforce representation is not unusual in the industry, but is disclosed at 61% women. It has also disclosed spending $15M with women-owned suppliers and provided an update on their pay equity goals.

The Hartford has robust supplier practices, including engagement with diverse suppliers to increase bid success rate, transparent disclosure of supplier industries, and disaggregated supplier categories and the spend associated. The level of detail allows them to estimate job multipliers to track direct and indirect job creation and impact in communities.

While these four companies stood out within their industries in terms of gender diversity, companies should do more to illustrate their commitment to closing the gap in women representation in boards, the workforce, and supply chains. We wanted to call special attention to the subject of diverse supplier spending. Each of the four companies demonstrated the following areas as best practices:

1. What and how much. Disclose how much spend is attached to each category of diverse supplier (e.g., women, veteran, minority, small/local business), Supplier Tier, and an overall Supplier Spend Amount. See Accenture, General Mills (page 54).

2. Community impact. Track supplier industry to estimate local impact factors and demonstrate community impact, as well as support of high and low wage industries. See The Hartford.

3. Equitable engagement. Detail a supplier engagement strategy that is easy to understand, and reduces certification cost pressures on suppliers who often have access to less capital, such as women-owned businesses. See Citi and General Mills (page 54).

4. Progress evaluation roadmap. Set milestones, and evaluate progress frequently and clearly with planned and easy to follow updates on progress and challenges to reaching goals. See Citi.

Additionally, we found that many of those leading their industry rankings were well positioned to demonstrate best practices to their peers in disclosure practices. Of the 54 companies that disclosed their spending on women-owned businesses, 69% ranked in the top 10 in their respective industry rankings.

Women’s representation in business leadership and the country’s overall workforce is an important issue to the American public. To demonstrate their commitment, more companies should go beyond public statements and select statistics, and demonstrate leadership through action, follow-through, and greater transparency through reporting.

To unpack your company’s gender equity performance in the 2023 Rankings and gain insights into how to improve on the issues that matter most to the American public, please reach out to corpengage@justcapital.com.

I recently had the pleasure of interviewing former Sprint CEO and JUST Capital Board member Dan Hesse about the importance of purpose-driven human leadership in business.

During the discussion, Dan – whose career spans five decades, from executive at AT&T, to Sprint, and now Board Chair of Akamai Technologies and Director of PNC Bank – recounted that when he became Sprint’s President and CEO in 2007, the company’s business plan had it filing for bankruptcy in six months. He had another plan. Over the next seven years, Sprint went “from hugely negative total shareholder return to the best total shareholder return of any big company in the U.S.,” he said. The key to the company’s success? Investing in a strong organizational culture from the top down and treating employees well. You can check out the highlights of the interview here.

It’s a refrain I hear a lot from the CEOs, executives and corporate directors I’m fortunate enough to talk to. Andrew Liveris, former 14-year CEO of Dow Chemical, just wrote a book on the subject, “Leading Through Disruption,” noting how the demands on business leaders today are becoming at once more complex and more challenging. Pete Stavros’ “Ownership Works” is turning it into a powerful business leadership philosophy, and McKinsey’s Re:think newsletter this week similarly showcased how companies can drive performance transformations at scale by listening to workers’ insights. Another JUST advisor, Hubert Joly, whose book “The Heart of Business” details the leadership principles he deployed to drive a purpose-led turnaround at Best Buy, lectures on the subject at Harvard Business School. And in private internal meetings, JUST board members including Grameen America CEO Andrea Jung and former EY CEO Mark Weinberger routinely stress the importance of purpose, of understanding your “why” – and that of others whose views you may oppose – as being key to leadership success.

Amid the very real pressures to deliver results, avoid PR missteps, and keep myriad stakeholders happy, it’s easy to forget all this. The fact is that in an era where Americans trust company leaders more than any other actor to lead, authentic human leadership in business is more important than ever.

Be well,

Martin

In the wake of the Supreme Court’s decision on affirmative action, corporate America is walking a tightrope on DEI. In a new Fortune editorial, JUST’s Director of Equity Initiatives Ashley Marchand Orme and Managing Director and Head of Corporate Impact Tolu Lawrence highlight the investor case for DEI initiatives. They point to our DEI Leaders Index Concepts that found the top 20% of JUST’s Rankings on DEI Issues outperformed the Russell 1000 Cap Weighted benchmark by 0.19% and Russell 1000 Equal Weighted benchmark by 3.4% since its inception on Dec. 31, 2021.

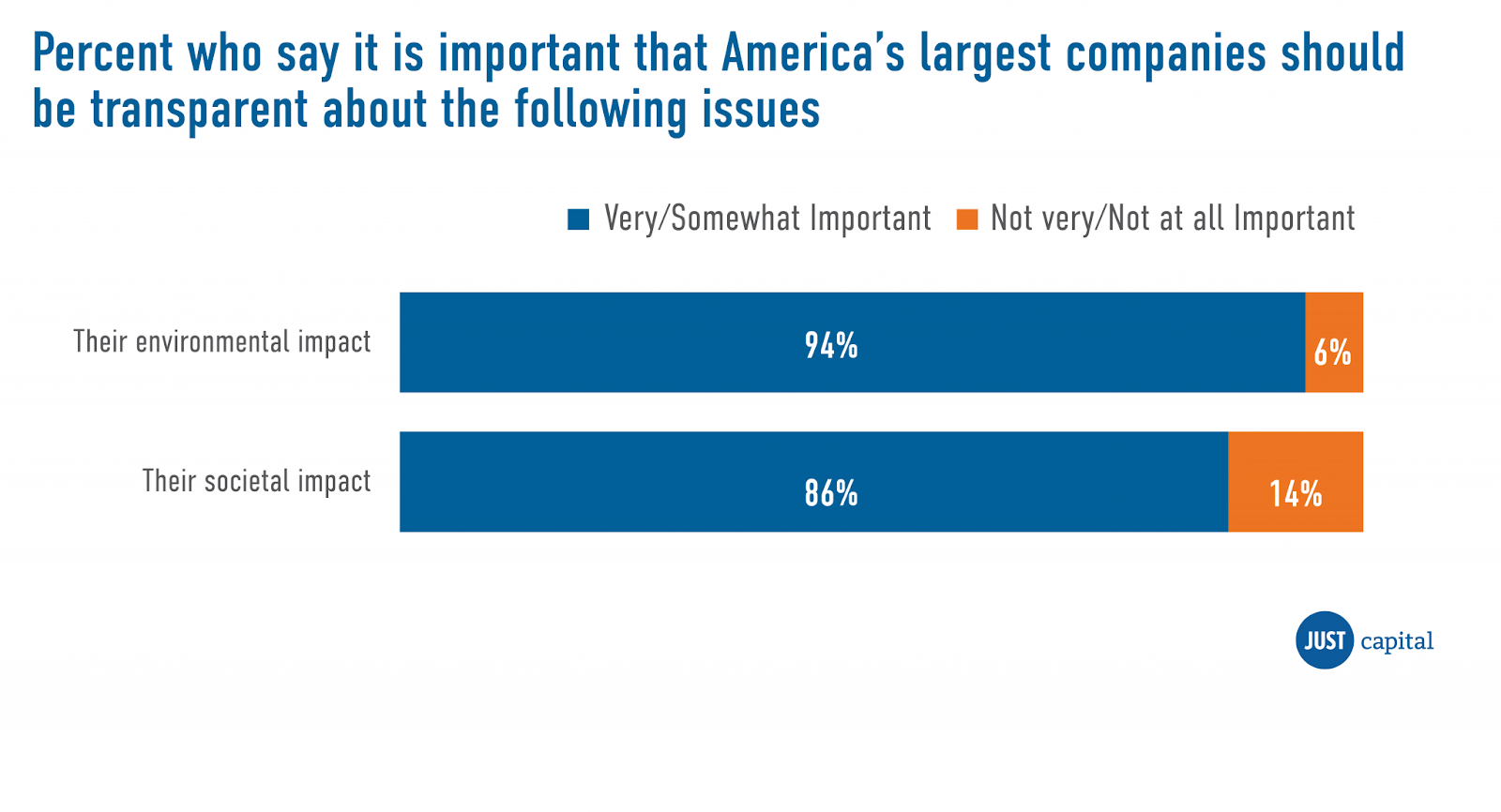

Thought leaders from the JUST Corporate Impact team – Senior Research Manager Rachel Doubledee, Director of Workforce Initiatives Kelly-Frances Fenelon, and Director of Research Insights Matthew Nestler – author a piece in the latest edition of Amplify, Cutter Consortium’s monthly journal on key business and technology issues. The article makes the case for increased corporate disclosure, bringing together what we’ve learned from the public on how they perceive and prioritize corporate transparency, as well as our analysis of disclosure at America’s largest companies.

Forbes features JUST Capital polling research tracking the American public’s top priorities, specifically their stance on climate justice. “The estimated probability that a random respondent would rank ‘combats global climate change by reducing its own emissions’ as a corporate priority is 2.6 percent. Instead, the probability that respondents would judge a worker-related issue as the most important aspect of ‘just’ corporate behavior is 44%.”

(Image Credit: Akamai Technologies)

“If you serve all stakeholders, your reputation improves, your customer base improves, employee productivity and retention improve. People talk about shareholder capitalism vs. stakeholder capitalism. They’re very symbiotic. But the CEOs who think in stakeholder terms achieve the highest shareholder results.”

JP Morgan Chase, Capital One, and Wells Fargo lead the race to make banking an AI-first industry. The three are among the North American banks outpacing their global peers with the region’s banks publishing 80% of all bank AI research and making 60% of all bank AI-related investments in 2022, while filing 99% of all the AI-related bank patents in 2021.

Fortune’s CHRO Daily Newsletter explores the ways AI will positively impact HR work, from payroll to hiring, even as CEOs are skeptical of the technology’s applications.

What is the best way to use ChatGPT? A new opinion piece in Fortune argues we should reconceptualize the tool as a “glider” with which we can navigate the possibilities of knowledge rather than a search tool that provides answers.

Bloomberg reports that conservative efforts to tamp down on ESG during a month of hearings in July failed to produce results by materializing into legislation or swaying investor behavior.

In a post-earnings interview with Fortune, Chipotle’s CFO attributes strong growth to its people and shared that the company will be spending $2.5 billion on salaries, bonuses, and benefits for its restaurant workers. “What we will do is make sure we invest in our people.” Hear firsthand from a Chipotle employee who’s benefited from these investments in our Worker Financial Wellness Initiative video feature.

A new opinion piece from McKinsey discusses the ways companies can adapt and innovate by taking worker insights into account.

NPR reflects on the stagnation of the federal minimum wage. It’s been 14 years since the number was raised.

Women now hold 33.3% of board seats among S&P 500 companies and represent a record 41 CEO positions even as DEI initiatives come under some scrutiny. Bloomberg has the story.

HR Drive shares a new study that found formerly incarcerated employees do not pose an outsized liability risk to companies. Research conducted by The Legal Action Center hopes to allay employer fears and help break the cycle of recidivism.

New U.S. labor market data shared by Axios points towards a possible “soft landing” as job openings and unemployment balance out.

In conjunction with our team’s latest piece on corporate disclosure featured in Cutter Consortium’s Amplify journal, we’re re-upping a key chart from a 2022 survey we conducted in collaboration with Public Citizen and Ceres, to better understand Americans’ views on the need for greater transparency in business. We found that strong majorities of Americans agreed that companies should disclose details on both their environmental impact (94%) and social impact (86%), signaling that the public sees a clear need for increased transparency in corporate America.

What could have been a highly disruptive strike was avoided on Tuesday when UPS and the Teamsters – which represents more than half of the company’s workforce – reached an agreement on wages and benefits just days before their current contract expired. The deal reportedly includes wage increases that move thousands of full- and part-time workers to at least $21/hour immediately, and $23/hour overtime, and thus closer to making a “Fair, Living Wage”, which as you know is the public’s #1 JUST issue.

Of note is that UPS dropped out of the JUST 100 for the first time in four years last year due in part to its lower scores on our enhanced living wage metrics. The company currently sits at 229 in our overall rankings and 6th out of 24 within its industry, but on Worker issues overall (which make up 44% of our model) they rank 786 overall and 22nd in their industry.

The UPS story is merely the latest in a seemingly endless number of labor disputes hitting the country right now, affecting everything from fast food and media to Amazon delivery drivers, Hollywood writers, and FedEx pilots. As Axios notes, the auto unions are heading into talks for a new contract that some expect will end in a strike of about 150,000 more workers. And with AI’s impact on the workforce looming, who knows how contentious things could get.

In a more positive vein, our recent conversation with MIT professor and President of The Good Jobs Institute Zeynep Ton offers some hope. She explains how companies who invested in better worker wages and benefits saw more bottom-line growth than their competitors and produced better results for both their customers and shareholders. The American worker, it seems, holds the key to value creation for all stakeholders.

Be well,

Martin

At the UN Climate & SDGs Conference, held earlier this month in New York, JUST Capital CEO Martin Whittaker took part in a panel discussion on accelerating the transition to a carbon neutral economy. Highlighting the strong support from both the business community and the public for climate action, Martin emphasized the business case for embedding sustainability practices in company operations. Watch his segment here.

Yesterday, July 27th, marked Black Women’s Equal Pay Day for 2023, representing the additional number of days Black women on average needed to work this year to earn what their white male counterparts made in 2022 alone. Our 2023 analysis shows that only 32% of companies disclose conducting pay equity analyses by gender, and only 24% by race/ethnicity.

This week, The Wall Street Journal and Motley Fool dig into whether ongoing C-suite pay cuts constitute merely a token gesture of solidarity with employees facing layoffs and other economic hardships – or something more meaningful. Citing our COVID-19 Corporate Response Tracker – which found that 20% of companies announced pay cuts for leadership in 2020 – both pieces note that CEO pay cuts remain relatively rare.

JUST Capital publishes our latest review of quarterly stakeholder performance. While all five stakeholders we track delivered negative performance in Q2 2023, we found that over the longer term – from January 2018 to June 2023 – top performing companies outperformed their lowest-ranked peers by 52.13% as measured by JUST Overall Score.

“One of the most exciting trends in the current movement towards stakeholder capitalism is the growing realization that treating employees with respect and dignity is absolutely central to business success. The UPS labor settlement points out that a big part of treating employees with respect and dignity is to pay them a fair wage. Businesses can no longer hide in the shadows of ‘it’s a competitive economy.’ One of the principles of stakeholder capitalism is to use the creative imagination to figure out how to pay people well and remain competitive.”

Digging into a recent McKinsey report, The Washington Post warns that nearly one-third of hours worked in the U.S. will be automated by 2030, most impacting jobs typically held by women, Black and Hispanic workers, workers without college degrees, and the youngest and oldest workers.

Seven leading AI companies – including Microsoft, OpenAI, Google, and Amazon – have made White House pledges to keep their products safe and transparent. Axios outlines these commitments, which include investing in cybersecurity and allowing scrutiny of their AI products by “domain experts.”

Bloomberg reports that Wall Street firms face new SEC restrictions surrounding their use of AI technologies, part of regulators’ broader efforts to increase oversight of artificial intelligence.

The Wall Street Journal covers the hidden, often traumatizing labor of low-paid ChatGPT workers based in Kenya, responsible for sifting through graphic, disturbing text found or generated by the AI, in an effort to prevent the technology from exposing users to toxic and offensive content.

Stanford’s Existential Risks Initiative identified artificial intelligence as an extinction-level threat to humans as part of a recent study. CBS News unpacks the findings.

New findings from an EY report show that while the 2023 proxy season saw an uptick in ESG-related shareholder proposals, support for them plummeted. Fortune’s Modern Board newsletter digs into what could be behind the trend.

A Harvard Business Review piece outlines how companies can legally use racial data in their DEI efforts following the Supreme Court’s Affirmative Action ruling.

Seven major automakers commit to investing at least $1 billion dollars to build 30,000 electric vehicle fast chargers in the U.S. and Canada. The New York Times has the story.

In the 33 years since the Americans with Disabilities Act was signed into law, many workers remain hesitant to disclose a disability. CNBC’s Sharon Epperson reports on new polling from Disability: IN, finding that while 93% of surveyed employers encourage their workers to confidentially self-identify, just 4.6% actually do.

As extreme heat continues across the globe, the Financial Times looks at the impacts these rising temperatures will have on a slew of industries. CNN also dives into the alarming rise in heat-related deaths on the job and the government’s work to develop a heat standard for workplaces.

Fortune’s CFO Daily newsletter covers a new report from Strategy& that outlines areas that are most and least effective to cut costs for long-term growth. Among those to avoid? Training and development and employee benefits.

As You Sow announces the launch of InvestingESG.org – a new educational resource that aggregates commentary, policies, and research on the use of ESG risk-assessment frameworks for business and investing.

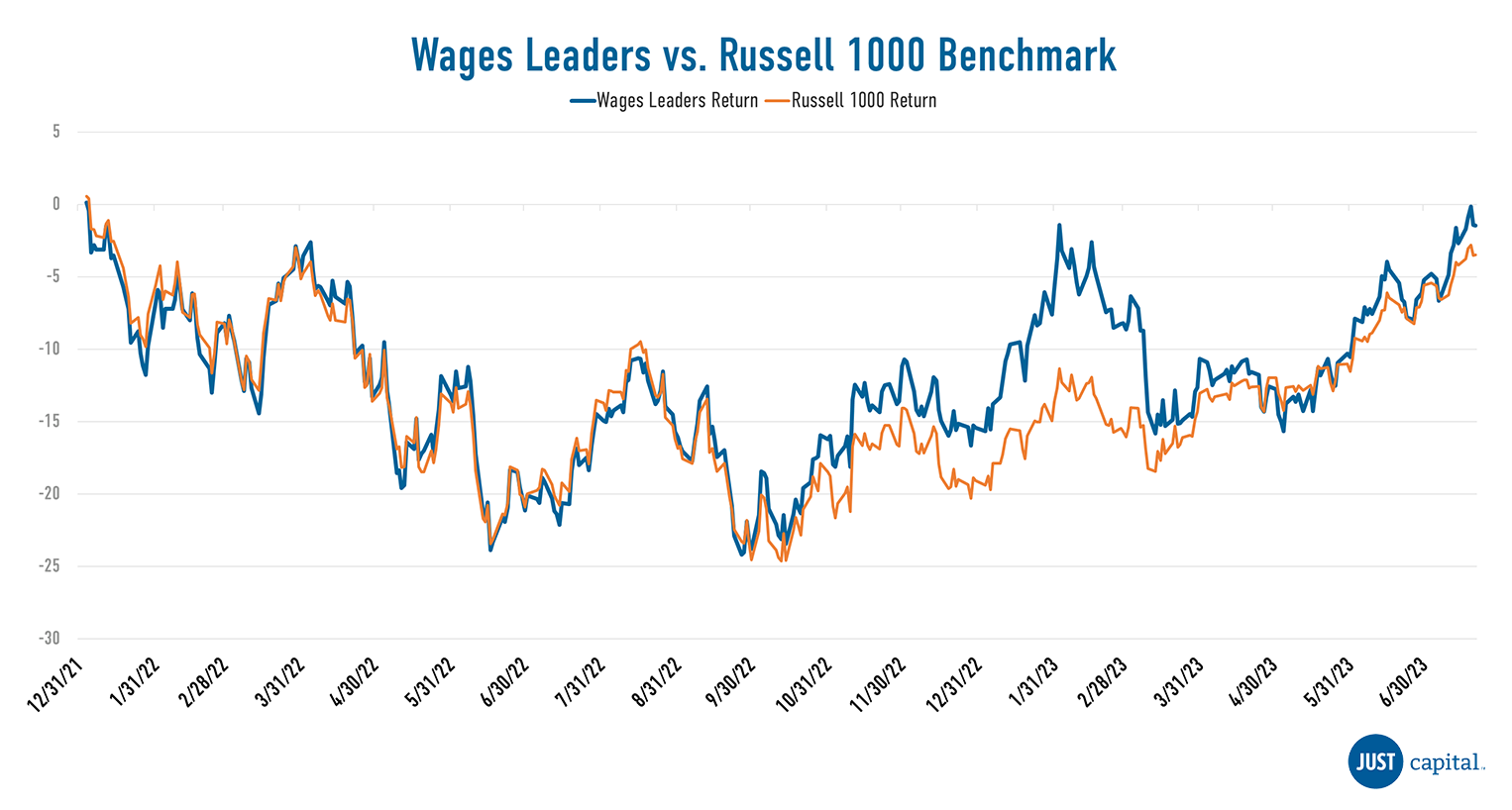

CHART OF THE WEEK:

The Wages Leaders index concept features the top 20% of Russell 1000 companies in JUST’s annual Rankings that pay a fair, living wage. This index concept highlights the financial performance and impact of investing in companies that prioritize fair and equal pay that covers the basic financial needs of their workers. From inception on December 31, 2021 through July 21, 2023, the concept has outperformed its Russell 1000 benchmark by 2.01 percentage points.

As more people in the workforce enter the “sandwich generation,” caring for their own children and older parents or relatives, access to equitable leave policies is becoming more and more desirable for employees. Despite this, only 9% of the largest U.S. companies currently offer parity of 12 weeks or more of paid parental leave to both caregivers, according to a recent JUST Capital report. In fact, research suggests that the percentage of companies offering paid parental leave has actually decreased in recent years.

One company that has prioritized its leave benefits is Morgan Stanley, which doubled down on parental leave in 2021. After analyzing results of a global employee survey and benchmarking peers, Morgan Stanley increased its parental leave to 16 weeks for all caregivers and four weeks of paid leave to care for a family member with a serious health condition, among other generous policies, such as a $75,000 maximum family building benefit to assist employees with the cost of adoption, surrogacy and fertility treatments. Previously the company offered primary caregivers 16 weeks of parental leave and non-primary caregivers six weeks of parental leave. This step forward to parity is critical to cultivating both gender and racial equity in the workplace.

JUST Capital recently spoke with Dr. David Stark, Morgan Stanley’s Chief Medical Officer and Global Head of Benefits, Analytics, and Technology Strategy, to learn more about how and why Morgan Stanley implemented its enhanced paid parental leave policy, as well as the impact on its workforce and company as a whole.

You increased your paid parental leave to 16 weeks for all caregivers – what prompted you to make this level of investment?

We made this change back in 2021. So, recall that the pandemic led to the caregiving crisis. We were seeing people leaving the workforce to take care of their kids or their parents or others in the home. This is on top of, you know, the “sandwich generation” being an issue, and I’m a part of that myself. We know that women were disproportionately being taken out of the workforce to shoulder those [caregiving] burdens. We were recognizing all of that. Additionally, in 2021, we did a global employee benefits survey, which was a really detailed and eye-opening survey. Overall, the vast majority of our employees were very happy with their benefits, but paid parental leave and family support were areas that were highlighted as opportunities for improvement. In fact, paid parental leave was the top driver that could promote increased satisfaction relative to other potential design changes we were considering.

The pandemic, the external environment, and our own surveying led us to benchmark our family support benefits against our peers, and then decide to prioritize the [family support] space for focus. What we learned is that our paid parental leave benefit had fallen behind our peers.

What did the progression of planning and rolling out of this benefit look like?

Using all of the [survey and benchmark insights], we developed a multi-year roadmap to enhance our family benefits – not just parental leave, but other support benefits. We addressed paid parental leave first. We thought that was where we could have the most significant impact.

We also looked for some quick wins that we could achieve relatively easily. For example, we put in place NICU and stillbirth leaves, and we eliminated a one year of service term requirement. We did that immediately while we took a little bit more time to redesign and socialize the more extensive expansion of parental leave enhancement. We also enhanced our family building benefit. We already had a pretty generous fertility benefit ($30,000 lifetime benefit) to support fertility regardless of infertility diagnosis, but we wanted to make that benefit more holistic. We expanded the benefit to provide a $75,000 lifetime maximum to support family-building across adoption, surrogacy, and fertility.

We expanded our paid parental leave to provide 16 weeks across the board for all parents, regardless of primary/non-primary [parent] and gender. In the U.S., we provide an additional six to eight weeks of disability leave for birth parents, resulting in a total of 22 to 24 weeks of parental leave.

How did you build the case for that level of support? What hurdles did you need to overcome?

Management was generally supportive of the change. It was obviously important to socialize the change within each of our business units, since the extended duration would have distinct and nuanced impacts on their respective organizations, resulting in the need to backfill roles and potentially impacting performance measures. This was actually happening amid a broader backdrop of the “great reshuffling” or the “great resignation.” James Gorman, our CEO, made a call to his operating committee at an off-site meeting that he felt strongly that we needed to renew the social contract with our workforce. That [prioritization] led to a very holistic look across the benefits space.

The general environment was very supportive of making these changes. It was viewed as an investment in maternal and infant health, long-term retention, and productivity upon returning to work. Those [investments] were weighed very favorably against the obvious, but relatively small, short-term issue of needing to backfill [roles held by employees on leave].

How do you respond to executives who say, paid parental leave is nice, but we can’t expand benefits in this economy?

Enhancing parental leave has low direct costs. It has a significant impact in terms of improving productivity, retention, and employee morale. Anecdotally, the feedback that we get from employees who’ve had the time to bond with their child, recover from giving birth, and support their partner in recovering from giving birth, is that [access to paid time] buys loyalty. And that’s almost immeasurable relative to the cost. It’s part of long-term thinking.

Oftentimes, frontline workers are not offered the same benefits as their corporate peers. How are you supporting not only corporate employees, but hourly employees or contract employees when it comes to parental leave?

Employees who work 20 hours or more, whether they’re hourly workers or salaried, are eligible for a full suite of benefits, and that includes paid parental leave.

As a global business, how do you approach benefits across different countries and territories?

That’s the fun part. Increasingly, through the pandemic and beyond, we have felt the need to provide more consistency globally across the board. We’ve actually worked very hard to first understand: What are the policies in the 40 countries where we operate? What’s the regulatory environment across all of our markets? What are local practices? And then we worked to establish, in this case, a global minimum standard to ensure consistency. That led to the 16 weeks [of paid parental leave] as a floor for all employees, and in certain markets, where regulations or local practices allow for more leave, we do that.

As a more general matter, delivering healthcare and other benefits globally is fascinating and challenging. The United States is probably the only country where employers are the principal providers or purchasers of healthcare on behalf of their employees. In most other countries, employees top up their national healthcare benefits with employer-sponsored plans. There’s obviously a lot of unevenness to navigate. We don’t strive to be equal across the board, we strive to be equitable across the board.

What benefits have you seen in your workforce in terms of recruitment, retention, wellbeing, productivity?

We are a year in, so, perhaps a little bit early for a formal evaluation, but we are quite rigorous about how we collect data to evaluate our programs and our offerings. On utilization, what we’re seeing is all parents are taking more time off for leave. One obvious question that could come up whenever an employer changes a policy or expands a leave is: are our employees actually taking advantage of it? I’m proud that our employees are. Birth parents are taking off, on average, five more weeks (+30%, from 16 to 21 weeks); non-birth parents are taking off four more weeks (+70%, from 6 weeks to 10 weeks). Additionally, non-birth parents are now deciding to take leave, whereas in the past so-called non primary parents (traditionally, the dads) might not be taking leave. Now, adjusting for headcount changes, we’re seeing about 15% more non-birth parents opting to take leave, which is great. Another component of the leave that we introduced was flexible leave, so you can take leave in up to three chunks over the year and can even start your leave before childbirth as well. My husband and I had our third kid in January, so I took off five weeks initially and I’ll take off two other chunks. That is what worked best for my family and my work. Of the non-birth parents who are taking parental leave, about 20% of them are opting to take advantage of our “flexible” leave policy, which allows parents to split their leave in up to three separate intervals.

What advice would you give an executive who wants to lead on this issue in their own company? What should they do first? What’s something to avoid doing?

We have quite a rigorous approach, and I’m very proud of how we developed our strategy around benefits design. I mentioned the dedicated benefits survey that we did back in 2021 – that was a global survey and which 35% of our entire workforce participated in – and it was quite extensive. In addition to that, we have our annual engagement survey where we ask about whether employees feel they have the resources they need to support their health and well-being. We also hold managers accountable. In their upward feedback of their managers, employees are asked whether their manager supports their health and well-being.

We also have a Global Wellbeing Board that we developed in the last two years, comprised of 16 senior leaders across the firm, like CEOs of business divisions. The responsibility of this board is senior accountability and ownership over our health and well-being strategy. I felt that this was important, because although HR/HR benefits traditionally has the role of developing and rolling out new programs and resources, health and well-being is a business imperative. It therefore requires involvement and buy-in from across the business. That’s been an excellent additional source, not just of leadership and visibility, but actually providing input into our strategy.

Complementing that top-down structure, we have a bottom up-structure: our Global Wellbeing Influencer Network that we also launched in the last year. This is essentially a grassroots network of employees, who have already demonstrated commitment and interest in supporting well-being issues. We’re giving them resources: awareness, programming resources, access to our programs, and a community to network through, so that they can be evangelists for our benefits and provide feedback both to HR and to the Global Wellbeing Board on our benefits. We have a lot of distinct modalities for collective sentiment around benefits.

We also look at hard data utilization, claims data, external benchmarking data, and market research. That all funnels into developing our multi-year strategy. This is a long-winded way of saying that we’re quite rigorous about using data to support the business case that we develop for any change in our benefits. And then ultimately, our job is to manage population health for our 83,000 employees in 40 countries. As a Chief Medical Officer, in addition to being a Global Head of Benefits, when I speak to management about the work that we’re doing, I’m speaking with this lens as a population health leader, not just as a benefits professional. I think that helps advance our case as well.

Given your role, how do you make the connection between increased paid leave and health?

I’m a physician, a pediatric neurologist by training. I have a background in biomedical data science, and biomedical informatics, so I’m serious when I say we were quite rigorous across all of our programs. There’s essentially four types of metrics that I care about: they are utilization, costs or affordability (both for employees and for the firm), employee experience, and then ultimately, health-specific outcomes.

Over time, we can actually do observational studies, where we look at different employee groups, those who have utilized a particular benefit, and those who have not. Then we look at outcomes of interest over time, whether that’s retention, productivity measures, or other performance measures that we have. Sometimes we rely on external measures for this as well. We know supporting mental health is the right thing to do, and so I’ve strongly made the case that we’re not always going to be able to demonstrate with hard metrics and ROI behind what we do. There are certain times where we have to say, “look, we already know this is the right thing to do. The evidence is out there. It’s been proven externally. Let’s not spend time arguing over whether it’s the right thing to do. Let’s agree and deploy internally, and then follow up over time.”

JUST Capital, in collaboration with partners, established the Corporate Care Network to advance the well-being of workers and demonstrate the long-term value of investment in workers. The Network is committed to driving increased access to care benefits, including paid leave and flexible work policies, and highlighting leaders in the space.

If you’re interested in gaining insights into how to improve on the issues that matter most to the American public, and learning how your company can get involved in the Network, please reach out to JUST Capital impact@justcapital.com.

For decades, many in the business community viewed a “lean and mean” operational strategy as the winning playbook: minimize costs in order to maximize profits – especially when it comes to labor costs. But a growing body of research indicates that when it comes to employees, mindsets need to shift and labor costs should instead be considered investments with the power to deliver strong returns.

On the cutting edge of that research is Zeynep Ton, MIT Professor and president of the nonprofit Good Jobs Institute. In her recently published book, “The Case for Good Jobs,” Ton lays out the key findings of years of research spent analyzing companies like Sam’s Club, Quest Diagnostics, and several factories, restaurants, retail stores, and call-fulfillment centers. Her main finding is that investing more in one’s workforce is more cost-effective than investing the bare minimum or “lean” amount, and that customers and shareholders benefit significantly when workers are supported.

In a recent conversation with JUST Capital – as part of the Worker Financial Wellness Initiative, supports company leaders as they prioritize workers’ financial security – Ton dove deeper into her findings and the changing notion of what it means to be a top performing company.

As she puts it: “Investing in workers isn’t about being nice. You’re doing this because this is how you win with customers. This is how you win as a business.”

At first glance, minimizing labor costs in any way possible makes sense. If labor is just another cost to be minimized, then of course, paying market rate, as opposed to a living wage, is a good call. But the reality is, human capital is a bit more complicated than that, Ton explained.

(A living wage is the amount of money needed for a given worker to cover the cost of their family’s minimum or basic needs in the area in which they reside).

“Paying workers low wages is actually very expensive for companies. Think about the costs of high turnover, the costs associated with low wages like lost sales, lost productivity, mistakes, errors, customer frustration,” Ton said.

In essence, when workers feel they’re replaceable, they act replaceable, she explained. And in addition to the high costs of replacing workers, companies have to foot the even greater costs associated with poor operational execution and a styming of innovation.

“If you have poor attendance, minimal effort and poor execution, and a cycle of high turnover, then middle managers are firefighters,” Ton said. They’re not managing their business or thinking of ways to make things more innovative or efficient, she explained, they’re fighting fires all the time.

At companies with low worker investments (low investments in wages, benefits, training, and career development), Ton explained that she’s observed turnover levels ranging between 40-400%, with 400% meaning a typical person stays for three months maximum. That translates into millions of dollars lost. “The direct cost of turnover ranges from 10-20% of payroll dollars that the company spends. And that’s just the costs associated with recruitment, hiring, onboarding, etc.,” she said.

“Competent leaders who want to run great companies, deep down, they know that you can’t run a great company if you don’t have a great team. You have to position your team for success,” Ton said. “So what I do in my book is articulate a case study on why they should do it and how they can do it.”

The good news is, there is a better strategy – what she calls the “Good Jobs Strategy” – where workers, customers, and shareholders reap more rewards. According to Ton, one key part is investing in workers while at the same time creating a culture of high expectations.

She cited Costco as an example. In 2022, the company’s U.S. average hourly pay was around $26 per hour, compared to the average retail worker wage of $16 per hour. That $10 extra is significantly higher, but has resulted in a more loyal and hardworking workforce, her research shows. Costco’s turnover is a “fraction” of the industry’s, Ton said.

Investing in workers doesn’t just mean paying a living wage or expanding benefits, it’s also about how companies operate, she said.

Costco sets up their workers for success even further by focusing and simplifying their inventory and investing in more training and cross-training, which allows workers to help customers as needed, Ton said. By having far fewer products than typical grocery stores, Costco’s workers are more knowledgeable about them (where they’re located, how they taste, typical shipping times), and that makes a better experience for the customer, Ton explained.

“At the same time, Costco has high expectations of its workers – the mindset is to create high value for the customer,” she said.

It’s a strategy that’s been working. Costco has continued to outperform its competitors and deliver good returns for investors.

“If you are customer-centric – which many businesses are – you have to be frontline-centric, because if the frontline employees don’t serve the customers well, if they’re not improving the business all the time, then you’re not creating value for the customers,” she said.

Indeed, multiple recent studies support Ton’s findings, showing that worker wellbeing – a byproduct of investments in their training, benefits, and wages – is associated with higher firm profitability, and that companies with the highest levels of worker satisfaction outperform standard benchmarks in the stock market.

Healthy investments in workers is also what Americans – from all backgrounds – want from CEOs. JUST Capital’s 2022 polling of the nation’s public shows that Americans agree that the top priority for companies should be to pay their workers a fair, living wage. The public also said that worker health and safety, career development, benefits, and diversity & inclusion should be among a company’s top priorities.

“By better serving consumers, through employee investments, you better serve shareholders,” Ton said.

The Worker Financial Wellness Initiative is a vibrant and growing community of business leaders dedicated to improving the financial health and security of their workers. The Initiative includes peer learning opportunities for C-Suite leaders; resources and events for HR and compensation professionals; direct assistance to companies on how to develop and deploy a Worker Financial Wellness Assessment, and how to use it to identify areas for improvement and immediate next steps; and public opportunities to celebrate corporate leadership.

To learn more about the Initiative and how you can join, click here.