Ten years ago, Walmart CEO Doug McMillon made a bet that flew in the face of conventional retail wisdom: invest heavily in frontline workers through higher wages, better training, and expanded benefits. The result was increased value for the company, shareholders, and their associates. Just’s analysis frequently highlighted this. This week, in a powerful LinkedIn reflection and in remarks from the company’s workforce conference in Bentonville, McMillon connected that decade-long commitment to how the company plans to navigate AI-related transformation.

The timing is striking. Headlines have focused on AI-driven job cuts, and McMillon himself acknowledged that “AI is going to change literally every job”. But he’s using this moment to double down on the philosophy that got Walmart here: “investing in wages, benefits, and education shouldn’t be seen as a line item, it should be valued as the strategic enabler that it is.”

This approach aligns perfectly with what the majority of Americans want. Worker issues such as fair pay, well-being, and training and advancement consistently rank as top priorities in our polling. And our data supports the business case: since 2021, companies excelling on worker issues in our rankings have outperformed the Russell 1000 equally-weighted index by over 20%. McMillon noted that Walmart’s shareholder returns are up about 490% since 2015, outperforming the S&P500.

Behind fair wages, the #2 issue for the American public this year was ethical leadership. McMillon’s remarks may offer the blueprint for ethical leadership in the AI era. He didn’t sugarcoat the challenge. AI will eliminate some jobs and create others. He outlined that the composition of Walmart’s 2.1 million-person workforce will change dramatically over the next three years, even as headcount stays flat. That transparency builds trust.

As we work over the next few months to begin to define what just AI deployment looks like, Walmart’s strategy is an exciting place to start.

Be well,

Martin

(Getty Images/Bill Pugliano)

“Old-timers in our plants were saying, ‘It’s no longer a career, Mr. Farley. Working at Ford is no longer a career.’”

NVIDIA CEO Jensen Huang is encouraging Gen Z to go to trade schools, stating that the AI future will require “hundreds of thousands” electricians, carpenters, and plumbers to help build data centers and AI infrastructure. Fortune has the story.

The Wall Street Journal asks when we will see results of the “epic” levels of AI spending, citing worries many investors have that there is no clear timeline for when they’d see any return, echoing the dotcom bubble.

The New York Times reports that California Governor Gavin Newsom has signed a sweeping new AI law that will force companies to report the safety protocols they’re using in development, the greatest risks posed by their technologies, and more.

Fortune reveals that 62% of white collar workers would transition to a trade job if it meant more employment stability and better pay, particularly for younger workers.

The New York Times takes a deeper look at the ways in which the Trump Administration could solve issues with the H-1B program and argues that the proposed $100k fee per new hire is not the solution.

Bloomberg worries that large swaths of Americans no longer have meaningful spending power to impact the economy, which is why stocks continue to grow despite American sentiment being down on the current state of the economy.

Nearly 100,000 government workers resigned this week as part of the Trump administration’s “Deferred Resignation Program” implemented in April of this year, which claims to save taxpayers $28 billion dollars. Newsweek has the story.

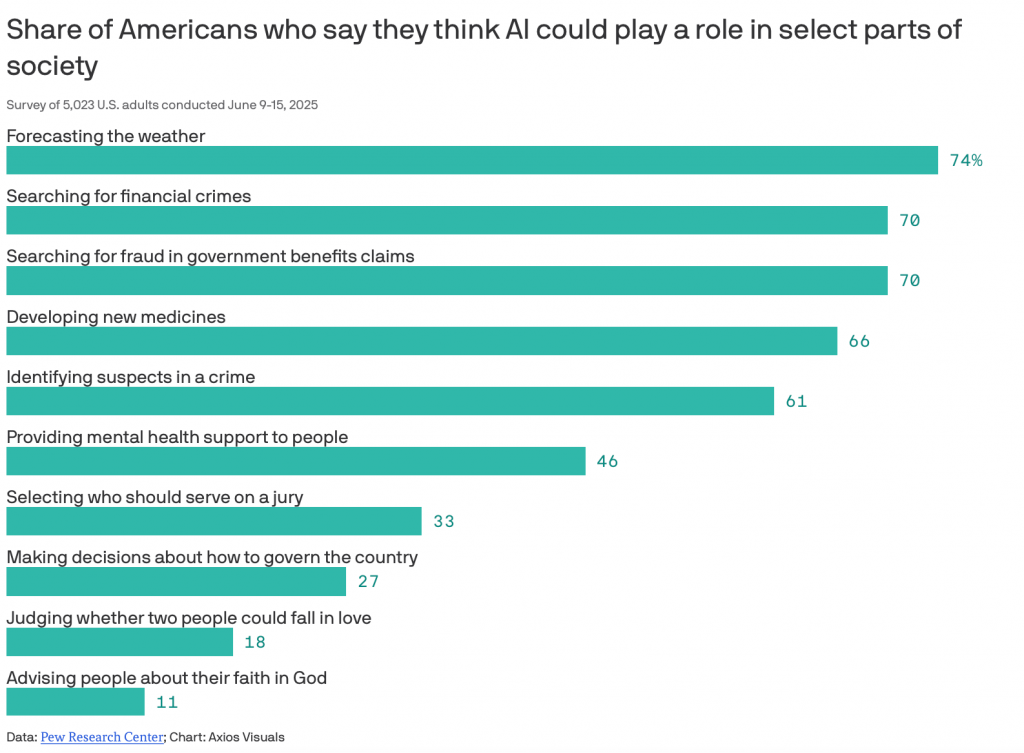

Pew Research released several pieces of data on how Americans are using AI. One important insight for company leaders? Most Americans believe it’s important to tell the difference between AI- and human-generated content, but very few feel like they can.

NEW YORK, NY September 29, 2025 – Just Capital today announced three strategic appointments to its C-suite leadership team. These hires, with 50+ years of combined expertise across private and nonprofit sectors, equip the organization to complete a significant transformation into an AI-powered data and insights platform focused on measuring, improving, and showcasing corporate stakeholder performance. This new approach will allow Just Capital to provide valuable intelligence – including critical guidance on responsible AI deployment – that helps corporate executives and boards optimize performance on key worker, customer, community, environmental, and shareholder priorities, driving superior outcomes for business and society. It will also increase the impact and scope of the organization’s rankings, indexes, and investment work.

“Just Capital’s transformation couldn’t come at a more important time,” said Martin Whittaker, Chief Executive Officer of Just Capital. “Corporate leaders today are faced with unprecedented change and complex, often competing stakeholder demands. With these hires, the leadership team at Just Capital is supremely well positioned to help companies navigate this new landscape, while unlocking value for stakeholders, shareholders, and society at large. That’s the win-win-win we’ve always believed in, and we couldn’t be more excited for the future.”

Michael Yoo, PhD, joins Just Capital with nearly 20 years of experience leading double-digit growth at information services businesses including Gartner, Skillsoft, and IndigoAg. As Senior Vice President and Group Vice President of Gartner, Yoo grew the combined revenue of three different business units from $200M to $550M over seven years. Yoo will be responsible for the growth of all earned revenue streams and commercial partnerships.

“I’ve seen firsthand how the right intelligence at the right moment can transform business outcomes,” said Yoo. “I’m excited to build upon Just Capital’s tools and insights to deliver C-suites the information they need to make decisions that benefit all stakeholders while driving superior financial returns.”

Thomas Herbig, PhD, joins Just Capital as Chief Research Officer, bringing decades of experience in management consulting, strategy, sales and marketing, mergers and acquisitions, and product management. Before his appointment, he held a range of corporate, nonprofit, and scientific roles, including serving as Director of the McKinsey Center for the Advancement of Problem Solving. At Just Capital, Herbig will lead the expansion of the organization’s research and data initiatives, equipping business leaders with actionable metrics and advancing the definition and measurement of responsible AI deployment.

“As AI reshapes entire industries and ways of working, we have a critical window to influence how businesses use these transformative technologies,” said Herbig. “Our research, insights, and intelligence will provide the roadmap for responsible AI adoption that creates value for all stakeholders.”

Tyler Spalding joins Just Capital from Golin, where he helped develop and grow the agency’s Corporate Affairs advisory practice. His prior experience extends across strategic communications, strategic partnerships, and social impact and sustainability, at industry leaders such as PayPal, eBay Inc., and Edelman. During his decade leading corporate affairs at PayPal, Spalding partnered with JUST Capital to launch the Worker Financial Wellness Initiative, comprised of 15 companies representing 1.2 million U.S. workers. Spalding will be responsible for shaping Just Capital’s brand and engaging key stakeholders across JUST Capital’s ecosystem, including philanthropic funders.

“As we undertake this exciting organizational evolution, Just Capital has a unique opportunity to inspire the next chapter of responsible business,” said Spalding. “My mission is to ensure every boardroom in America understands that our data doesn’t just measure stakeholder value – it predicts business performance.”

President Trump’s proposal to eliminate quarterly earnings reports touches on a fundamental issue for many interested in the future of capitalism: how to embrace longer-term thinking while providing sufficient transparency (especially for retail investors), performance discipline, and market accountability.

The evidence for taking a more long-term perspective is powerful. According to FCLT Global, 90% of executives agree longer time horizons would improve performance, and companies able to do so outstrip competitors in revenue, earnings, and job creation. Business Roundtable has consistently emphasized that long-term thinking is essential for superior business performance and sustainable value creation. Warren Buffett and Jamie Dimon have also argued that quarterly pressures create “an unhealthy focus on short-term profits at the expense of long-term strategy, growth and sustainability.”

One factor to keep in mind is that public demands for more corporate transparency are going up, not down. Our polling shows “communicates honestly and transparently” has risen to become a top 5 issue for the majority of Americans regardless of demographic or political association. In today’s low-trust environment, reducing reporting could backfire.

One solution may be to change what is reported. In their 2018 op-ed, Buffett and Dimon argued that earnings reports should continue as they “support being open with shareholders about actual financial and operational metrics.” What they proposed to eliminate was forecasting or guidance on future quarterly earnings. Doing so would “strengthen the U.S. economy, benefit America’s workers, shareholders and investors, and leave a generational legacy we can be proud of.”

What if we expanded that concept to report more holistically on other forms of stakeholder value creation, such as performance on workforce training; well-being and human capital advancement; investments in local communities and suppliers; improvements in customer satisfaction and privacy protections; progress on AI safety? Could be a win-win for long-term thinkers and transparency advocates alike.

Be well,

Martin

Semafor covers Eliezer Yudkowsky and Nate Soares’s new book “If Anyone Builds It, Everyone Dies”, which argues that nearly everyone will be harmed or destroyed if AI systems continue to be built under the current paradigms.

Meanwhile, CNBC covers OpenAI CEO Sam Altman’s remarks to Tucker Carlson that he’s been “losing sleep” over small model decisions that can have big repercussions.

Fortune speaks to several high-profile CEOs who think that AI innovation will spur 3-day work weeks for many Americans.

Anthropic released data showing that some companies are eliminating entry-level roles altogether.

Fiverr’s CEO announces layoffs and a plan to return to a “startup mentality” as they pivot to being an “AI-first” company. View the full LinkedIn post.

Can AI actually help us reduce our energy consumption despite the costs to run it? The Director of the Energy, Climate Justice, and Sustainability Lab at NYU thinks so. Read the Wall Street Journal op-ed here.

Fortune confirms that many CEOs are using RTO mandates to trim headcounts without having to order actual layoffs.

Business Insider reports that many Americans aged 80 and older who retired from well-paying jobs are now accepting low-paying roles — retail, caregiving, or service positions — to supplement social security and make ends meet as prices rise.

The Wall Street Journal looks at how companies are handling the calls to fire employees based on their social media posts around Charlie Kirk’s death.

Yahoo Finance reports that Ben of Ben & Jerry’s is resigning after 47 years due to parent company Unilever trying to silence the brand’s activism.

Axios reports on new Pew Research data that shows Americans are setting boundaries for what they think AI should be involved with and what it shouldn’t.

“Particularly with middle- and lower-income consumers, they’re feeling under a lot of pressure right now.”

That worrying statement comes from McDonald’s CEO Chris Kempczinski, who earlier this week sat down with Fortune for a conversation on the state of the business. Going further, he relayed that traffic among these demographics is down double-digits, with low-income consumers skipping breakfast in particular.

Other indicators are also concerning. This week brought a dismal jobs report (the first time in four years the economy lost jobs). A new Federal Reserve Bank of New York poll shows that people’s confidence in their ability to find work if they lose their job is the lowest it’s been since they started polling in 2013. They also suggest lower-income households have already begun to change their shopping habits to withstand economic uncertainty.

How are companies responding to help their less well-off customers?

McDonald’s itself is currently cutting prices on certain food combos and offering limited time deals to help customers feeling the pinch. Other chains are making similar attempts,such as Domino’s recent “Best Deal Ever” promotion, which offered any pizza toppings for $9.99.

Other industries are also following suit. FanDuel gave $80,000 to restore Philly’s Septa train service for the Eagles’ season opener after the city officials said it would have to cut express service thanks to budget shortfalls. Grocer Aldi cut prices on 400 everyday items over the summer to offset rising food costs; energy companies (including Eversource) provide eligible customers with up to a 50% monthly discount on their electric bill and flexible payment plans; and earlier this year Target dramatically expanded their healthcare products under $10 to make health and wellness purchases more budget-friendly.

As more and more Americans become squeezed financially, we will surely see more efforts by just companies to ease the pressure.

We will be tracking them.

-Martin

The Washington Post reports that Anthropic (creator of the Claude AI model) has agreed to a history-making $1.5 billion class-action settlement with authors and publishers for allegedly downloading millions of books without permission — marking a notable legal precedent in the ongoing clash between AI development and creators’ rights.

Fortune reveals that the average employee age at tech companies has increased by five years as AI-enabled entry-level job cuts reshape their workforce.

Taco Bell is scaling back their use of AI after the technology led to worse problems with customer ordering compared to human employees.

Former Just Capital board member Dan Hesse discusses authentic leadership as a key way to unlock business value on The Mentors Radio podcast.

The Wall Street Journal reports that health insurance costs for employers are rising more than they have in 15 years, stunning small businesses in particular.

Business Insider looks at how the attempt to crack down on Elon Musk’s pay backfired spectacularly and what lessons can be learned going forward.

Newsweek examines how job changing is dwindling as workers find it harder to secure higher pay at a new company.

Following the removal of their new logo, Cracker Barrel is officially ending all of its restaurant remodels to respond to consumer backlash. Fortune has the story.

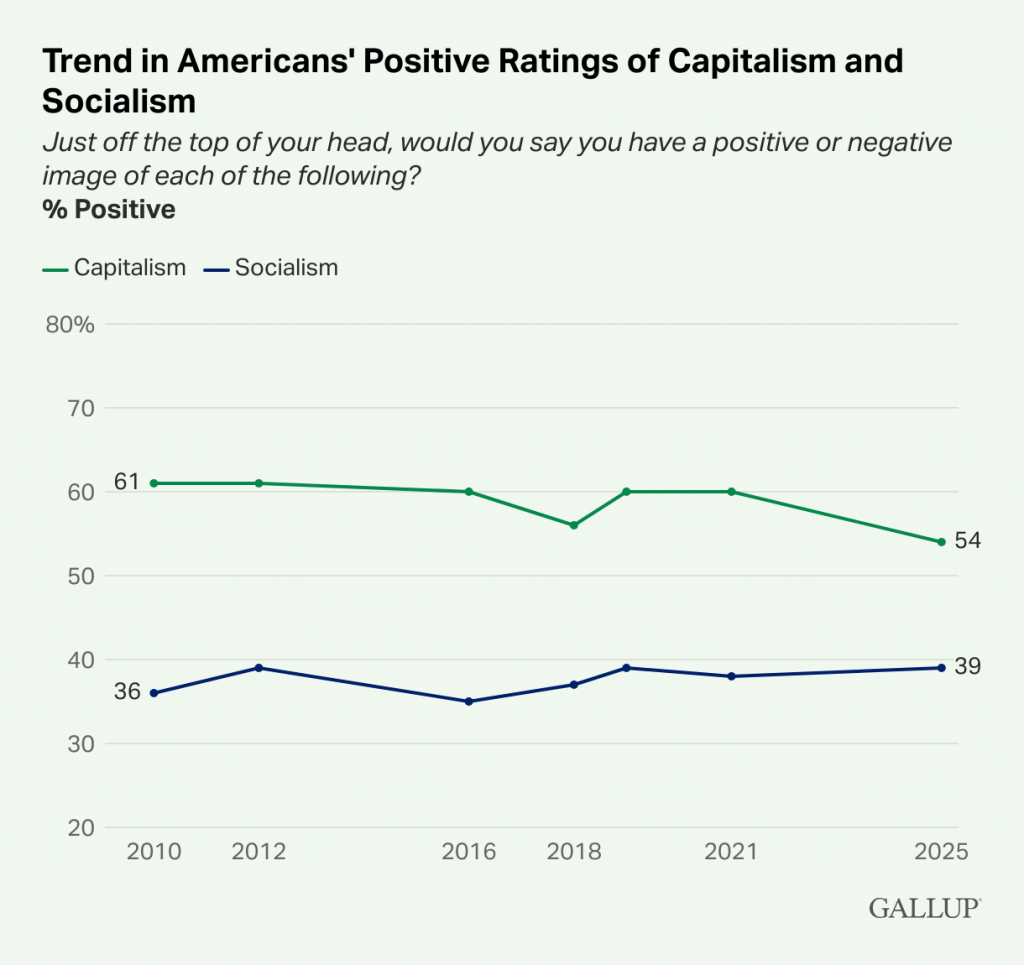

Gallup reveals that only 54% of Americans have a positive view of capitalism, down from 60% in 2021.