Hi – it’s Alison Omens, President of JUST Capital, filling in for Martin with a dispatch this week from Washington D.C., where JUST Capital’s media partner, CNBC, hosted their second annual CEO Council Summit. Given our location and the upcoming election, much of the conversation centered on how CEOs can navigate the political environment to lead in transitional and turbulent times.

The Managing Director of the IMF, Kristalina Georgieva, kicked off the morning with a challenge to leaders that I appreciated. She noted that this decade is still being defined and that the Twenties may come to be known by one of three ‘T’ words: turbulent, tepid, or transformational. She urged business leaders to steer toward the latter path.

But other leaders had a different message.

In their own ways, Speaker Mike Johnson, FTC Chair Lina Khan, and Assistant Attorney General Jonathan Kanter, who leads the Justice Department’s Antitrust Division, all signaled the importance of business staying in its lane without running into enforcement challenges or overstepping on social or political matters.

This message left an interesting challenge in my mind, something that JUST Capital spends our time on – understanding what business leadership means today.

There were two additional ‘T’ words that Georgieva didn’t use, but I think are highly relevant here. One is transition. This moment is transitional for businesses, whether transitioning to an AI future, changing demographics, climate, or shifting political winds. To navigate these transitions, I recommend looking at JUST Capital’s extensive polling of the American people for guidance. The public is clear, regardless of ideology: focus on your own workforce. Create jobs with good wages and benefits in communities that need them.

The second ‘T’ word, also derived from the polling, is transparency. Transparency signals priority and direction, and Americans clearly believe it to be a necessary part of effective business leadership today (check out this Agenda Week article about the importance of transparency on workforce and human capital issues with JUST Capital’s data).

Each business leader needs to forge their own path on how to guide their organization through challenging times. Through the turbulence, focusing on workers and transparency will be key.

“If all the women are secretaries, and all the men are executives and you don’t tell us that, you have not given us the information that we need to assess whether or not you’re really an employer that values all types of people.”

Two weeks ago, we released the CRE Alliance Standards, which is a roadmap for businesses to advance equity and inclusion, combat discrimination, and embody the best of socially responsible business.

But, to bring these standards to life, we must work together.

Contribute to the development of the standards by taking part in our public comment period. If you want to lend your perspective on the topics of corporate governance and leadership, internal infrastructure, workplace culture, workforce diversity, job quality, products and services and/or a socially responsible value chain, take our online survey or sign up for a virtual roundtable discussion before September 13.

Read the standards and take the survey inside.

Business Insider highlights a McKinsey study that says AI has the power to disrupt the job market by 2030 as severely as COVID did in 2020.

The Washington Post reports that a dozen of current and former employees at OpenAI and other prominent AI companies warned that the technology poses grave risks to humanity in a Tuesday letter, calling on these businesses to implement sweeping transparency changes. Learn more here.

Bloomberg is reporting that key engines of US spending are declining all at once, alongside increases in credit usage as disposable income declines.

Meanwhile, Walgreens joins Target and several other retailers in slashing prices on over 1300 common items within its stores to help out their customers. CBS News has the story.

In possibly the strangest business story of the week, the CEO of Chipotle had to answer questions about “shrinkflation” in Fortune this week after several Tik-Tok videos went viral claiming that the chain was skimping on meat in their orders.

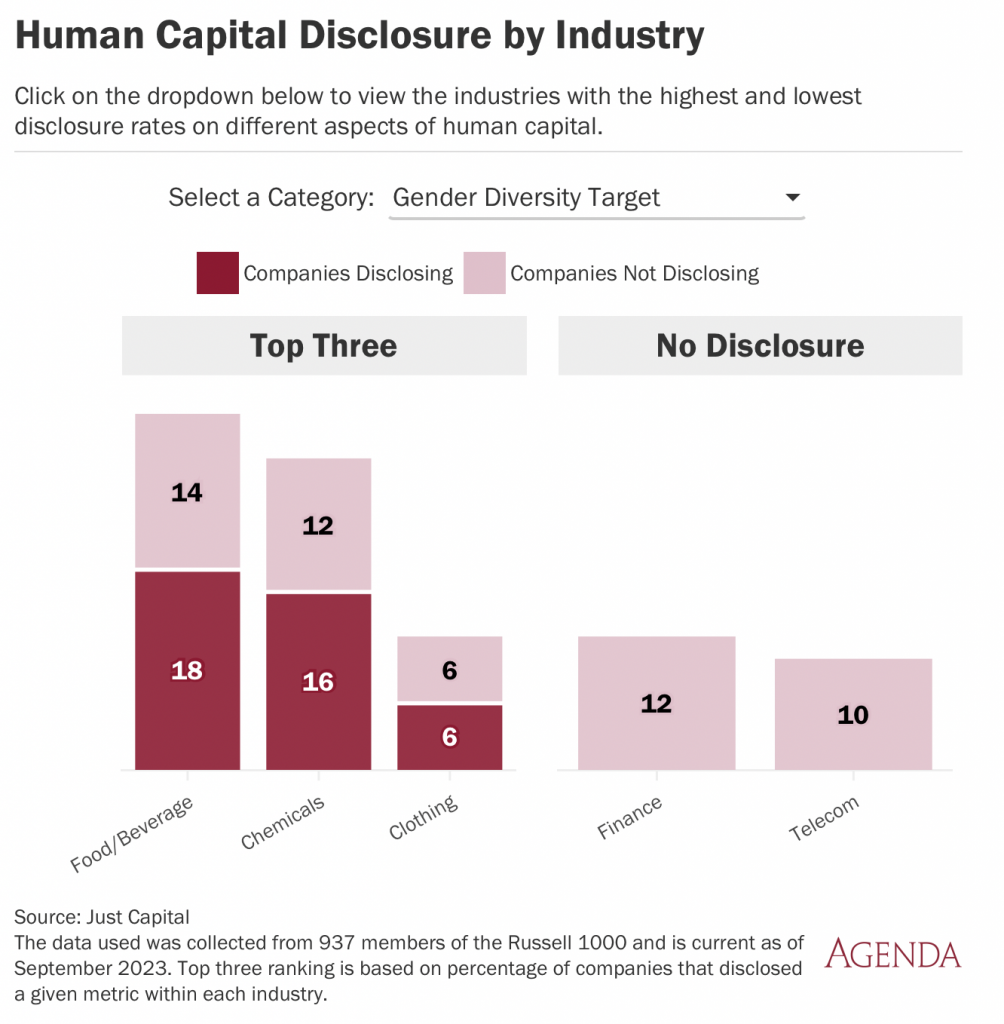

This chart comes from a deep dive into the data within our JUST Jobs Scorecard via Gretchen Lenth at Agenda Week, highlighting which data points different companies are disclosing across industries. Explore this interactive chart and others in the full article.

Walmart made headlines this week with news that the company plans to raise starting wages for its frontline workers to at least $14 per hour. When the wage hike goes into effect in early March, Walmart store employees will earn $14-19 an hour – up from the $12-18 they currently make hourly.

The announcement comes after Walmart made its second appearance on the JUST 100 this year, thanks in part to strong performance on issues including local job creation, hiring programs to assist with re-entry to work for formerly incarcerated individuals, employee retention and advancement, and detailed disclosure of workforce demographics.

Walmart has invested in becoming a leader on good jobs. When it comes to wages, however, the company has been weaker. We’re delighted to hear it’s raised the baseline, and also know that most wages for Walmart workers, according to JUST data, are already higher. After raising its minimum wage to $14 per hour, Walmart is around the average in its industry. But it is below the median in its industry ($15) and below retail competitors like Best Buy, Target, and Amazon (all $15).

As the largest private employer in the United States, what Walmart does matters.

Companies compete with the retailer for consumers, workers, and innovation. Walmart is also an extremely profitable company. Walmart can set a precedent for corporate America when it comes to many practices, including pay. And it’s chosen to raise wages at a time when the labor market for retail remains tight, its workforce continues to deal with inflation and rising costs of essentials, and fears of a recession loom.

Moving to a $14 minimum wage is important, but it’s also important to note that this rate is still much lower than the national living wage average of $17.46 for one full-time worker with no children, as well as a family-sustaining living wage of $24.16 for a family of two full-time workers and two children according to MIT’s Living Wage Calculator.

Paying a fair, living wage has consistently remained the number one priority of the public for the last three years. The reality is, and as our research shows, 51% of the workers in the Russell 1000 are still not earning a family sustaining wage. This is true while a majority of Americans we polled (84%) agree that large companies have a responsibility to pay their frontline workers enough to make ends meet and regularly increase wages to keep up with the rapidly rising cost of living (87%). And that companies that do so will be better for the U.S. economy overall (86%) and more competitive in its industry (71%).

Disclosure of minimum wages paid by major U.S. employers also remains sparse. JUST analysis found that only 13% of America’s largest companies disclose some data about their employees’ hourly wages, and even fewer, 9%, disclose the exact value of the minimum wage paid to their U.S. workforce. This persists despite a majority of Americans we polled (89%) supporting companies releasing the minimum wage paid to frontline workers.

And while moving to a $14 minimum wage is a welcome step, it is also important to note that with inflation, that doesn’t change that much from people’s current reality. Ultimately people can’t be present and engaged at work if they’re worried about putting food on the table and affording transportation to work and to bring their kids to school. My colleague Matthew Nestler put together some helpful charts explaining why it’s important for employers to continue to raise wages to match inflation and also helped debunk some of the persistent media narratives that pit wage gains for frontline workers against fears of a wage-price-spiral.

Our co-founder and chairman Paul Tudor Jones recently discussed this theme with CNBC Squawk Box anchor Joe Kernen:

We’ll keep tracking Walmart’s leadership on the issue, and the connection to its operations and competitive advantage. And we’ll do the same on other companies who follow its lead, and continue to forge ahead on their own. We will continue to track and push for a sea change on how companies invest in their workers, including through wage transparency and wage increases.

A recent headline I appreciated (and chuckled at a bit) notes companies are “hoarding” workers. The economic term is apt for how companies traditionally have approached their workforce: a cost to be managed. And so in the early days of the pandemic, with so much uncertainty, the answer was to lay off mass numbers of people to conserve capital. Yet, two and a half years later, we’re still paying for that decision in non-resilient supply chains, ill-trained workers, and ongoing turnover costs.

I’m often asked if I think the pandemic changed how companies fundamentally see their workers, and, with a potential recession oncoming, if we’re sliding toward business as (pre-pandemic) usual. The hoarding phenomenon is one example that I believe implies some fundamental conventional wisdom may be changing in favor of an emerging business strategy that: 1. Acknowledges that human capital can be a source of value creation, and that replacing that capital costs a lot in terms of productivity, recruitment costs, and institutional knowledge, and 2. Reflects a growing awareness that workers are more than capital, that investing in people can lead to strong, positive culture changes, and that underinvesting in human capital (or ignoring it altogether) can leave companies vulnerable to consumer and worker pressure.

Of course, this approach isn’t new, and didn’t emerge with the pandemic. Yet, for those of us who are focused on the momentum of the last couple of years around jobs and worker value, there’s an urgency to ensuring that trend continues, and we don’t return to pre-pandemic normal. The American people believe, and share that urgency. JUST Capital continues to see polling on how intensely they want to see companies invest in their workers.

It’s part of the reason we recently launched our JUST Jobs program. JUST Jobs is meant to highlight how companies are acting on the lessons from the past two and half years on the importance of workers – and which ones haven’t lived up to the rhetoric. Concerns about a potential recession and inflation make these questions more urgent. I spoke last week at CNBC’s Workforce Executive Council, where conversation focused on how to manage worker issues in a turbulent time. Knowing that this question is at the top of many people’s minds, and that simultaneously there’s significant work underway to secure the progress that’s been made, I wanted to observe and connect the dots around what’s currently happening.

JUST Capital is in a lot of rooms with different economic players, from corporate leaders to investors to civil society leaders. I’ve come to think about the work underway, and what needs to happen, in three buckets: the definition of a good or “just” job, the measurement of a good job, and the investment in creating good jobs.

Each bucket has seen different levels of progress recently. We spoke with some of the largest U.S. companies to gauge their reactions and thoughts on the work underway and what’s still to come, and have collected an overview of what we’ve found.

The Aspen Institute and Families and Workers Fund spearheaded a process over the last six months to define what a good job is, recently launched as the Good Jobs Champions Group’s Statement on Good Jobs and Working Definition. We were excited to facilitate corporate conversations that informed the multi-stakeholder-based definition, led by Kelley Frances Fenelon, our Director of Programs and Engagement. There is other work underway, from additional survey work of Americans to listening directly from workers on what constitutes a good job. I believe that in the next six months or so, we’ll have far additional clarity and shared language around what constitutes a good job.

And in the meantime, it’s useful to pause and lift up the elements of the Good Jobs Champions Group’s Working Definition that found clear resonance within our facilitated corporate conversations and aligned with corporate leaders’ priorities – as well as notice where there are sticking points or differences in approach. Most importantly, company representatives were excited to see a “North Star” understanding of job quality that could inspire action across different companies in different industries. Shared language, they agreed, is inherently helpful, even as businesses will tailor any good job definition’s component parts to align with their unique employee value proposition.

But moving beyond the usefulness of a definition in general, what did they like about this one? By focusing on three thematic areas – economic security, economic mobility, and equity, respect, and voice – the working definition acknowledges that no single aspect can address the whole of job quality. Instead, high-profile (and certainly important) aspects of job quality like compensation are rightly portrayed as one part of a larger puzzle. That point came up time and again, as company representatives across industries expressed appreciation for the definition’s inclusive approach.

A few elements of the definition also stood out as forward-looking to companies as they race to define how they’ll attract, develop, and retain the right employees. While the table stakes issues that provide for workers’ economic security can’t be ignored, the corporate representatives emphasized that it’s increasingly important for companies to demonstrate that individual employees are valued and integral to the success of the organization. That can look like being meaningfully included in operational decisions that impact their role, supported with leave and benefits policies, and invested in as an individual who has room to grow within the organization.

Another emerging focus for companies is attention to wealth-building opportunities so that, as one representative put it, people can go beyond surviving to thriving. Company leaders pointed to wealth-building opportunities as a leading advantage for employers of choice with initiatives like financial literacy education, retirement savings, employee stock ownership programs, and education and training for career advancement.

And yet, company representatives noted that any good jobs definition will, by nature, paint with a broad brush, thereby making it difficult at times to see how some elements apply across the workforce. Should all positions offer employee stock ownership? How do fair scheduling practices apply to a salaried managerial or even executive leadership role? In a sense, these questions ask: For whose jobs are these definitions meant? A counterpoint was raised by several company representatives as well – the definition usefully signals the importance of job quality features that are not yet commonplace across the U.S. workforce, and demands thoughtfulness about what employees at all levels of a company should expect from their job.

In doing so, the Good Jobs Champions Group’s Working Definition allows companies to prioritize the future of work at their organization in the midst of a highly competitive talent environment by creating jobs that, as one participant hoped, really make people want to stick around.

Ultimately, however, a job quality definition is only as good as it is useful, and those we spoke with saw how this one could be carried forward and put into action. From being used as an internal tool to advance conversations about workforce initiatives, to providing a point of reference in comparison with an existing employee value proposition, to even serving as an accountability mechanism to check internal priorities, most company representatives could immediately envision how they’d use the definition. They were also eager to see what might be built beyond the definition to capture context (e.g., how key elements like good managers and robust, diverse employee pipelines come into play) and inform improving practice (e.g. benchmarking tools and leading practice examples).

Those hopes for what’s to come align with my own sense for what’s needed. Once we have a definition, how do we capture whether companies are living up to its promise?

There are two things needed to measure a good job: Agreement on specifically what to measure, so that everyone can benchmark and track according to the same metrics and the data itself.

I was on a panel last week that Jobcase hosted, with the Rise Fund and the Burning Glass Institute. The three of us functionally represented three kinds of data: Publicly disclosed, private, and crowdsourced. This means what we’re measuring could focus on disclosure of certain policies and practices or outcomes of those activities. This is one of the elements that we and others will continue to work through – how do we best construct metrics that recognize the unique, and complementary, value of different datasets.

The U.S. Department of Labor has also been facilitating a similar dialogue (we’ve been honored to co-lead the workstream on corporate data) on how to integrate different sets of data from different sources to create a holistic view of jobs. So there is some progress on aligning these approaches to measuring good jobs, or at least getting much clearer on what the differences are and how to use each appropriately.

On access to data, we are seeing momentum in a couple of areas, including last week’s release of the American Opportunity Index. What’s important about this index is that it’s one of the first times that crowdsourced data is standing on its own to assess companies relative to each other. It speaks to how much data has now been aggregated from job sites and other places so that research organizations can begin to use employees’ own, self-reported data to track real workers and their progress.

On the public disclosure side, rates are still quite low. JUST Capital did a recent assessment on the workforce data that we use in our Rankings, and it shows that much data disclosure is below 50%, and for data that investors and researchers really want (turnover rates, total workforce compensation, training costs) that number is much lower. According to an assessment JUST Capital did a year ago, most were less than 10% or even 5%.

As for jobs strategy at private companies, we’ve been part of several conversations recently in which we discussed with investors, like those in private equity, ways they can determine which businesses are implementing a good jobs strategy – and invest accordingly. So stay tuned for more on that, too.

Finally, and most crucially, none of this matters if we don’t see movement on the creation of good jobs.

Our main message to companies on creating good jobs is to start with some fundamental questions. These questions are applicable regardless of industry, type of workforce, and more. I spoke at Slack’s Future Forum event this week and I suggested executives ask four main questions about their workforce, with a particular focus on frontline workers:

Once you have the answers, start to align how to address those questions with your business strategy. These questions are how JUST Capital orients our programmatic work, as well. It’s why JUST Capital and PayPal, in partnership with the Financial Health Network and the Good Jobs Institute, launched the Worker Financial Wellness Initiative to support companies as they decide which questions to ask first and how they’ll go about answering them. JUST Capital will also be launching a cohort on racial equity in the coming months.

One company may make different choices about how to address the results of the questions, and at the end of the day, a workforce strategy, along with a stakeholder capitalism and purpose strategy, must align with operational strategy. Otherwise, it often simply becomes noise, and the first thing to cut.

We’re seeing significant movement both from investors and workers on the topic of good jobs. Both State Street and BlackRock are putting an increasing focus on how companies should think about their human capital strategy. The Human Capital Management Coalition, a group of institutional investors representing over $8 trillion in assets that is co-chaired by our Head of Investor Strategies, Cambria Allen-Ratzlaff, continues to push companies for fundamental workforce disclosure data. And, as ESG has become seen as political, the “S” or Social issues, continue to be built out as an example of a real value driver (something I wrote about at the beginning of this year).

Workers themselves are also starting to apply real pressure. Whether it’s organizing unionization pushes, leveraging social media to highlight workplace conditions, or refusing to remain in a workplace that doesn’t provide quality jobs or access to opportunity, workers are increasingly feeling empowered to speak up when they feel like their employers aren’t living up to their expectations.

Finally, governments have taken more of an active role. In California, the legislature recently passed a law essentially establishing a workforce council for the fast food industry. The SEC has also continued to signal that it will take up human capital disclosure soon. At a recent SEC Investor Advisory Committee, two JUST Capital colleagues presented on the importance of human capital.

JUST Capital believes in the catalytic effect of large companies through their own footprint and that of their suppliers. We work with the largest publicly-traded companies in the United States, which employ around 20 million people. According to our recent assessment, half of those people do not make a family-sustaining living wage. Wages and compensation are obviously one core element of a good job. We launched the JUST Jobs program to focus directly on those 10 million people through this program, and indirectly the lives of the 160 million people who are employed in the United States.

Defining, measuring, and creating JUST Jobs is core to the program. The primary tool we’ll employ in this effort is a JUST Jobs Scorecard, which will track elements of a good job year-over-year using publicly available data, and show how each company stacks up relative to their peers. The Good Jobs Champions framework noted above is influencing what we measure, along with our and others’ polling work. We’ll be using the Scorecard to show companies where they can improve for their workers, and work with other nonprofits that are experts on specific elements of that on further improvement recommendations.

We’ll also continue to share the business benefits for an investment in good jobs. We’ll uplift research that continues to show that investing in workers leads to better productivity, lower absenteeism, more innovation, and lower turnover costs. We’ll partner with academics and others to continue to interrogate and highlight these facts.

We’re focusing on this topic at this moment because there is urgency to ensure that we don’t unlearn the lessons of the last several years. And the American people are very clear, according to a number of recent surveys conducted by JUST Capital, that this is the issue that companies should be focused on.

Much ink has been spilled on the Great Resignation and what it all means. People are leaving their jobs at record levels, and with the degree of job openings and wage growth, there’s far less risk in doing so than there used to be. Both business and finance leaders are taking note. Businesses are reassessing their jobs strategies, and investors asking about those strategies, and expecting far more thoughtful and detailed answers than in years prior. This growth has coincided with a rapidly intensifying interest in the “S” of the ESG, with people across the market working to define and benchmark what it means to invest in the social aspect of a business, from jobs to supplier issues.

Yet there hasn’t been much focus on how to approach this moment from an individual perspective, either as a worker or as a manager. In speaking to a friend recently who’s struggling with her own job, and wondering if she should leave, I shared the emerging consensus around the framework of a good job to help her measure her own satisfaction. As a manager myself who’s had employees leave, I’ve used this grouping to assess what I’m doing well and where I need to improve.

In an environment where we’re all worried about turnover, this framework is useful to start breaking down where an organization may be coming up short. So what are the dimensions? It’s usually four or five elements, including:

If we imagine this framework as a pyramid, financial security is at the bottom. Without financial security, every other dimension of a good job goes away. This is both intuitive and oddly an area of under examination. To put it plainly, imagine someone loves their job but their wages and compensation don’t cover their rent, food, childcare, and transportation. If they find a job that pays $1 more an hour across town, they have no choice but to take it.

And this isn’t a small number of people. According to our past research, half of employees working at the thousand largest publicly-traded companies in the US aren’t making a living wage. And according to a recent survey, more than half of Americans can’t afford a $1,000 emergency. I will say it again and again: Every employer should be assessing their compensation package and their approach to providing hours and work schedules to understand if their workers are making ends meet every month. If they’re not, employers will have issues with productivity, retention, absenteeism, and more.

Safety is another area that has reemerged in recent years as a critical focus. A hundred years ago we were talking about basic safety – protection against fire, the air we breathe in the workplace, and more. Today we’re still focused on those things, the pandemic reminded us why they’re so important, but we’re also focused on psychological safety. Are you able to speak up? Can you offer ideas? Will you be heard? According to a recent poll, the top reason people planned to quit was because they want better working conditions.

Fair treatment is fundamental. People must feel like they’re treated fairly and appreciated with regard to their race, ethnicity, gender, age, and disability, and where they sit in the organization. Is there an acknowledgement of the value and insights that workers at every level bring to the organization? Is there a commitment and constant evaluation of equity within the organization, including tracking and releasing demographic numbers, ensuring senior leadership represents the demographic makeup of the organization, and with clear mechanisms in place for reporting and assessing non-equitable environments. Is everyone respected and able to speak up the way that senior leadership is?

Opportunity and growth is why people stay. They need to have access to training, and to see their growth path at the organization. If that path isn’t there – and only 39% of U.S. workers in a recent poll say they receive the training and development they want – people eventually have to seek that growth elsewhere. And again, growth isn’t limited to white collar workers, but includes wage growth through better jobs, too.

Purpose is a term that’s thrown around a lot, and I historically have found it overemphasized when the first four elements aren’t satisfied. But it’s important for a couple of reasons. One of the things that JUST Capital hears from polling is that companies need to take action on the issues that align with their values. Do employees know what those values are? Do they feel like they’re connected to what the company is aspiring to do in the world? This is the underlying question – do people see their work as contributing to the broader mission of the organization and their own personal mission?

As Arvind Krishna, CEO at IBM, said on CNBC recently, “At the end of the day, you have to be competitive on wages, you have to be competitive on benefits, you have to give people a career path they enjoy – and they have to believe in the company, that the work they’re doing is serious and benefits society.”

Gallup is out with a new poll that shows U.S. employee engagement is at its lowest in a decade, with just 34% of workers saying they’re engaged in their work and workplace. Disengaged workers cost the economy between $450 and $550 billion per year, in addition to the cost for individual businesses. The cost of turnover is estimated around one third of each workers’ earnings. And companies who prioritize their workforces outperform their peers in the market.

As investors, workers, and managers make more concrete asks around “S” strategies, this framework is one way for employers to better advance and align business strategy with this growing focus. Unless companies address these elements, and then adopt them as a business strategy, they will see worse business outcomes including decreased productivity and lower retention. And, most importantly, an investment in workers unlocks the value that an engaged, experienced workforce provides.

To learn more about how your company can implement this framework, reach out to our corporate engagement team. For more on how to assess workers’ financial security, explore resources from The Worker Financial Wellness Initiative and get in touch on how your company can join leaders like Chipotle, Prudential, Verizon, and more.

Nearly two years into the COVID-19 pandemic, the U.S. workforce is once again squarely in the spotlight. And it’s not just that the Great Resignation is wearing on, with the Department of Labor this week reporting 10.9 million jobs were open in December 2021. Major signals from various parts of the market are showing companies and investors are paying attention to this in a new and important way. Asset managers like State Street, Vanguard, and BlackRock have all issued 2022 proxy voting guidelines that emphasize that they’re looking at the materiality of good jobs.

There is clearly a recognition across sectors that an investment in workers is, at the very least, worth considering as a business strategy, and in many cases, an increased acknowledgement that they represent untapped value to business and to society. The macro trends have also translated to a heightened focus on the “S” (Social) factors in ESG, and better definitions around it.

What’s the business imperative that markets need to focus on today?

Interestingly, the current momentum is behind the first, around defining what to measure, and mostly lagging on the latter two.

So first, defining what Social factors matter most is important. And certainly workers’ basic financial security, opportunities for mobility and advancement, and workplace equity are critical elements. Unfortunately, corporate disclosure on these “S” issues tend to be negligible, token, or nonexistent, as JUST analysis has shown. The Social factors are also unstandardized, making it challenging to meaningfully benchmark and compare company performance. While this may soon change, as the SEC has signaled it is considering new human capital standards, choosing to not disclose at all sends a message to stakeholders, and leaves companies falling back on inadequate benchmarks and behaviors.

But it also feels like nonprofits, philanthropists, government, and the private sector are spending too much time defining the “S” at the expense of action. Now is the moment to shift momentum towards incentivizing companies to invest in workers and ensuring ESG inflows are driving connected outcomes.

For JUST, 2022 is the year to not only define but align and drive action on the “S” of ESG. That means inspiring higher levels of transparency and disclosure by companies on key metrics, and using the power of data, storytelling, and markets to accelerate action. If we don’t connect capital going toward ESG inflows to “S” outcomes, our collective work runs the risk of being merely the new “green-” or “purpose washing.” With new human capital data in hand, companies, employees, investors, and other stakeholders will have a more holistic and accurate benchmark for how to align operations with worker issues. In other words, it’s time to ensure meaningful change is attached to ESG.

To power this transition, we’re expanding our corporate action team, bringing in new nonprofit partners to help us pull in the same direction, and utilizing new platforms like our partnership with CNBC to shine a light on research insights, data benchmarks, and corporate performance to drive impact. We’re excited about where we’re headed and hope you’ll join us as a corporate leader, ESG partner, or supporter on this journey.

For the first time in 15 years, there is serious national momentum around raising the federal minimum wage, potentially to $15. With this momentum comes the opportunity to examine our national priorities around wages and jobs, particularly as we emerge from the pandemic and continue to grapple with racial inequity in the U.S.

The minimum wage emerged as an answer to the Great Depression, and was codified in the late 1930s as part of a broader push to establish the floor for labor standards in America. It was born from the recognition that the government needed to create a baseline for how companies and the market could treat people and value their work. It was a time not too different from the one we’re in now – featuring a major stratification of wealth, as well as a realization that society wasn’t protecting enough people and that the market wasn’t as reliable or transparent as we needed it to be.

In the 1970s, we ushered in a new set of expectations for our economy, when corporate America codified the conventional wisdom that minimizing labor costs and keeping wages low is key to profitability. So it’s no coincidence that wages haven’t meaningfully gone up in a long time. According to recent work by the Economic Policy Center, worker pay has grown 13.7% since 1978. By comparison, CEO pay grew over 1000% in that same time horizon. That extreme contrast signals a belief system about who brings value to business.

And the minimum wage is a barometer for the values of a society. It speaks to our collective baseline expectations for how any business should treat someone. According to our extensive annual survey research efforts, Americans across the ideological divide agree that business leaders should prioritize workers above all else, starting with wages. As a nation, we should be aspiring to create jobs that give people the freedom to support themselves and their families.

In recent months, we’ve heard an increasingly loud argument about the irrelevance of the federal minimum wage – that local economies across the U.S. are so vastly different that one standard simply isn’t applicable. And while I can relate to that central premise, it misses a key point – that society dictates what is acceptable and unacceptable. That reality makes wages a federal issue.

On the other hand, good wages do vary dramatically across different geographies and counties, and therefore I welcome those who seek to eliminate the federal minimum wage to seize the living wage as an alternative concept. According to the Living Wage Calculator created by MIT professor Amy Glasmier, the living wage in counties across the U.S. ranges from around $18 to $30 for a family of four. A living wage, conceptually, is compensation that covers an individual’s or a family’s monthly bills for essential needs. Childcare. Housing. Transportation. Food. Living wages fluctuate dramatically based on if an individual has a partner and/or children, in addition to where they live. When we talk about raising the minimum wage, we miss that nuance and context. The minimum wage is not a concept designed to cover any one person’s monthly costs, while a living wage is.

We also hear a lot about how increasing the minimum wage will cost jobs and hurt business. There continues to be a lot of work done, and disagreement around, if and how many jobs could be lost. Increasingly researchers are finding that significant job loss is unlikely. Critically, this line of reasoning again misses the broader point – poverty-level jobs should not be what we aspire to. $15 an hour will not be a living wage for a family of four anywhere in the country. It would only be a living wage for a single adult with no children in about half of the states in the country. And good jobs can help businesses and workers.

But despite the importance of the minimum wage, it’s also a blunt instrument, further undermined by the fact that, when it was first established, it was in the context of a broader push for safe and family-supporting jobs. With the establishment of the minimum wage came overtime, outlawing child labor, and the creation of today’s concept of employment. The minimum wage, and indeed wages overall, can and should be understood in the context of jobs, not as a standalone.

Many business leaders today understand this. In 2019, PayPal identified the importance of understanding if its workers were getting by and getting ahead, and so undertook a formal assessment of the financial security of call center workers, focusing on their “net disposable income.” This analysis essentially looked at the workers’ wages, in addition to costs of healthcare, ability to save, and pay for emergencies. Since this assessment took place, JUST Capital and PayPal, along with the Financial Health Network and the Good Jobs Institute, have partnered to create the Worker Financial Wellness Initiative, which asks all corporate executives to consider whether they know if their workers’ wages are covering the bills, and if workers are getting by overall – and if they don’t know, to conduct an assessment, like PayPal did, to find out. In short, we need to move away from thinking only about one piece of the puzzle (wages), and instead examine the full financial lives’ of people. And we need to expect business leaders, who are increasingly trusted more than politicians, to work toward a future that creates quality jobs within their own companies, regardless of industry.

Research shows that engaged and financially secure workers can bring significant value to businesses. MIT Sloan Professor Zeynep Ton, founder of the Good Jobs Institute, has done extensive research on the business case for good jobs in the retail sector. The data shows that this approach can lead to competitive advantage. It can increase retention and productivity, and in turn, customer satisfaction. Mercer found that employers report losing $250 billion each year due to the stress of their employees. And JUST Capital’s own work shows that companies that invest in their workers also outperform their peers in the market.

The moral of the story is that the minimum wage is a crucial step on the journey toward a society and an economy that recognizes and values good jobs and good wages. And to be clear: raising wages is a critical piece of the puzzle. But over the decades, we’ve lost the context for this conversation, and have treated it as a government issue rather than a business AND government issue. As the dialogue in Washington gets more intense about raising the minimum wage, political leaders should consider this issue in the context of the broader push to create good jobs in our country, and understand that even $15 is not a living wage. And business leaders should embrace this new reality, where paying people well leads to better long-term business outcomes, and shows real leadership. As we emerge from the pandemic to a changed economy, it’s time to create an economy where a certain caliber of job is simply unacceptable, and where all Americans are able to both get by and get ahead.